Fake Photo? Manipulated Video? How to Spot Sham AI

This to preserve the credibility of digital media and safeguard users from falling victim to scams. As synthetic media becomes more sophisticated, identifying AI-generated manipulations presents a unique challenge, but numerous free apps and toolsare readily available allowing users to validate photo and video authenticity with ease—a major step forward in safeguarding trust in a world increasingly influenced by AI-generated visuals, ensuring transparency and security in the digital age. More below.

How AI Drives Misinformation

Amid the onslaught of highly concerning news headlines spotlighting how deepfake AI-generated photo and video scams are driving rampant misinformation and wreaking havoc across digital, cultural, workplace, political and other societal frameworks, solutions are emerging combat AI-driven misinformation and fraud before people fall victim to scams.

One AI disruptor transforming the fight against AI fraud is BitMind—an AI deepfake detection authority that offers a suite of free apps and tools that instantly identify and flag AI-generated images before you fall victim.

Built by AI Engineers

Built by a team of AI engineers hailing from leading tech companies like Amazon, Poshmark, NEAR, and Ledgersafe, BitMind’s instant detection of deepfakes helps uphold the credibility of the media, guaranteeing the authenticity of the information we use. A strong deepfake detection enhances digital interactions, supports better decision making and strengthens the integrity of the modern digital world—serving to protect reputations, shield finances and maintain trust for celebrities, politicians, public figures … and everyone else.

For both B2C and B2B use, these 5 BitMind tools are free and accessible to anyone:

AI Detector App: A simple web page where users can drag-and-drop suspicious images for fast deepfake detection results;

Chrome Extension: Flags AI-created content in real-time, while browsing.

X Bot: Verifies if images on X/Twitter are real or AI-generated;

Discord Bot: Verifies if images are real or AI-generated via its Discord Integration;

AI or Not Game: Fun Telegram bot that tests your ability to distinguish between AI-generated and human-created images.

“Recognizing the need to integrate deepfake detection into everyday technology use, our applications fit seamlessly into users’ lives,” notes Ken Miyachi, BitMind CEO. “For example, the BitMind Detection App is a user-friendly application that allows individuals to upload images and quickly assess the likelihood of them being real or synthetic. Additionally, the Browser Extension enhances online security by analyzing images on web pages in real time and providing immediate feedback on their authenticity through our subnet validators. These tools are designed to empower users, enabling them to navigate digital spaces with confidence and security.”

As the world’s first decentralized Deepfake Detection System, BitMind is an open-source technology that enables developers to easily integrate the technology into their existing platforms to provide accurate real-time detection of deepfakes.

“Deepfake technology has emerged as both a marvel and a menace,” continued Miyachi. “With the capacity to create synthetic media that closely mimics reality, deepfakes present unprecedented challenges in privacy, security, and information integrity. Responding to these challenges, we introduced the BitMind Subnet, a breakthrough on the Bittensor network, dedicated to the detection and mitigation of deepfakes.”

According to Miyachi, here are key reasons why BitMind technology is a game changer:

The BitMind Subnet, which represents a pivotal advancement in the fight against AI-generated misinformation. Operating on a decentralized AI platform, this deepfake detection system employs sophisticated AI models to accurately distinguish between real and manipulated content. This not only enhances the security of digital media but also preserves the essential trust in digital interactions.

The BitMind Subnet is equipped with advanced detection algorithms that utilize both generative and discriminative AI technologies to provide a robust mechanism for identifying deepfakes.

BitMind employs cutting-edge techniques, including Neighborhood Pixel Relationships, ensuring competitive accuracy in detection. The operation of the subnet is decentralized, with miners across the network running binary classifiers. This setup ensures that the detection processes are widespread and not confined to any centralized repository, enhancing both the reliability and integrity of the detection results.

Community collaboration is a cornerstone of the BitMind Subnet, actively encouraging the community to contribute to our evolving codebase, and by engaging with developers and researchers, the subnet is continuously improved and updated with the latest advancements in AI.

BitMind combines its extensive industry expertise, cutting-edge academic research, and a deep passion for technology. The team has a proven track record in AI, blockchain, and systems architecture, successfully leading tech projects and founding innovative companies.

What truly sets BitMind apart is their commitment to creating a safer, more transparent digital world where AI benefits humanity, driven by their passion for innovation, security and community engagement. Their technologies are expressly designed to safeguard the integrity of digital media and foster a trustworthy digital ecosystem.

In the modern world full of fake news and increasing cyber threats, BitMind’s innovations are paving the way for a future in which digital trust is not an option, but a necessity. As the threats increase, the global community must be equipped with the means to ingest digital information in a reliable and authentic in order to realize AI’s true potential safely and efficiently. For the Silo, Marsha Zorn.

Ottawa’s forthcoming AI strategy needs to walk a tightrope between two equally important principles: safeguarding Canadians from possible misuses of AI but also giving our private and academic sectors the leeway to use Canada’s AI strengths to develop and commercialize new technologies and products.

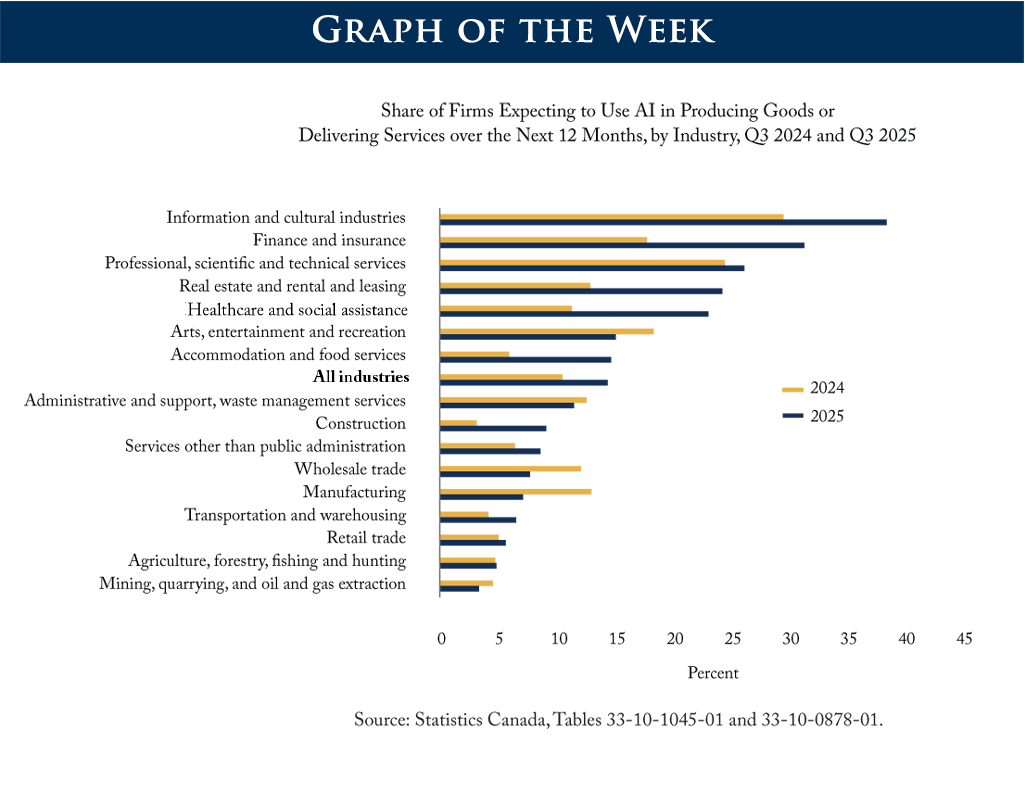

Planned AI adoption rose sharply between Q3 2024 and Q3 2025, but progress remains highly uneven across industries. Knowledge-intensive sectors – such as information and cultural industries, finance and insurance, and healthcare – show the strongest gains, while several goods-producing and operational sectors, including manufacturing, wholesale trade, and mining, show stagnant or declining expectations.

The federal government must clearly define a framework for responsible, widespread AI innovation – one that encourages beneficial development and adoption while setting firm expectations about the harms innovators must avoid.

Canada’s competition reforms must keep pace with data-driven business models by empowering authorities with modern tools to detect, assess, and stop conduct that genuinely harms competition, innovation, or consumers.

The explosive growth of online shopping is reshaping Canadian retail by empowering consumers with unprecedented choice, driving omnichannel innovation, and intensifying competition.

Next year, the United States will host the world’s 20 largest economies for the first time since 2009. Coinciding with America’s 250th anniversary, the 2026 G20 will be a chance to recognize the values of innovation, entrepreneurship, and perseverance that made America great, and which provide a roadmap to prosperity for the entire world. We’ll showcase these values and more when we host the G20 Leaders’ Summit in December 2026 in one of America’s greatest cities, Miami, Florida.

Under President Trump’s leadership, the G20 will use four working groups to achieve progress on three key themes: removing regulatory burdens, unlocking affordable and secure energy supply chains, and pioneering new technologies and innovation. The first Sherpa and Finance Track meetings will be held in Washington, DC, on December 15-16, followed by a series of meetings throughout 2026. As the global economy confronts the changes driven by technologies such as Artificial Intelligence, and shakes off ideological preoccupations around green energy, the President is prepared to lead the way.

We will be inviting friends, neighbors, and partners to the American G20. We will welcome the world’s largest economies, as well as burgeoning partners and allies, to America’s table. In particular, Poland, a nation that was once trapped behind the Iron Curtain but now ranks among the world’s 20 largest economies, will be joining us to assume its rightful place in the G20. Poland’s success is proof that a focus on the future is a better path than one on grievances. It shows how partnership with the United States and American companies can promote mutual prosperity and growth.

The contrast with South Africa, host of this year’s G20, is stark.

South Africa entered the post-Cold War era with strong institutions, excellent infrastructure, and global goodwill. It possessed many of the world’s most valuable resources, some of the best agricultural land on the planet, and was located around one of the world’s key trading routes. And in Nelson Mandela, South Africa had a leader who understood that reconciliation and private sector driven economic growth were the only path to a nation where every citizen could prosper.

Sadly, Mandela’s successors have replaced reconciliation with redistributionist policies that discouraged investment and drove South Africa’s most talented citizens abroad. Racial quotas have crippled the private sector, while corruption bankrupts the state.

The numbers speak for themselves. As South Africa’s economy has stagnated under its burdensome regulatory regime driven by racial grievance, and it falls firmly outside the group of the 20 largest industrialized economies.

Rather than take responsibility for its failings, the radical ANC-led South African government has sought to scapegoat its own citizens and the United States. As President Trump has rightly highlighted, the South African government’s appetite for racism and tolerance for violence against its Afrikaner citizens have become embedded as core domestic policies. It seems intent on enriching itself while the country’s economy limps along, all while South Africans are subject to violence, discrimination, and land confiscation without compensation. Its former Ambassador to the United States was openly hostile to America. Its relationships with Iran, its entertainment of Hamas sympathizers, and cozying to America’s greatest adversaries move it from the family of nations we once called close.

The politics of grievance carried over to South Africa’s Presidency of the G20 this month, which was an exercise in spite, division, and radical agendas that have nothing to do with economic growth. South Africa focused on climate change, diversity and inclusion, and aid dependency as central tenets of its working groups. It routinely ignored U.S. objections to consensus communiques and statements. It blocked the U.S. and other countries’ inputs into negotiations. It actively ignored our reasonable faith efforts to negotiate. It doxed U.S. officials working on these negotiations. It fundamentally tarnished the G20’s reputation.

For these reasons, President Trump and the United States will not be extending an invitation to the South African government to participate in the G20 during our presidency. There is a place for good faith disagreement, but not dishonesty or sabotage.

The United States supports the people of South Africa, but not its radical ANC-led government, and will not tolerate its continued behavior. When South Africa decides it has made the tough decisions needed to fix its broken system and is ready to rejoin the family of prosperous and free nations, the United States will have a seat for it at our table. Until then, America will be forging ahead with a new G20.

Marco Rubio was sworn in as the 72nd secretary of state on January 21, 2025. The secretary is creating a Department of State that puts America First.

AI is fundamentally redefining leadership by providing new tools, frameworks, and systems that allow leaders not just to manage complexity, but to see, challenge, and reshape their organizations in ways never before possible. The competitive mandate for leaders is clear: harness AI not merely for efficiency, but as an engine for deeper self-awareness, structured dissent, and proactive sensing that unlocks true organizational agility and resilience.

Strategic Frameworks for Next-Gen AI Leadership

Forward-thinking leaders are moving beyond pilot projects and isolated automation to experiment with new, holistic approaches—many inspired by concepts like the Leadership Mirror, Red-Team Loop, and Organization Pulse Monitor. These paradigms operationalize AI in ways that directly address the perennial blind spots, biases, and inertia that often undermine executive decision-making.

George Yang- helping organizations and executives embrace AI.

The Leadership Mirror: Cultivating Radical Self-Awareness

The Leadership Mirror uses AI to continuously analyze leadership communication, decision rationale, and team interactions, surfacing insights that are often overlooked or difficult for humans to acknowledge. For example, Microsoft has begun leveraging AI tools to track who dominates meetings, which voices get systematically dismissed, and when evidence is overridden by intuition—creating dashboards that encourage leaders to confront uncomfortable patterns.

This approach helps leaders challenge their own narrative, improve inclusiveness, and drive more thoughtful debate.

With AI’s ability to process language in real time, leaders can receive feedback loops and “reflections” that support a culture of deliberate, transparent leadership.

The Leadership Mirror is also a vehicle for mitigating the “competence penalty,” where women and older workers face skepticism for using AI—even when it enhances productivity. By surfacing evidence of expertise and impact, it reduces bias and builds psychological safety.

There are different types of AI including less sophisticated models such as Generative AI. To decide whether to use generative artificial intelligence for a task, ask yourself whether it matters if the output is true and you have the expertise to verify the tool’s output. (Adapted from Aleksandr Tiulkanov‘s LinkedIn post)

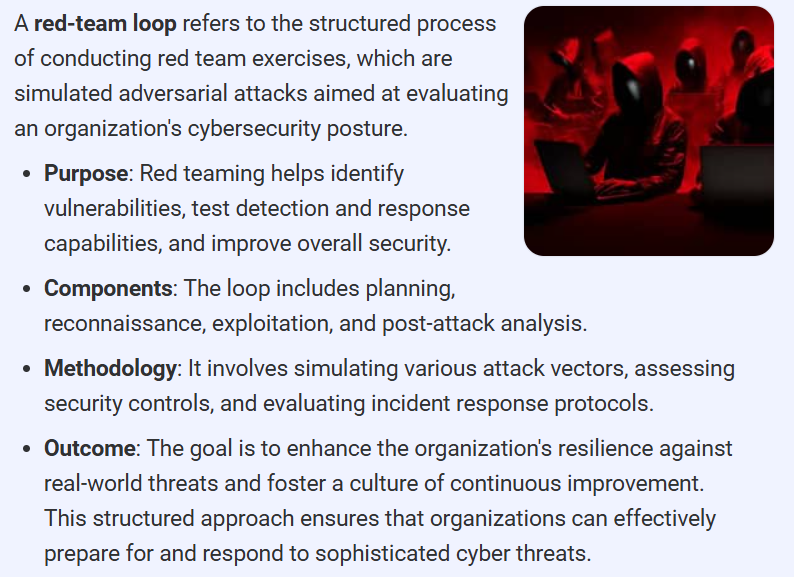

The Red-Team Loop: Embedding Structured Dissent

To counter groupthink and executive overconfidence, Red-Team Loop systems employ AI to automate adversarial reviews of strategy and operational decisions. Verizon, for instance, uses an AI framework that captures assumptions, risks, and anticipated outcomes for major decisions, then generates simulated critiques and alternative scenarios—sometimes challenging senior executives on blind spots they themselves hadn’t recognized.

By proactively “red-teaming” their own decisions, leaders foster a culture where dissent is routine, rational, and data-driven—not ad hoc or punitive.

The approach is especially valuable in M&A, crisis management, and product launches, where high-stakes, high-ambiguity decisions benefit from rigorous challenge.

Leading boards now expect Red-Team Loops as part of their fiduciary duty, recognizing that the cost of missed risks is measured not just in dollars, but reputation and long-term viability.

Organization Pulse Monitor: Proactive Sensing for Culture and Risk

The Organization Pulse Monitor uses AI to detect weak signals in organization culture, ethical risk, and operational friction long before traditional metrics or surveys would register them. Some organizations have begun linking AI-powered sentiment analysis of internal communications, workflow behaviors, and network interactions to predict where a culture may be straining, where compliance risks are emerging, or where silent dissent is brewing.

When Pulse Monitors flagged drops in engagement and early warning signs of burnout, one multinational fast-tracked well-being interventions, pre-empting attrition.

AI-driven pulse scans also help surface ethical risks—such as exclusionary behaviors or data privacy concerns—enabling leaders to respond immediately, not months later.

Actionable Strategies: Bringing AI Experiments to Leadership

How can senior leaders experiment and innovate with these systems while maximizing value and minimizing risk?

Map Adoption Hotspots and Blind Spots: Use mirror and pulse data to identify where AI is catalyzing positive behaviors—and where competence penalties or shadow AI usage may be undermining equity or performance. Target interventions accordingly.

Mobilize Role Model Leaders: Encourage respected senior leaders, particularly those from underrepresented demographics, to visibly experiment with and champion AI tools. Research shows that when these role models use AI openly, adoption gaps shrink, and psychological safety rises.

Redesign Evaluation and Disclosure Policies: Shift performance metrics from subjective ratings of proficiency to objective impact, cycle time, accuracy, and innovation. Blind reviews and private feedback mechanisms can reduce bias against AI users and drive fairer rewards.

Embed Structured Red-Teaming in Decision Flows: Institutionalize adversarial testing of key decisions, making AI-enabled dissent a standard step—not a threat or afterthought. Leaders should receive regular “contrarian” insights, not just consensus-building reports.

Common Pitfalls and Human Impact

Despite rising investment, less than one-third of US employers believe staff are equipped for critical thinking in the AI era, and only 16% of American workers use AI on the job despite widespread availability. The main barriers are not just technical, but social: competence penalties, fear of reputation loss, and resistance among influential skeptics.

Competence Penalty: AI users, especially women and older employees, may face a perception of diminished competence. This undermines adoption and can exacerbate workplace inequality.

Shadow AI and Hidden Risks: Employees sometimes use unauthorized tools to bypass bias, exposing the organization to compliance, reputational, and security risk.

Skill Gaps vs. Work Context: Traditional training falls short without tailored, role-specific feedback loops—AI tutors offer scalable, personal learning but must be embedded in daily workflow, not delivered in isolation.

Governance, Ethics, and Sustainable Change

Human-centered leadership isn’t optional—it’s a strategic imperative. Boards and executives must be proactive in:

Instituting transparent governance for all AI systems (mirrors, loops, monitors), with clear oversight on privacy, fairness, and impact.

Ensuring structured role-modeling and psychological safety—particularly for vulnerable groups confronting competence penalties.

Making change management a continuous process, with AI as both coach and sentinel, not just a dashboard.

The call to action for C-suite leaders is urgent and profound: treat responsible, experimental, and self-critical AI adoption as the core discipline of next-generation leadership. Not just for efficiency, but for building organizations where insight, challenge, and well-being are sustainably enabled. Those who master the trifecta of mirror, loop, and pulse will set the new standard for profitable, human-centered growth in the age of AI.

More about:

George Yang is a Toronto-based digital innovator and AI adoption strategist with over 15 years of experience in marketing and digital transformation. As Chair of the AI Working Group at the National Payroll Institute, he helps organizations translate AI strategy into measurable business outcomes. George is passionate about making AI adoption ethical, practical, and impactful, bridging the gap between innovation and implementation across industries. georgeyang.ca

“Pay attention students, write this down for memorization.” The Trivium and Quadrivium, medieval revival of classical Greek education theories, defined the seven liberal arts necessary as preparation for entering higher education: grammar, logic, rhetoric, astronomy, geometry, arithmetic, and music. Even today, the education disciplines identified since Greek times are still reflected in many education systems. Numerous disciplines and branches have since emerged, ranging from history to computer science…

Now comes the Information Age, bringing with it Big Data, cloud computing, artificial intelligence as well as visualization techniques that facilitate the learning of knowledge.

All this technology dramatically increased the amount of knowledge we could access and the speed at which we could generate answers to our questions.

“New and more innovative knowledge maps are now needed to help us navigate the complexities of our expanding landscape of knowledge,” says Charles Fadel. Fadel is the founder of the Center for Curriculum Redesign, which has been producing new knowledge maps that redesign knowledge standards from the ground up. “Understanding the interrelatedness of knowledge areas will help to uncover a logical and effective progression for learning that achieves deep understanding.”

Joining us in The Global Search for Education to talk about what students should learn in the age of AI is Charles Fadel, author of Four-Dimensional Education: The Competencies Learners Need to Succeed.

“We need to identify the Essential Content and Core Concepts for each discipline – that’s what the curation effort must achieve so as to leave time and space for deepening the disciplines’ understanding and developing competencies.” — Charles Fadel

Charles, today students have the ability to look up anything. Technology that enables them to do this is also improving all the time. If I want to solve a math problem, I use my calculator, and if I want to write a report on the global effects of climate change, I pull out my mobile. How much of the data kids are being forced to memorize in school is now a waste of time?

The Greeks bemoaned the invention of the alphabet because people did not have to memorize the Iliad anymore. Anthropologists tell us that memorization is far more trained in populations that are illiterate or do not have access to books. So needing to memorize even less in an age of Search is a natural evolution.

However, there are also valid reasons for why some carefully curated content will always be necessary.

Firstly, Automaticity. It would be implausible for anyone to constantly look up words or simple multiplications – it just takes too long and breaks the thought process, very inefficiently. Secondly, Learning Progressions. A number of disciplines need a gradual progression towards expertise, and again, one cannot constantly look things up, this would be completely unworkable. Finally, Competencies (Skills, Character, Meta-Learning). Those cannot be developed in thin air as they need a base of (modernized, curated) knowledge to leverage.

Sometimes people will say “Google knows everything” or “ask AI” and it is striking, but the reality is that for now, Google stores everything. Of course, with AI, what is emerging now is the ability to analyze a large number of specific problems and make predictions, so eventually, Google and similar companies will know a lot more than humans can about themselves!

Closeup of mobile phone with language learning application in jeans pocket. focus on screen

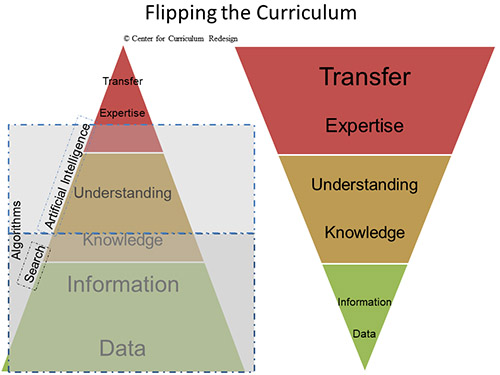

“What we need to test for is Transfer – the ability to use something we have learned in a completely different context. This has always been the goal of an Education, but now algorithms will allow us to focus on that goal even more, by ‘flipping the curriculum’.” — Charles Fadel

If Child A has memorized the data in her head while Child B has to look up the answers, some might argue that Child A is smarter than Child B. I would argue that AI has leveled the playing field for Child A and Child B, particularly if Child B is digitally literate, creative and passionate about learning. What are your thoughts?

First, let’s not conflate memory with intelligence, which games like Jeopardy implicitly do. The fact that Child A memorized data does not mean they are “smarter” than Child B, even though memory implies a modicum of intelligence. Second, even Child B will need some level of content knowledge to be creative, etc. Again, this is not developed in thin air, per the conversation above.

So it is a false dichotomy to talk about Knowledge or Competencies (Skills/Character/Meta-learning), it has to be Knowledge (modernized, curated) and Competencies. We’d want children to both Know and Do, with creativity and curiosity.

Lastly, we need to identify the Essential Content and Core Concepts for each discipline – that’s what the curation effort must achieve so as to leave time and space for deepening the disciplines’ understanding and developing competencies.

Given the impact of AI today and the advancements we expect each year, when should (all) school districts introduce open laptop examinations to allow students equal access to information and place emphasis on their thinkingskills?

The question has more to do with Search algorithms than with AI, but regardless, real-life is open-book, and so should exams be alike. And yes, this will force students to actually understand their materials, provided the tests do more than multiple-choice trivialities, which by the way we find even at college levels for the sake of ease of grading.

What we need to test for is Transfer – the ability to use something we have learned in a completely different context. This has always been the goal of an Education, but now algorithms (search, AI) will allow us to focus on that goal even more, by “flipping the curriculum”.

Today, if a learner wants to do a deep dive into any specific subject, AI search allows them to do this outside of classroom time. What do you say to a history teacher who argues there’s no need to revise subject content in his classroom?

For all disciplines, not just History, we must strike the careful balance between “just-in-time, in context” vs “just-in-case”. Context matters to anchor the learning: in other words, real-world projects give immediate relevance for the learning, which helps it to be absorbed. And yet projects can also be time-inefficient, so a healthy balance of didactic methods like lectures are still necessary. McKinsey has recently shown that today that ratio is about 25% projects, which should grow a bit more over time as education systems embed them better, with better teacher training.

Second, it should be perfectly fine for any student to do deep dives as they see fit, but again in balance: there are other competencies needed to becoming a more complete individual, and if one is ahead of the curve in a specific topic, it is of course very tempting to follow one’s passion. And at the same time, it is important to make sure that other competencies get developed too. So, balance and a discriminating mind matter.

Employers consider ethics, leadership, resilience, curiosity,mindfulness and courage as being of “very high” importance to preparing students for the workplace. How does your curriculum satisfy employers’ demands today and in the years ahead?

These Character qualities are essential for employers and life needs alike, and they have converged away from the false dichotomy of “employability or psycho-social needs.” A modern curriculum ensures that these qualities are developed deliberately, systematically, comprehensively, and demonstrably. This is achieved by matrixing them with the Knowledge dimension, meaning teaching Resilience via Mathematics, Mindfulness via History, etc. Employers have a mixed view and success as to how to assess these qualities, so it is a bit unfair that they would demand specificity they do not have. And it is also unfitting of school systems to lose relevance.

people, education, technology and exam concept – close up of students with smartphones taking picture of books page and making cheat sheet in school library

“Educators have been tone-deaf to the needs of employers and society to educate broad and deep individuals, not merely ones that may go to college. The anchoring of this problem comes from university entrance requirements.” — Charles Fadel

There is a significant gap between employers’ view of the preparation levels of students and the views of students and educators. The problem likely exists partly because of incorrect assumptions on both sides, but there are also valid deficiencies. What specific inadequacies are behind this gap? What system or process can be devised to resolve this issue?

On one side, employers are expecting too much and shirking their responsibility to bring up the level of their employees, expecting them to graduate 100% “ready to work” and having to spend nothing more than job-specific training at best. On the other side, educators have been tone-deaf to the needs of employers and society to educate broad and deep individuals, not merely ones that may go to college.

The anchoring of this problem comes from university entrance requirements (in the US, AP classes, etc.) and their associated assessments (SAT/ACT scores). They have for decades back-biased what is taught in schools, in a very self-serving manner – narrowly as a test of whether a student will succeed at university. It is time to deconstruct the requirements to broaden/deepen them to serve multiple stakeholders. For the Silo, C.M. Rubin.

(All photos are courtesy of our friends at CMRubinWorld)

C. M. Rubin and Charles Fadel

Join me and globally renowned thought leaders including Sir Michael Barber (UK), Dr. Michael Block (U.S.), Dr. Leon Botstein (U.S.), Professor Clay Christensen (U.S.), Dr. Linda Darling-Hammond (U.S.), Dr. MadhavChavan (India), Charles Fadel (U.S.), Professor Michael Fullan (Canada), Professor Howard Gardner (U.S.), Professor Andy Hargreaves (U.S.), Professor Yvonne Hellman (The Netherlands), Professor Kristin Helstad (Norway), Jean Hendrickson (U.S.), Professor Rose Hipkins (New Zealand), Professor Cornelia Hoogland (Canada), Honourable Jeff Johnson (Canada), Mme. Chantal Kaufmann (Belgium), Dr. EijaKauppinen (Finland), State Secretary TapioKosunen (Finland), Professor Dominique Lafontaine (Belgium), Professor Hugh Lauder (UK), Lord Ken Macdonald (UK), Professor Geoff Masters (Australia), Professor Barry McGaw (Australia), Shiv Nadar (India), Professor R. Natarajan (India), Dr. Pak Tee Ng (Singapore), Dr. Denise Pope (US), Sridhar Rajagopalan (India), Dr. Diane Ravitch (U.S.), Richard Wilson Riley (U.S.), Sir Ken Robinson (UK), Professor Pasi Sahlberg (Finland), Professor Manabu Sato (Japan), Andreas Schleicher (PISA, OECD), Dr. Anthony Seldon (UK), Dr. David Shaffer (U.S.), Dr. Kirsten Sivesind (Norway), Chancellor Stephen Spahn (U.S.), Yves Theze (LyceeFrancais U.S.), Professor Charles Ungerleider (Canada), Professor Tony Wagner (U.S.), Sir David Watson (UK), Professor Dylan Wiliam (UK), Dr. Mark Wormald (UK), Professor Theo Wubbels (The Netherlands), Professor Michael Young (UK), and Professor Minxuan Zhang (China) as they explore the big picture education questions that all nations face today.

C. M. Rubin is the author of two widely read online series for which she received a 2011 Upton Sinclair award, “The Global Search for Education” and “How Will We Read?” She is also the author of three bestselling books, including The Real Alice in Wonderland, is the publisher of CMRubinWorld and is a Disruptor Foundation Fellow.

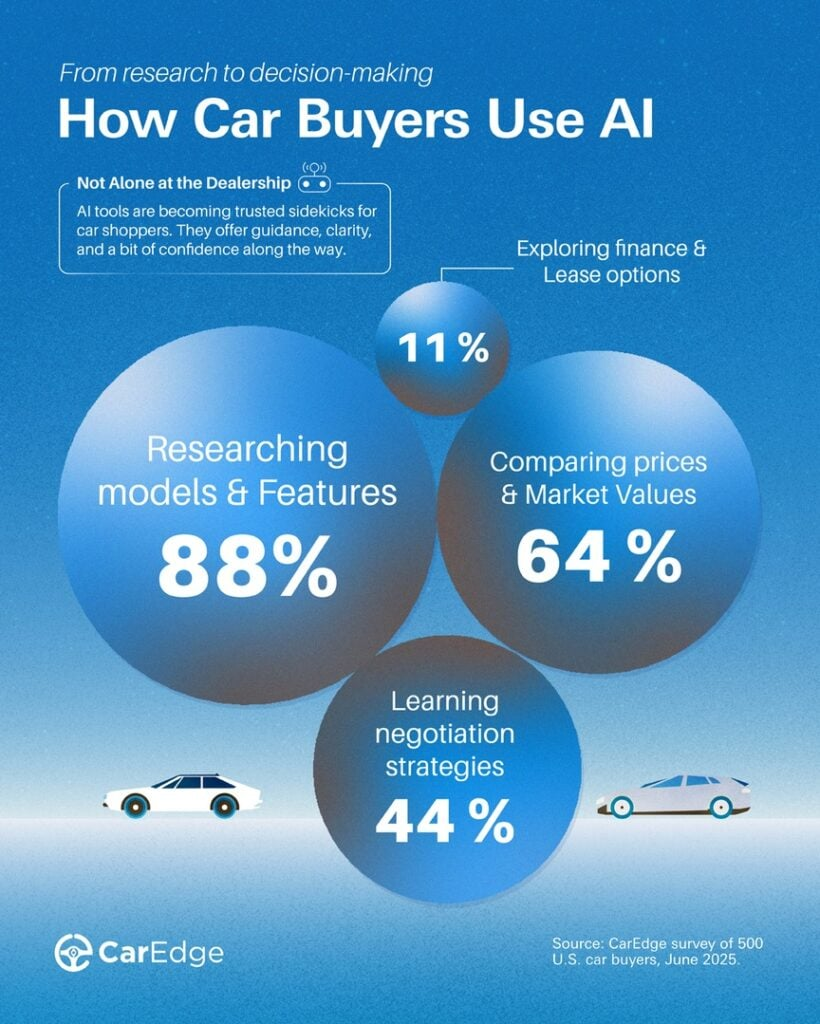

A recent consumer survey backed by similar results from Elon University reveals that AI adoption for car shopping is skyrocketing, rapidly becoming a standard part of the automobile buying process. This as fully one in four buyers have already used AI tools this year to research, compare prices, negotiate and otherwise outsmart dealerships, and an overwhelming 88% found it helpful. Signaling a seismic shift in the way North Americans are now shopping for cars, nearly half of consumers indicated plans to use AI in their next purchase. Not just for buyer benefits, dealerships are gleaning critical business intelligence from AI to inform sales strategies, train staff and elevate customer engagement. The below report from our friends at CarEdge, which offers its own AI Negotiator car buying tool saving shoppers thousands, details the first data-backed look at how AI tools are reshaping the car buying experience.

Mornine- AI powered car dealership robot.

Study: 1 in 4 Car Buyers Tap AI for Better Deals

Artificial intelligence is changing the way North Americans buy cars, and it’s a transition that is happening quickly. In the first-ever survey of its kind, CarEdge asked 500 car shoppers if they’re using AI tools like ChatGPT to research, compare, and negotiate during the car buying process. The results confirm a major shift is underway. One in four car buyers in 2025 are already using AI tools to gain an edge, and future buyers are even more likely to embrace these technologies.

Car buyers are finding AI to be a valuable tool. Among those who used tools like ChatGPT, Perplexity, Google Gemini, and others, 88% said it was helpful. AI is quickly becoming a trusted co-pilot for car buyers.

Key Findings: Car Buying Is Changing

The 2025 CarEdge AI & Car Buying Survey reveals a clear and growing trend: AI tools are quickly becoming part of the car buying process for a significant portion of consumers. Here are the standout findings:

1 in 4 Car Buyers Use AI

25% of car buyers in 2025 say they used or plan to use AI tools like ChatGPT during the shopping or buying process. This contrasts with a recent survey by Elon University that found 52% of Americans now use AI large language models. While signs point towards increased adoption of AI tools, the CarEdge survey found that most car buyers are still in the early stages of integrating these tools into high-stakes decisions like vehicle purchases. This suggests there’s still significant room for growth in AI adoption amongst car buyers.

AI Use Is Accelerating

Among those who haven’t bought a car yet this year, 40% say they are using or plan to use AI tools during their search or deal-making. This is nearly 3x higher than the 14% seen among those who already bought a car earlier in the year.

AI Tools Deliver Results

Among those who used AI:

88% say the tools were helpful

32% found them very helpful

60% used them “a lot” during the process

The AI Holdouts: Drivers Who Lease

Of the respondents who had already leased a car in 2025, none reported using any AI tools.

The AI-Adopting Buyer: Who’s Using It, and How?

AI adoption among car buyers is still in its early stages, but clear trends are beginning to emerge.

Among Buyers Who Already Purchased in 2025:

Just 14% of those who already bought a vehicle this year used AI tools during the process. Adoption rates were nearly identical across new and used buyers, with 14% in each group saying they used AI tools.

Among Future Car Buyers:

The numbers jump significantly when looking at those who haven’t yet bought in 2025. Among this group — who represent 39% of total respondents — 40% say they either already use or plan to use AI tools during their car search and buying process.

That’s more than triple the current usage rate among recent buyers, suggesting AI adoption is accelerating as awareness grows and tools become easier to use.

This group also appears to be more proactive: 60% of those who used AI tools during their buying journey said they used them “a lot,” while 40% used them only occasionally.

What Car Buyers Are Using AI Tools

AI tools are quickly becoming essential research companions for car shoppers looking to make more informed, confident decisions. After all, why go it alone when a wealth of automotive knowledge powered by large language models (LLMs) is right in your pocket?

Among buyers who used AI tools during their car purchase or lease process, here’s how they put them to work:

88% — Researching Vehicles

The most common use by far, AI tools helped buyers learn about different models, trims, features, and reliability. For many, it was like having an always-available expert to explain the pros and cons of their options.

64% — Comparing Prices and Market Values

Buyers used AI to better understand fair pricing, from invoice pricing to out-the-door.

44% — Learning Negotiation Strategies

Nearly half of AI users leaned on these tools to prepare for conversations with salespeople. Whether role-playing negotiation scenarios or asking how to spot add-on fees, this group used AI to level the playing field at the dealership.

11% — Exploring Finance and Lease Options

A much smaller portion of buyers used these tools to become familiar with leasing vs. financing, how to calculate payments, and similar queries.

Industry Implications

Car buying has always been tilted in favor of the dealership. Information asymmetry — what the dealer knows versus what the customer knows — has long been the source of consumer frustration, confusion, and overpayment.

That dynamic is beginning to shift.

This survey confirms what many in the industry are only starting to realize: AI is giving car buyers the upper hand. Tools like ChatGPT are helping consumers cut through the noise, ask smarter questions, and avoid common dealership traps. Instead of relying on guesswork or scattered advice, buyers are turning to AI for fast, personalized guidance at every step.

But one auto industry veteran has words of caution for buyers relying heavily on AI tools.

“It’s both surprising and a little scary to see how quickly people are turning to AI to guide such a major financial decision,” said Ray Shefska, Co-Founder of CarEdge. “While tools like ChatGPT can be powerful, they’re only as good as the data behind them. AI should complement your research, not replace your own critical thinking.“

That perspective underscores the real takeaway of this report: AI works best when it’s used thoughtfully as a tool, not as a crutch. In an age where automation raises fears of job loss or decision-making without human oversight, this survey offers a more optimistic view — one where technology helps everyday consumers make smarter choices. Used wisely, AI can help level the playing field and bring more transparency and fairness to the car buying experience.

Methodology

This survey was conducted by CarEdge between June 19 and June 24, 2025. A total of 500 U.S. respondents participated, recruited through the CarEdge email newsletter and social media channels. Questions were tailored based on buying status to better understand how and when AI tools were used in the car shopping process.

For the Silo, Karen Hayhurst.

About CarEdge Founded in 2019 by father-and-son team Ray and Zach Shefska, CarEdge is a leading platform dedicated to empowering car shoppers with free expert advice, in-depth market insights, and tools to navigate every step of the car-buying journey. From researching vehicles to negotiating deals, CarEdge helps consumers save money, time, and hassle, hundreds of thousands of happy consumers have used CarEdge to buy their car with confidence. With trusted resources like the CarEdge AI Negotiator tool, Research Center, Vehicle Rankings and Reviews, and hundreds of guides on YouTube, CarEdge is redefining transparency and fairness in the automotive industry. Follow them on YouTube, TikTok, X, Facebook, and Instagram for actionable car-buying tips and market insights. Learn more at www.CarEdge.com.

October, 2025 – Canada has world-class strength in AI research but continues to fall short in widespread adoption, according to a new report from the C.D. Howe Institute. On the heels of the federal government’s announcement of a new AI Strategy Task Force, the report highlights the urgent need to bridge the gap between research excellence and real-world adoption.

In “AI Is Not Rocket Science: Ideas for Achieving Liftoff in Canadian AI Adoption,” Kevin Leyton-Brown, Cinda Heeren, Joanna McGrenere, Raymond Ng, Margo Seltzer, Leonid Sigal, and Michiel van de Panne note that while Canada ranks second globally in top-tier AI researchers and first in the G7 for per capita publications, it is only 20th in AI adoption among OECD countries. “This matters for the economy as a whole, because such knowledge translation is a key vehicle for productivity growth,” the authors say. “It is terrible news, then, that Canada experienced almost no productivity growth in the last decade, compared with a rate 15 times higher in the United States.”

The authors argue that new approaches to knowledge translation are needed because AI is not “rocket science”: instead of focusing on a single industry sector, the discipline develops general-purpose technology that can be applied to almost anything. This makes it harder for Canadian firms to find the right expertise and for academics to sustain ties with industry. Existing approaches – funding academic research, directly subsidizing industry efforts through measures such as SR&ED and superclusters, and promoting partnerships through programs like Mitacs and NSERC Alliance – have not solved the problem.

Four ideas to help firms leverage Canadian academic strength to fuel their AI adoption include: a concierge service to match companies with experts, consulting tied to graduate student scholarships, “research trios” that link AI specialists with domain experts and industry, and a major expansion of AI training from basic literacy to dedicated degrees and continuing education. Drawing on their experiences at the University of British Columbia, the authors show how local initiatives are already bridging gaps between academia and industry – and argue these models should be scaled nationally.

“Canada’s unusual strength in AI research is an enormous asset, but it’s not going to translate into real-world productivity gains unless we find better ways to connect AI researchers and industrial players,” says Kevin Leyton-Brown, professor of computer science at the University of British Columbia and report co-author. “The challenge is not that AI is too complicated – it’s that it touches everything. That means new models of partnership, new incentives, and new approaches to education.”

AI Is Not Rocket Science- 4 Ideas in Detail

Idea 1: A Concierge Service for Matchmaking

We have seen that it is hard for industry partners to know who to contact when they want to learn more about AI. Conversely, it is at least as hard for AI experts to develop a broad enough understanding of the industry landscape to identify applications that would most benefit from their expertise. Given the potential gains to be had from increasing AI adoption across Canadian industry, nobody should be satisfied with the status quo.

We argue that this issue is best addressed by a “concierge service” that industry could contact when seeking AI expertise. While matchmaking would still be challenging for the service itself, it could meet this challenge by employing staff who are trained in eliciting the AI needs of industry partners, who understand enough about AI research to navigate the jargon, and who proactively keep track of the specific expertise of AI researchers across a given jurisdiction. This is specialized work that not everyone could perform! However, many qualified candidates do exist (e.g., PhDs in the mathematical sciences or engineering). Such staff could be funded in a variety of different ways: for example, by an AI institute; a virtual national institute focused on a given application area; a university-level centre like UBC’s Centre for Artificial Intelligence Decision-making and Action (CAIDA); a nonprofit like Mitacs; a provincial ministry for jobs and economic growth; or the new federal ministry of Artificial Intelligence and Digital Innovation.

Having set up an organization that facilitates matchmaking, it could make sense for the same office to provide additional services that speed AI adoption, but that are not core strengths of academics. Some examples include project management, programming, AI-specific skills training and recruitment, and so on. Overall, such an organization could be funded by some combination of direct government support, direct cost recovery, and an overhead model that reinvests revenue from successful projects into new initiatives.

Idea 2: Consultancy in Exchange for Student Scholarships

Many businesses that would benefit from adopting AI do not need custom research projects and do not want to wait a year or more to solve their problems. The lowest-hanging fruit for Canadian AI adoption is ensuring that industry is well informed about potentially useful, off-the-shelf AI technologies. We thus propose a mechanism under which AI experts would provide limited, free consulting to local industry. AI experts would opt in to being on a list of available consultants. A few hours of advice would be free to each company, which would then have the option of co-paying for a limited amount of additional consulting, after which it would pay full freight if both parties wanted to continue. The company would own any intellectual property arising from these conversations, which would thus focus on ideas in the public domain. If the company wanted to access university-owned IP, it could shift to a different arrangement, such as a research contract. This system would work best given a concierge service like the one we just described. The value offered per consulting hour clearly depends on the quality of the academic–industry match, and some kind of vetting system would be needed to ensure the eligibility of industry participants.

Why would an AI expert sign up to give advice to industry? All but the best-funded Canadian faculty working in AI report that obtaining enough funding to support their graduate students is a major stressor. Attempting to establish connections with industry is hard work, and such efforts pay off only if the industry partner signs on the dotted line and matching funds are approved. There is thus space to appeal to faculty with a model in which they “earn” student scholarships for a fixed amount of consulting work. For example, faculty could be offered a one- semester scholarship for every eight hours set aside for meetings with industry, meaning that one weekly “industry office hour” would indefinitely fund two graduate students. Consulting opportunities could also be offered directly to postdoctoral fellows or senior (e.g., post-candidacy) PhD students in exchange for fellowships. In such cases, trainees should be required to pass an interview, certifying that they have both the technical and soft skills necessary to succeed in the consulting role. The concierge service could help decide which industry partners could be routed to PhD students and which need the scarcer consulting slots staffed by faculty members.

The system would offer many benefits. From the industry perspective, it would make it straightforward to get just an hour or two of advice. This might often be enough to allow the company to start taking action towards AI adoption: there is a rich ecosystem of high-performance, reliable, and open-source AI tools; often, the hard part is knowing what tool to use in what way. Beyond the value of the advice itself, consulting meetings offer a strong basis for building relationships between academics and industry representatives, in which the academic plays the role of a useful problem solver rather than of a cold-calling salesperson. These relationships could thus help to incubate Mitacs/Alliance-style projects when research problems of mutual interest emerge (though also see our idea below about how restructuring such projects could help further).

For academics, the system would constitute a new avenue for student funding that would reward each hour spent with a predictable amount of student support. Furthermore, it would offer scaffolded opportunities to deepen connections with industry. The system would come with no reporting requirements beyond logging the time spent on consulting. The faculty member would be free to use earned scholarships to support any student (regardless, for example, of the overlap between the student’s research and the topics of interest to companies), increasing flexibility over the Mitacs/Alliance system, in which specific students work with industry partners. Students who self-funded via consulting would learn valuable skills and would expand their professional networks, improving prospects for post-graduation employment.

Finally, the system would also offer multiple benefits from the government’s perspective. It would generate unusually high levels of industrial impact per dollar spent (consider the number of contact hours between academia and industry achieved per dollar under the funding models mentioned in Section 3). All money would furthermore go towards student training. The system would automatically allocate money where it is most useful, directing student funding to faculty who are both eager to take on students and relevant to industry, all without the overhead of a peer-review process. And it would generate detailed impact reports as a side effect of its operations, since each hour of industry–academia contact would need to be logged to count towards student funding.

Idea 3: Grants for Research Trios

Our third proposal is an approach for expanding the Mitacs/Alliance model to make it work better for AI. Industry–academia partnerships leverage two key kinds of expertise from the academic side: methodological know-how for solving problems and knowledge about the application domain used for formulating such problems in the first place. In fields for which the set of industry partners is relatively small and relatively stable, it makes sense to ask the same academics to develop both kinds of expertise. In very general-purpose domains like AI, it holds back progress to ask AI experts to become domain experts, too. Instead, it makes sense to seek domain knowledge from other academics who already have it. We thus propose a mechanism that would fund “research trios” rather than bilateral research pairings. Each trio would contain an AI expert, an academic domain expert, and an industry partner. This approach capitalizes on the fact that there is a huge pool of academic talent outside core AI with deep disciplinary knowledge and a passion for applying AI. While such researchers are typically not in a position to deeply understand cutting-edge AI methodologies, they are ideally suited to serve as a bridge between researchers focused on AI methodologies and Canadian industrial players seeking to achieve real-world productivity gains. In our experience at UBC, the pool of non-AI domain experts with an interest in applying AI is considerably larger than the pool of AI experts. One advantage of this model is that projects can be initiated by the larger population of domain experts, who are also more likely to have appropriate connections to industry. Beyond this, involving domain experts increases the likelihood that a project will succeed and gives industry partners more reason to trust the process while a solution is being developed. The model meets a growing need for funding researchers outside computer science for projects that involve AI, rather than concentrating AI funding within a group of specialists. At the same time, it avoids the pitfall of encouraging bandwagon-jumping “applied AI” projects that lack adequate grounding in modern AI practices. Finally, it not only transfers AI knowledge to industry, but also does the same to both the domain expert and their students.

Idea 4: Greatly Expanded AI Training

As AI permeates the economy, Canada will face an increasing need for AI expertise. Today, that training comes mostly in the form of computer science degrees. Just as computer science split off from mathematics in the 1960s, AI is emerging today as a discipline distinct from computer science. In part, this shift is taking the form of recognizing that not every AI graduate needs to learn topics that computer science rightly considers part of its core, such as software engineering, operating systems, computer architecture, user interface design, computer graphics, and so on. Conversely, the shift sees new topics as core to the discipline. Most fundamental is machine learning. Dedicated training in AI will require a deeper focus on the mathematical foundations of probability and statistics, building to advanced topics such as deep learning, reinforcement learning, machine learning theory, and so on. Various AI modalities also deserve separate study, such as computer vision, natural language processing, multiagent systems, robotics, and reasoning. Training in ethics, optional in most computer science programs, will become essential.

Beyond dedicated training in the core discipline, we anticipate huge demand for broad-audience AI literacy training; for AI minors to complement other disciplinary specializations; for continuing education and “micro-credential” programs; and for executive education in AI. There is also a growing need for “AI Adoption Facilitators”: bridge-builders who can help established workers in medium-to-large organizations understand how data-driven tools could offer value in solving the problems they face. Training for this role would emphasize business principles and domain expertise, but would also require firmer foundations in machine learning and data science than are currently typical in those disciplines.

Artificial Intelligence (AI) has become an integral part of our daily lives, influencing everything from how we interact with technology to how businesses operate. But where did it all begin? Let’s take a journey through the early days of AI, exploring the key milestones that have shaped this fascinating field.

Today, AI is a rapidly evolving field with applications in various domains, including healthcare, finance, transportation, and entertainment. From virtual assistants like me, Microsoft Copilot, to autonomous vehicles and systems, AI continues to transform our world in profound ways.

A Copilot self generated image when queried “Show me what you look like”. CP

Conclusion

The journey of AI from its early conceptual stages to its current state is a testament to human ingenuity and perseverance. While the field has faced numerous challenges and setbacks, the progress made over the past few decades has been remarkable. As we look to the future, the potential for AI to further revolutionize our lives remains immense.

Did you know that, every year, home renovation projects are derailed by hidden costs, vague language, and inconsistent contractor bids—pushing 78% of jobs over budget and forcing two-thirds of homeowners into debt? It’s not just homeowners who feel the pain: contractors, property managers, real estate agents, investors, and flippers all struggle to assess and compare bids quickly and accurately.

The problem is that contractor quotes are rarely “apples to apples,” often missing critical details or disguising inflated charges—making it hard to identify true scope, cost, and risk. Now, the free-to-use and industry first BidCompareAI tool analyzes and compares multiple contractor bids, instantly identifying missing scope items, unrealistic allowances and other red flags before any work begins … often with tens of thousands of dollars on the line. In minutes, the AI generates a clear, line-by-line report that standardizes bids into transparent, actionable insights—helping homeowners avoid costly overruns, while enabling industry pros to quote with confidence, negotiate smarter, close deals faster, and protect ROI. Interest in this innovation raising industry transparency standards?

AI Reveals These Top 10 Home Renovation Bid Red Flags

First-of-its-kind free AI tool turns confusing, inconsistent contractor bids into clear, side-by-side insights—helping homeowners avoid costly overruns and enabling industry pros to quote, negotiate and close with confidence

Renovations are one of the most expensive and stressful decisions a homeowner makes. Yet 78% of projects blow their budgets, and 2 in 3 homeowners go into debt just to pay for them. Why? Because contractor bids are often riddled with hidden costs, vague language, and missing work that leave you paying more than you bargained for. Thankfully, new AI technology is now making these red flags impossible to ignore—saving homeowners thousands before a hammer is even swung. BidCompareAI is the first-ever AI tool that lets homeowners upload multiple bids and get a fast, detailed report comparing scope, pricing, and red flags—no construction expertise needed and no signup or payment required.

“Homeowners have been forced to make major financial decisions based on unclear or incomplete bids,” says GreatBuildz Co-CEO Jon Grishpul. “BidCompareAI adds instant transparency and clarity—saving people from costly mistakes before a project even starts. For contractors, property managers, and real estate professionals, it’s a credibility and efficiency tool that streamlines communication, builds trust and helps win more business.”

Here are the top 10 red flags often hiding in contractor bids, and how the BidCompareAI tool reveals them instantly:

1. Missing Scope Items — “Surprise” Costs Waiting to Blow Your Budget

Your contractor’s quote doesn’t include demolition, cleanup, or critical tasks? That’s a ticking time bomb. Now, homeowners can catch these omissions so you never get hit with surprise charges.

2. Vague Allowances — The Fine Print That Drains Your Wallet

Ambiguous line items like “fixtures” or “materials” can mean anything. The AI tool flags vague terms so you can demand specifics upfront.

3. Unrealistically Low Bids — Too Good to Be True? Usually Are

Low-ball bids often mean corners will be cut or costs will balloon later. This AI exposes these dangerously low estimates before you get stuck with change orders.

4. Pricing Inconsistencies — Comparing Apples to Oranges?

Quotes come in all formats with wildly different terminology. This advanced technology standardizes and compares them side-by-side, so you’re not left guessing.

5. Hidden Fees — The Black Box of Renovation Budgets

Permits, procurement, and labor fees sometimes get lumped in mysteriously. The AI reveals these “hidden” charges clearly in its summary report.

6. Overlapping or Duplicate Charges — Paying Twice Without Knowing It

Some bids unknowingly charge for the same work twice. The AI delivers a line-by-line analysis that spots these costly errors fast.

7. Unclear Project Timelines — When Delays Lead to Extra Costs

Vague or missing timelines can spiral into costly delays. While timelines aren’t priced, spotting missing info helps you demand accountability.

8. Missing Cleanup and Disposal — Don’t Get Stuck with the Mess

Quotes that don’t include cleanup leave you responsible for hauling debris and disposing of waste. This AI highlights these crucial omissions.

9. Discrepancies in Material Quality — Low-Quality Where You Expected Premium

One bid may specify high-end fixtures while another hides “allowances” that could mean anything. The AI tool flags these differences so you know exactly what you’re paying for.

10. Inconsistent Labor Charges — Watch for Inflated or Unexplained Fees

Labor costs vary widely, and some bids overcharge or include unnecessary markups. This user-friendly technology points out these red flags clearly.

“This is about more than just tech,” added Paul Dashevsky, Co-CEO of GreatBuildz. “It’s about empowering homeowners to feel confident and in control of their renovation projects—and helping contractors better serve their clients.”

Renovations don’t have to be a financial nightmare. As consumer-facing AI tools proliferate across industries, the BidCompareAI innovation demonstrates how artificial intelligence can bring real-world value by making complex, high-stakes decisions—like selecting the right contractor—faster, clearer and far less stressful. For the Silo, Marsha Zorn.

Artificial Intelligence (AI) has infiltrated our lives for decades, but since the public launch of ChatGPT showcasing generative AI in 2022, society has faced unprecedented technological evolution.

With digital technology already a constant part of our lives, AI has the potential to alter the way we live, work, and play – but exponentially faster than conventional computers have. With AI comes staggering possibilities for both advancement and threat.

The AI industry creates unique and dangerous opportunities and challenges. AI can do amazing things humans can’t, but in many situations, referred to as the black box problem, experts cannot explain why particular decisions or sources of information are created. These outcomes can, sometimes, be inaccurate because of flawed data, bad decisions or infamous AI hallucinations. There is little regulation or guidance in software and effectively no regulations or guidelines in AI.

How do researchers find a way to build and deploy valuable, trusted AI when there are so many concerns about the technology’s reliability, accuracy and security?

That was the subject of a recent C.D. Howe Institute conference. In my keynote address, I commented that it all comes down to software. Software is already deeply intertwined in our lives, from health, banking, and communications to transportation and entertainment. Along with its benefits, there is huge potential for the disruption and tampering of societal structures: Power grids, airports, hospital systems, private data, trusted sources of information, and more.

Consumers might not incur great consequences if a shopping application goes awry, but our transportation, financial or medical transactions demand rock-solid technology.

The good news is that experts have the knowledge and expertise to build reliable, secure, high-quality software, as demonstrated across Class A medical devices, airplanes, surgical robots, and more. The bad news is this is rarely standard practice.

As a society, we have often tolerated compromised software for the sake of convenience. We trade privacy, security, and reliability for ease of use and corporate profitability. We have come to view software crashes, identity theft, cybersecurity breaches and the spread of misinformation as everyday occurrences. We are so used to these trade-offs with software that most users don’t even realize that reliable, secure solutions are possible.

With the expected potential of AI, creating trusted technology becomes ever more crucial. Allowing unverifiable AI in our frameworks is akin to building skyscrapers on silt. Security and functionality by design trump whack-a-mole retrofitting. Data must be accurate, protected, and used in the way it’s intended.

Striking a balance between security, quality, functionality, and profit is a complex dance. The BlackBerry phone, for example, set a standard for secure, trusted devices. Data was kept private, activities and information were secure, and operations were never hacked. Devices were used and trusted by prime ministers, CEOs and presidents worldwide. The security features it pioneered live on and are widely used in the devices that outcompeted Blackberry.

Innovators have the know-how and expertise to create quality products. But often the drive for profits takes precedence over painstaking design. In the AI universe, however, where issues of data privacy, inaccuracies, generation of harmful content and exposure of vulnerabilities have far-reaching effects, trust is easily lost.

So, how do we build and maintain trust? Educating end-users and leaders is an excellent place to start. They need to be informed enough to demand better, and corporations need to strike a balance between caution and innovation.

Companies can build trust through a strong adherence to safe software practices, education in AI evolution and adherence to evolving regulations. Governments and corporate leaders can keep abreast of how other organizations and countries are enacting policies that support technological evolution, institute accreditation, and financial incentives that support best practices. Across the globe, countries and regions are already developing strategies and laws to encourage responsible use of AI.

Recent years have seen the creation of codes of conduct and regulatory initiatives such as:

The Bletchley Declaration, Nov. 2023, an international agreement to cooperate on the development of safe AI, has been signed by 28 countries;

US President Biden’s 2023 executive order on the safe, secure and trustworthy development and use of AI; and

Governing AI for Humanity, UN Advisory Body Report, September 2024.

We have the expertise to build solid foundations for AI. It’s now up to leaders and corporations to ensure that much-needed practices, guidelines, policies and regulations are in place and followed. It is also up to end-users to demand quality and accountability.

Now is the time to take steps to mitigate AI’s potential perils so we can build the trust that is needed to harness AI’s extraordinary potential. For the Silo, Charles Eagan. Charles Eagan is the former CTO of Blackberry and a technical advisor to AIE Inc.

With AI reshaping everything from finance to fast food, the $1.5T auto retail industry is finally facing its overdue disruption. The typical car-buying experience—riddled with hidden fees, lead bloat, pricing games and low trust—has remained stubbornly analog. But now, with 90% of dealerships in America (and growing % in Canada and Mexico) experimenting with AI tools and 1 in 4 buyers already using AI to shop, the tide is turning. Agentic AI technology is fundamentally reshaping one of the most significant purchases in a person’s life.

Zach Shefska, Co-Founder and CEO of CarEdge, asserts that agentic AI is the key to rebuilding trust, removing friction and leveling the playing field for both buyers and sellers. From AI-powered shopping assistants that negotiate on your behalf, to data tools that reveal deceptive dealership practices, Shefska is a pioneer in “agentic AI” — a new form of artificial intelligence bringing much-needed transparency to the industry.

The Broken Status Quo: Car buying is frustrating and inefficient for both consumers and dealerships—highlighting key stats like 72% sales staff turnover and 2% lead conversion from third-party platforms.

Lead Generation Platforms Are Failing: Legacy systems flood dealers with unqualified leads, drain resources, and deliver minimal value to consumers.

The Rise of Agentic AI in Auto Retail: Consumers are turning to tools like ChatGPT and CarEdge’s AI agent to navigate purchases with more confidence, speed, and clarity—25% are already doing it.

From Friction to Fluidity: Agentic AI replaces quantity with quality—streamlining the buyer’s journey, reducing information overload, and improving dealer efficiency.

The End of Pricing Games: AI tools now collect and publish out-the-door pricing from thousands of dealerships, exposing hidden fees and rewarding transparent sellers.

The Future of Negotiation: AI agents can negotiate on behalf of both buyers and sellers—minimizing stress, cutting transaction times from days to hours, and removing the adversarial edge.

Real-World Impact Stories: One buyer saved $1,280 and hours of back-and-forth using CarEdge’s agentic AI—illustrating AI’s practical value in real-life scenarios.

AI Helps Honest Dealers Win: In a trust-starved industry, AI gives reputable dealers a new way to stand out by offering full transparency and faster deals.

What’s Next for AI in Auto Retail: The emerging frontier: AI agents dynamically collecting and updating real-time pricing and inventory data across markets to offer true market intelligence.

For the Silo, Zach Shefska. Zach is CEO of CarEdge, a leading platform—founded by father-and-son team Ray and Zach Shefska—dedicated to empowering car shoppers with free expert advice, in-depth market insights and tools to navigate every step of the car-buying journey. From researching vehicles to negotiating deals, CarEdge helps consumers save money, time and hassle. Alsop with trusted resources like the CarEdge Research Center, Vehicle Rankings and Reviews, and hundreds of guides on YouTube, CarEdge is redefining transparency and fairness in the automotive industry. Connect with Shefska at www.CarEdge.com or on social media on YouTube, TikTok, X, Facebook, and Instagram.

Canada is great at AI development, but what should the country’s first Minister for Artificial Intelligence make his key priorities? University of Waterloo’s Anindya Sen and the C.D Howe Institute’s Rosalie Wyonch offer strong insight — and geek out a bit about the economics-oriented nature of machine learning algorithms.

Hello AI Tinkerers and welcome to the latest Sci-Tech article here at The Silo. Get ready, You will want to pay attention because the spotlight is on this Dude because he knows how to get around ‘bad ai prompting’. Just recently, he has helped spin out 40 startups using one core skill. Can you guess which one? Yep. Prompting.

In the One-Shot video below, Kevin Leneway breaks down his real workflow for shipping AI products fast — using markdown checklists, agent coding, rubric-based UI design, and zero Figma.

“I don’t need Figma. I just prompt my way to a working front end.” — Kevin Leneway

While most people are still asking ChatGPT to write code snippets, Kevin is building full-stack products using nothing but prompts. In this One-Shot episode, he reveals the exact system he’s used to launch over 40 startups at Pioneer Square Labs. We break down:

How he writes BRDs and PRDs that don’t suck

Why vibe coding fails and how to actually use AI agents

The markdown checklist that replaces a product team

How to go from idea to working app with zero context switching

His open-source starter kit that makes Cursor and Claude 3.5 feel like magic

“I’ve helped launch six startups including Singlefile (singlefile.io, $24M raised), Recurrent (recurrentauto.com, $24M raised), Joon (joon.com, $9.5M raised), Gradient (gradient.io, $3.5M raised), Genba (genba.ai, acquired May 2022) and Enzzo (enzzo.ai, $3M raised).”

If you’re a builder, this will change how you work. No gimmicks. Just a ruthless focus on speed, clarity, and shipping. Watch now. Learn the system. Steal it. For the Silo, Joe at aitinkerers.org

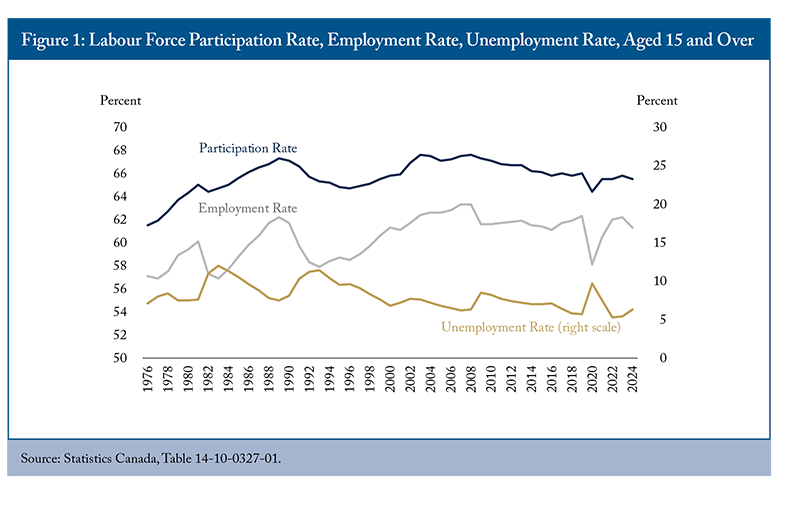

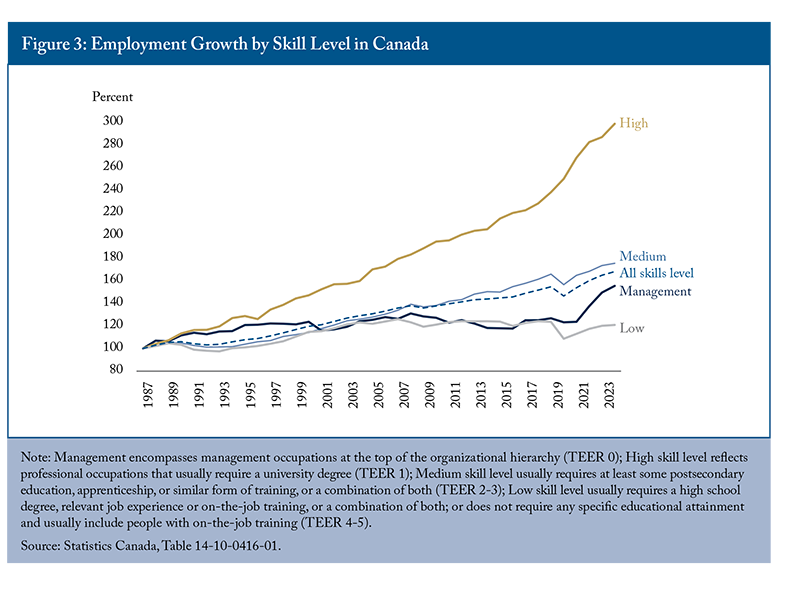

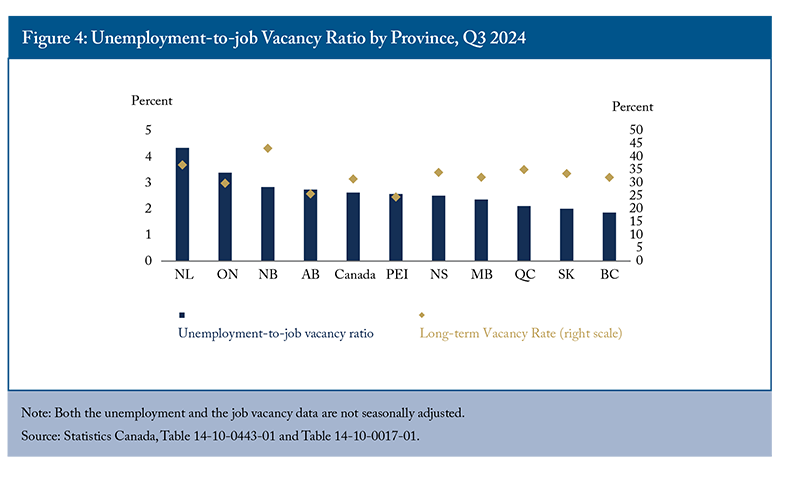

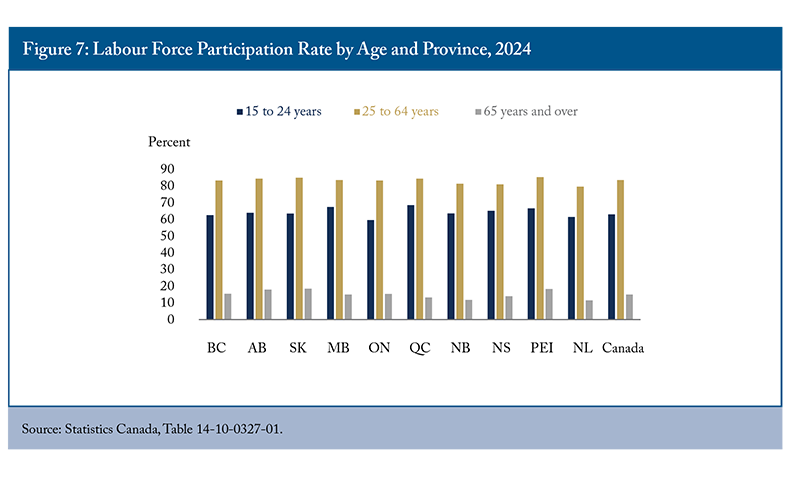

In 2024, Canada’s labour market showed modest growth, with job creation continuing but lagging rapid population growth. This led to an increase in the unemployment rate, reflecting a mismatch between labour force expansion and job creation rather than a decline in sector-specific labour shortages.

Ongoing challenges persist, such as declining labour productivity, sector-specific labour shortages, underemployment, demographic shifts and disparities, and regional imbalances.

Our international comparisons show that Canada typically ranks at or below the Organisation for Economic Co-operation and Development (OECD) average in terms of labour force participation and employment rates for certain population segments. This is largely due to weaker performance in specific regions, such as the Atlantic provinces, and pension policies that incentivize early retirement.

This labour market review emphasizes the need for tailored policies to improve labour market outcomes for seniors and immigrants. Recommendations include gradually increasing the retirement age, offering high-quality training support, and easing labour mobility barriers.

Introduction

The labour market is where economic changes most directly affect working-age Canadians, influencing their job opportunities and income. The supply of labour also determines the availability of Canadians’ skills and knowledge to employers who combine them with capital to produce goods and services that drive our national income and its distribution among income classes. Therefore, the labour market is one of the most important components of Canada’s – or any – economy.

In 2024, Canada’s labour market saw moderate growth, with employment rising to 20.7 million jobs. However, the employment rate declined to 61.3 percent, down from 62.2 percent in 2023, and remains below the pre-pandemic level of 62.3 percent in 2019. While over 1.7 million employed persons have been added since 2019, employment growth has lagged behind population growth, partly due to an aging population, despite high levels of immigration.1 The unemployment rate also increased, reflecting a gap between job creation and labour force expansion, partly due to limited absorptive capacity to keep pace with population growth.

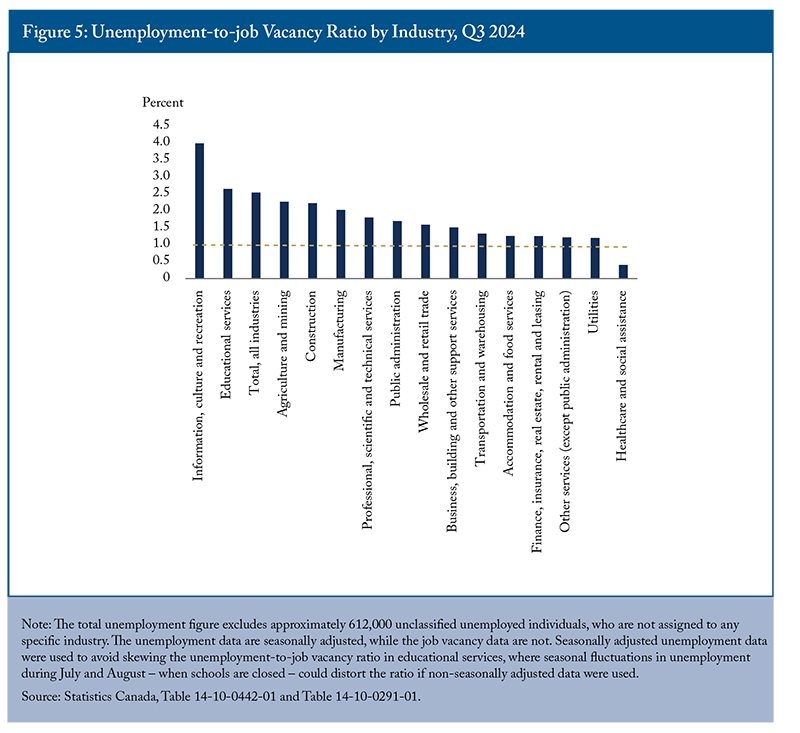

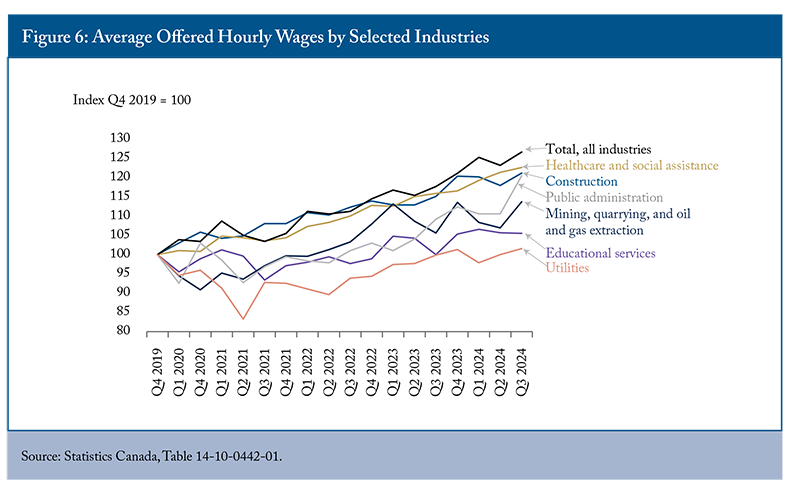

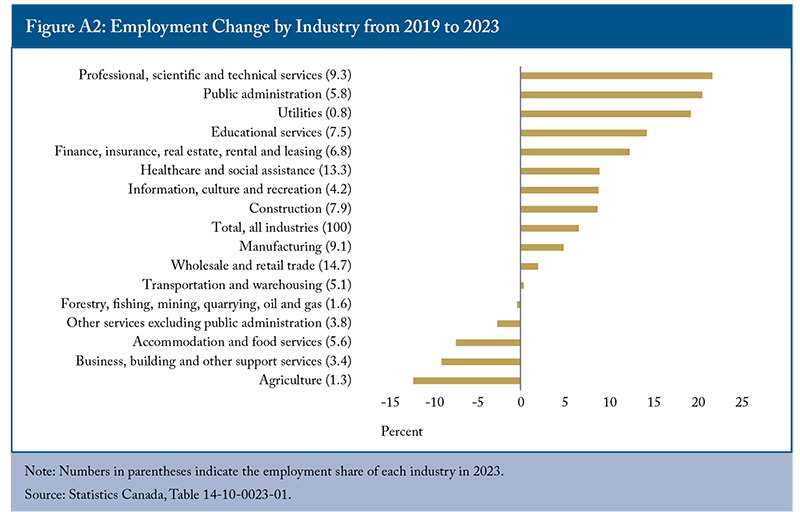

Job vacancies have decreased since mid-2022, but over half a million positions remained unfilled during the third quarter of 2024 (12 percent higher than the pre-pandemic level). Of these vacancies, the majority were full-time (432,810 positions), with more than 31 percent remaining vacant for the long term – persisting for over 90 days. Despite high full-time vacancies, more than half a million workers were underemployed in 2024, seeking full-time work while employed part-time, indicating mismatches between the skills needed by employers and the skills offered by job seekers. Among sectors facing labour shortages, factors such as better relative wages and working conditions appear to be helping, particularly in industries like construction. Healthcare, on the other hand, may benefit from raising wages and reducing training costs to better attract and retain workers.

Further, Canada faces declining labour productivity, which can be attributed to factors such as stagnant capital investment and automation, high reliance on temporary foreign workers to fill low-paying positions, underemployment (including immigrants’ overqualification), a growing public sector with lower productivity, and shifts in industry composition.

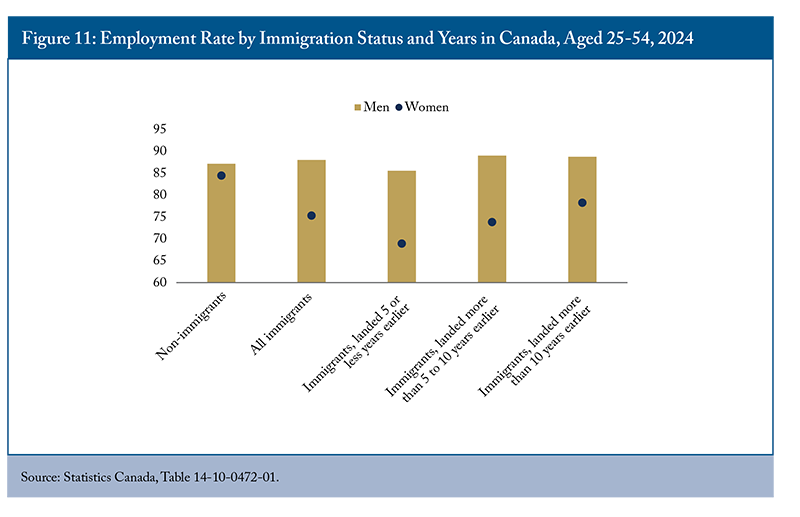

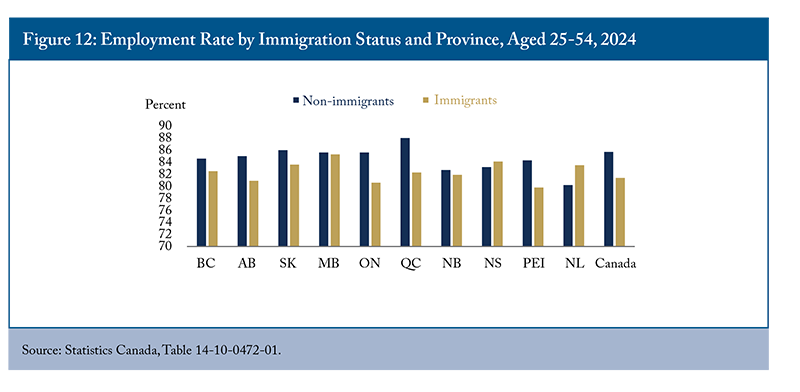

This inaugural C.D. Howe Institute labour market review highlights major differences in the labour market across provinces and sectors and among socio-economic groups. It shows that labour force participation and employment of older workers and recent immigrants still have room for improvement.

Canada needs targeted workforce development policies to improve labour market participation and outcomes for diverse population groups and encourage a longer working life (Holland 2018 and 2019). Our recommendations are to:

Gradually raise the normal retirement age from 65 to 67 and delay pension access.

Support older workers with flexible work, part-time options, and self-employment, especially in the Atlantic provinces.

Invest in high-quality training programs for underrepresented groups, focusing on digital skills and job search strategies.

Streamline credential recognition and licensure for skilled immigrants and ease labour mobility in regulated occupations while maintaining the quality of professional services.

Enhance settlement strategies for immigrants, including workplace-focused language training.

Businesses should integrate automation and artificial intelligence (AI) to boost productivity while improving retention and encouraging later retirement by offering training2 and flexible scheduling (Mahboubi and Zhang 2023).Finally, better informing Canadians about learning and training opportunities and addressing financial and non-financial barriers would improve their training participation rates and empower them to acquire the skills needed in a changing labour market.

Overview of Canada’s Labour Market

Canada’s labour market has undergone major changes over time, influenced by factors such as the COVID-19 pandemic, globalization, technological progress, and demographic shifts. These forces have affected the functioning of the labour market, with demographic changes playing a particularly important role. This section reviews key indicators (i.e., labour-force participation, employment and unemployment) and highlights the major trends and disparities in provincial and national labour markets.

The labour force has grown steadily since 1976 but experienced a decline in 2020 due to the pandemic. The lockdowns and public health measures significantly reduced worker participation, especially among women, in the labour market. However, once the restrictions were lifted, workers returned, and the labour force fully recovered. By 2024, Canada had 22.1 million people in the labour force, an increase of about 1.9 million from 2019, mainly driven by the expansionary immigration policy that the country has followed until recently.3 Immigrants accounted for 56 percent of this increase in the labour force, while non-permanent residents made up 32 percent.4

Although the labour force has grown over time, the labour force participation rate (LFPR) has trended downward over the last two decades. This trend is largely driven by an aging population, as participation rates drop sharply after age 54 and continue to decline with age. While the LFPR among prime-aged workers (25-54) reached a record high in 2023, the overall rate remained below pre-pandemic levels and declined further in 2024, reaching 65.5 percent despite high levels of immigration.5 Three factors contributed to this decline compared to pre-pandemic levels: a lower participation rate among youth, a substantial increase in the older population (aged 55 and over) and a decline in the latter group’s participation rate. This decline in older workers’ participation is primarily due to aging, as the proportion of seniors aged 65 and over within the 55-and-over age group increased from 54.8 percent in 2019 to 60 percent in 2024.