Michigan-Based Humanitarian Organization, Life for Relief and Development (LIFE), Helps Put a Book in Every Child’s Hand at Ontario School

Centuries after books first became humanity’s primary means of preserving knowledge, they continue to offer something technology alone cannot: the space to reflect, question, imagine, and think deeply. As our world is increasingly shaped by instant answers, AI-generated content, endless notifications, and shrinking attention spans, the ability to engage with long-form content and complex ideas may be more valuable than ever.

Reading researchers have repeatedly found that reading on paper often leads to stronger comprehension and retention than reading the same material digitally, particularly when students engage with longer and more complex texts. Recent systematic reviews likewise suggest that print reading supports deeper engagement and comprehension, particularly when students are working with longer or more cognitively demanding texts.

As concerns grow over academic achievement, rising screen time, and the increasing use of artificial intelligence by students, educators across North America are confronting difficult questions about how to prepare the next generation for the future.

Life for Relief and Development (LIFE) is a U.S.-based humanitarian organization that has served vulnerable communities in more than 60 countries for over three decades. They believe that books and educational support are among the most valuable tools we can give future generations.

LIFE recently delivered thousands of educational resources to Al-Taqwa School in London, Ontario. The shipment included reading and writing materials, literature anthologies, teacher editions, and textbooks for students from kindergarten through Grade 8.

According to Neil, principal of Al-Taqwa School, the school first received educational books through LIFE more than a decade ago. Those resources served students for years before a new shipment arrived. Beginning in 2016, LIFE also provided school furniture to support the school’s growing educational needs, helping create learning spaces where students could learn, collaborate, and thrive.

The longevity of those earlier donations speaks not only to the quality of the resources but also to the enduring value of educational investments that continue benefiting students long after they are delivered.

When the newest shipment arrived, teachers immediately recognized the difference it would make. For years, educators often relied on shared resources, photocopies, and creative workarounds to stretch classroom materials. The arrival of additional books meant students could finally have direct access to the materials they needed.

According to Neil, the new shipment meant there was finally “a book in every child’s hand.”

That statement carries added significance at a time when screens occupy an increasingly large role in children’s lives. Canadian health guidelines recommend no more than two hours of recreational screen time per day for school-aged children and youth, yet studies consistently show many exceed that amount by several hours. Researchers have linked excessive screen use to lower academic performance, reduced attention spans, poorer sleep quality, and decreased reading engagement.

Technology undoubtedly has a place in modern education. Digital tools provide access to information, research opportunities, and new ways of learning. However, what we are seeing in many schools is the complete replacement of books with items like Chromebooks and other screen-based devices.

The arrival of new classroom books from LIFE allowed teachers at Al-Taqwa to spend less time on screens, managing textbook shortages, and more time focusing on instruction, mentorship, and student growth.

Al-Taqwa School is concerned not only with what students learn but also with who they become. School leaders emphasize character, responsibility, leadership, and personal development alongside academic achievement. Quality educational resources support those goals by helping teachers create classroom experiences that foster curiosity, intellectual engagement, and a lifelong appreciation for learning.

Life for Relief and Development (LIFE) holds the philosophy that knowledge creates opportunity. The organization’s educational initiatives extend far beyond Ontario. In communities around the world, LIFE supports education through large book shipments, scholarships, educational supplies, building schools, and learning opportunities that help children continue their studies despite poverty, conflict, or displacement. In Gaza, for example, LIFE has supported educational spaces that have helped nearly 1,000 children continue learning despite the ongoing humanitarian crisis.

“Education is one of the greatest investments we can make in the future,” said Dr. Hany Saqr, President and CEO of LIFE. “When we place quality educational resources in the hands of children, we are doing more than supporting their studies. We are helping cultivate future leaders, innovators, educators, and problem-solvers who will shape the communities and world they inherit.”

The partnership between LIFE and Al-Taqwa School reflects Dr. Saqr’s sentiment. The first books delivered through LIFE served students for more than a decade before a new generation of resources arrived. Today, those latest materials will help another generation of learners build knowledge, develop confidence, and engage more fully with their education.

Every book placed in a student’s hands represents another opportunity to learn, imagine, question, and think for themselves about the world around them. Those opportunities ultimately shape our collective future. No matter how many technological advancements we witness, books will continue to remain among the most enduring tools for cultivating knowledge, curiosity, and critical thought.

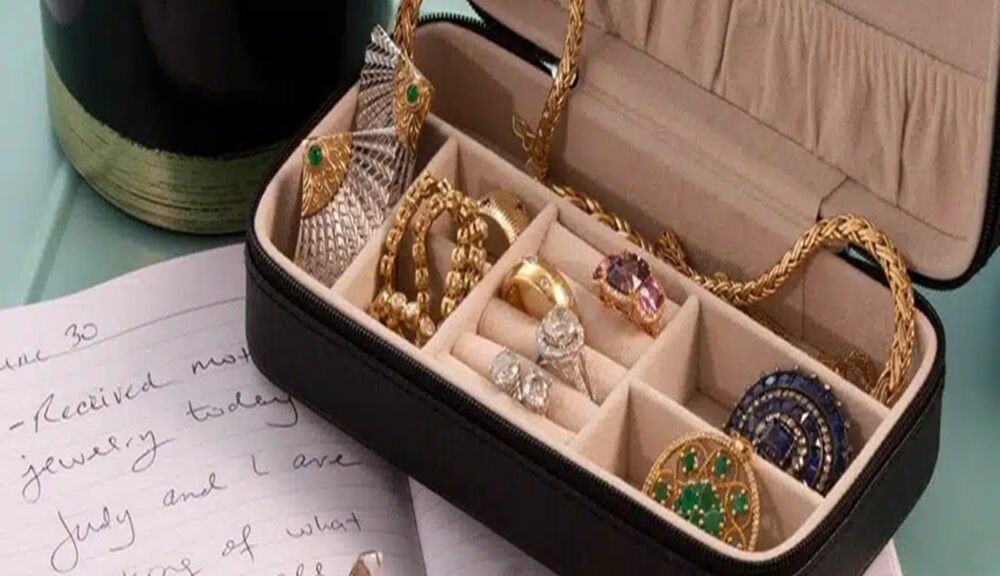

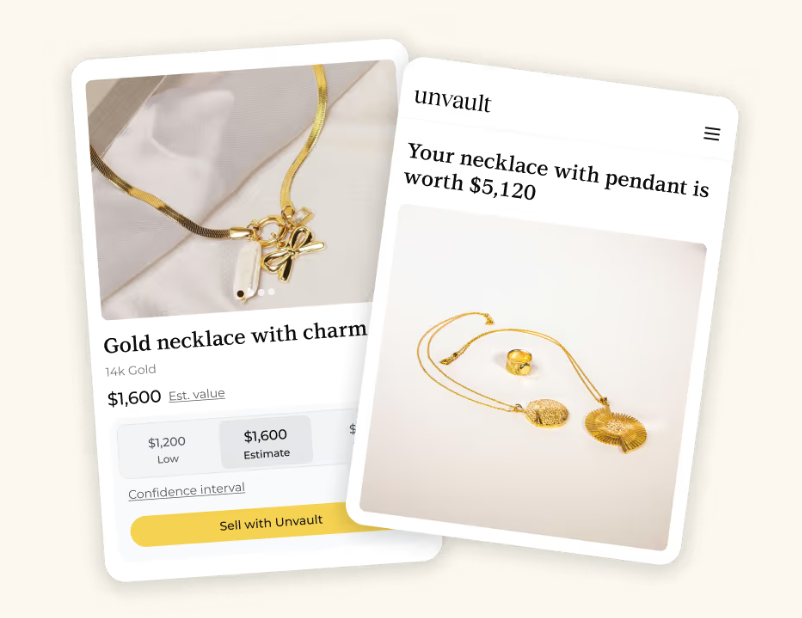

Following weaker-than-expected U.S. and Canada jobs data while gold rebounds to its highest level in weeks, more North Americans are looking around their homes for fast sources of cash … and family jewelry is increasingly becoming the first asset they choose to sell. But, consumer advocates warn that many sellers rush into pawn shops, mail-in buyers, or hotel gold-buying events without ever learning what their jewelry is actually worth, potentially leaving hundreds or even thousands of dollars behind. With gold prices climbing again and household budgets still under pressure, knowing how to value jewelry before selling has become more important than ever.

Why more North Americans are cashing in family jewelry, the biggest resale mistakes consumers make, and how AI is helping sellers avoid pawn shop pricing traps

As inflation, rising household costs, and economic uncertainty continue squeezing family budgets, many Americans are looking around their homes for quick sources of cash. One asset is suddenly attracting renewed attention: old gold and silver jewelry. With precious metal prices near record highs, consumers are increasingly selling inherited jewelry, broken chains, forgotten rings, and unused pieces to generate extra income. But experts warn that the rush to sell is also creating opportunities for lowball offers, misleading valuations, and resale scams that can cost consumers hundreds or even thousands of dollars.

Nidhi Singhvi, Co-Founder and CEO of AI-powered jewelry valuation platform Unvault, has talked extensively about how today’s jewelry resale market works, why so many consumers unknowingly accept offers far below market value, and the simple steps sellers should take before walking into a pawn shop or mailing away valuable pieces. Using AI-powered image analysis, live precious metals pricing, and transparent valuation models, Unvault helps consumers understand what their jewelry may actually be worth before deciding whether to sell. The platform was built specifically to replace the opaque appraisal process that has traditionally dominated the resale market while giving consumers more control over their financial decisions.

According to Unvault, Americans alone may be sitting on an estimated $750 billion usd to $1 trillion usd worth of gold jewelry that is largely untracked and often significantly undervalued by its owners. Add in jewelry collections from Mexican and Canadian families and the numbers get staggering.

As gold prices have climbed, consumer interest has surged, with Unvault reporting rapid growth in jewelry assets being tracked as more people seek transparent valuations before selling.

Keep the following key points in mind when considering selling

Why are soaring gold prices prompting more North Americans to sell jewelry to cover everyday expenses?

What are the biggest red flags that suggest a buyer may be dramatically undervaluing your jewelry?

Why do pawn shop offers and resale quotes vary so widely?

How do you determine whether jewelry should be sold, insured, or held as a long-term asset?

What are the common misconceptions people have about inherited, broken, or outdated jewelry?

How can AI provide a market-based jewelry valuation in under a minute using only photos?

Why should consumers know their jewelry’s value before entering any resale negotiation?

Which types of gold and silver jewelry typically retain the strongest resale value?

What are the safest ways to sell valuable jewelry while protecting against fraud and pricing manipulation?

Research which practical advice is there for maximizing resale value without falling victim to common industry pricing tactics.

Independent Palestinian Doctors Association Leads Health Initiatives to Support Vulnerable Communities in Remote Areas

As humanitarian and healthcare challenges continue to intensify across Jerusalem and the West Bank, the Independent Palestinian Doctors Association (IPDA) is advancing a comprehensive portfolio of medical, developmental, and training initiatives aimed at strengthening healthcare services, expanding access to medical care, supporting community institutions, and investing in the professional development of healthcare workers on the ground.

The Association’s vision is rooted in delivering a comprehensive response to the growing needs of Palestinian communities through programs that combine direct medical interventions, professional training, and healthcare infrastructure support. These efforts contribute to strengthening community resilience, improving the quality of healthcare services, supporting both governmental and non-governmental healthcare sectors, and advancing Palestine’s healthcare system through medical fellowship programs and the provision of modern medical technologies and equipment.

Mobile Medical Clinic Expands Access to Healthcare in Underserved Communities

One of the Association’s flagship initiatives is its Mobile Medical Clinic Project, a fully equipped medical unit that travels throughout remote villages and marginalized communities across Jerusalem and the West Bank. The clinic provides free medical examinations, laboratory testing, and medications to patients in need.

The project aims to address critical gaps in healthcare access in underserved areas by bringing essential medical services directly to residents who face significant challenges in reaching hospitals and healthcare centers, ensuring continuous access to primary healthcare services.

In addition, the Association organizes free medical outreach days targeting the most vulnerable populations. These events provide medical consultations, diagnostic examinations, and essential treatments at no cost, helping alleviate the financial burden on low-income families while improving their access to appropriate healthcare services.

The Association also operates field medical points within displacement-affected areas, delivering primary healthcare services and emergency medical interventions to displaced individuals and vulnerable communities. These field units play a vital role in rapid emergency response efforts, particularly in areas facing difficult humanitarian conditions, by providing immediate medical assistance that helps reduce suffering and improve health outcomes.

Investing in Healthcare Professionals and Capacity Building

The Association places significant emphasis on strengthening the skills and preparedness of healthcare professionals through internationally accredited training programs designed to enhance their ability to respond effectively to emergencies and critical medical situations.

Among its most prominent programs is the Advanced Trauma Life Support (ATLS) course, which equips physicians and healthcare workers with the knowledge and skills needed to manage severe injuries and trauma cases according to internationally recognized medical protocols.

The Association also delivers Advanced Cardiovascular Life Support (ACLS) training, one of the most important specialized programs in cardiac emergency management and resuscitation. The course provides participants with the expertise required to respond rapidly and effectively to life-threatening cardiac emergencies.

Complementing these initiatives is the Basic Life Support (BLS) program, which offers practical training in first aid, cardiopulmonary resuscitation (CPR), and emergency response to cardiac arrest, respiratory failure, and loss of consciousness, thereby enhancing the capacity of healthcare providers to manage a wide range of emergency situations.

Harnessing Artificial Intelligence to Advance Palestinian Healthcare

As part of its commitment to digital transformation and technological innovation, the Association has launched a specialized training program on Artificial Intelligence applications for members of the Palestinian Medical Association. The program introduces participants to emerging AI tools and technologies that can be utilized in administrative, organizational, and professional healthcare settings, contributing to improved efficiency, resource management, and service delivery.

In parallel, the Association implements a surgical assistance program dedicated to supporting patients who are unable to afford medical treatment. Through this initiative, essential surgical procedures are provided to low-income patients, helping save lives and improve the quality of life for individuals requiring specialized medical care.

Supporting Hospitals and Expanding Access to Life-Saving Surgical Care

The Association also focuses on strengthening non-governmental hospitals by providing critical medical equipment and devices that are unavailable in some healthcare facilities. Efforts include upgrading outdated equipment, replacing non-functional devices, and enhancing the overall capacity of healthcare institutions to deliver quality medical services.

Additionally, the Association contributes to funding free surgical procedures and post-operative medical follow-up programs for eligible patients, ensuring that vulnerable individuals receive the care they need regardless of their financial circumstances.

Its programs further extend to supporting ambulance and emergency medical services in areas affected by ongoing tensions and field developments. By strengthening emergency response teams and providing essential operational support, the Association helps ensure faster access to injured individuals and timely delivery of emergency medical care, ultimately reducing health risks associated with delayed treatment.

The trend of Canadians going into more debt is a significant concern, driven by rising living costs and financial obligations such as mortgages, student loans, and consumer debt. Recent statistics reveal that total household debt in Canada surpassed $3 billion in September 2024, with the average Canadian now carrying approximately $41,500 in household debt, excluding mortgages. This trend has been steadily rising for years,

This ratio reached 173.08% in 2021. Secured debt, such as mortgages or car loans, is a major contributor to household debt, while unsecured debt, including credit cards, relies on the borrower’s creditworthiness.

The cost of living is catching up to a large chunk of Canadians, with almost one in four taking on new debt in the last year. The Financial Consumer Agency of Canada found that more than half of Canadians are struggling to pay bills, and the OSB reported that 4.2 out of every 1,000 adult Canadians filed for insolvency in 2024, the highest rate since 2019. This accumulation of debt is attributed to spending consistently outstripping income for some time now.

Global News To manage debt, Canadians are advised to consider debt consolidation, a debt management plan, or a consumer proposal. These options can help reduce the amount paid if the interest rates and terms of a consolidation loan from a bank are better than those of the individual creditors.

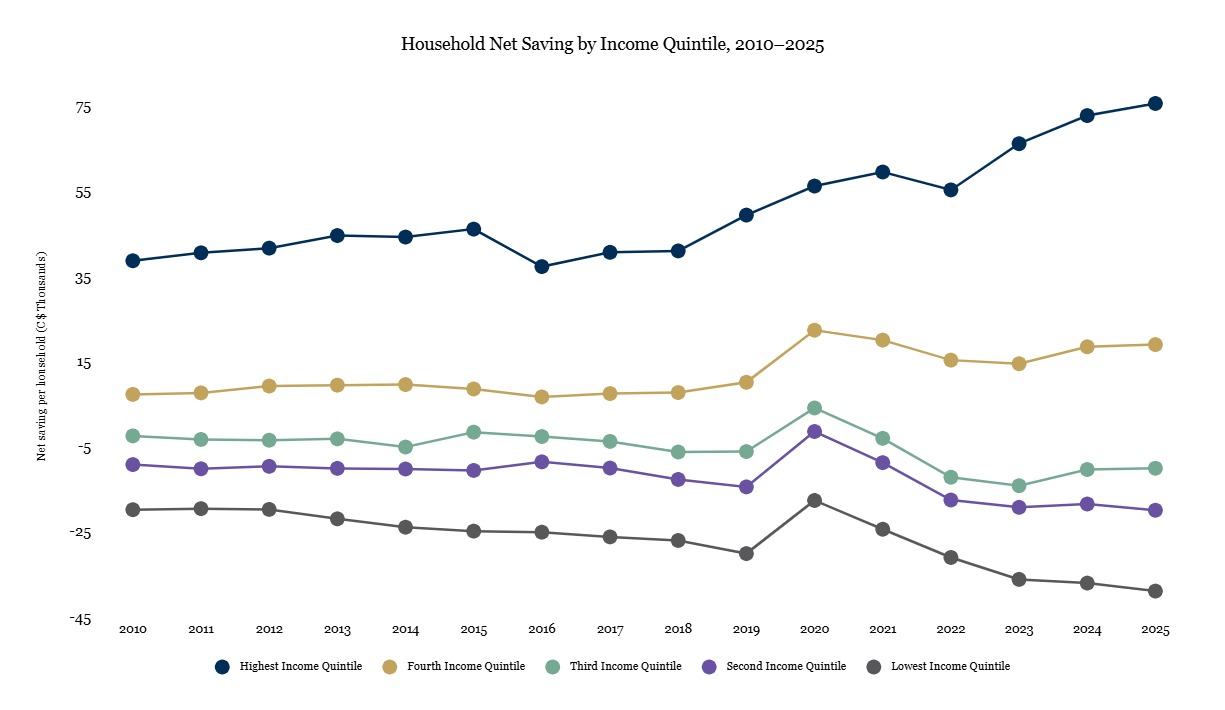

Canada’s household saving picture is splitting in two. Since 2021, the top fifth has lifted its average net saving to over $75,000 a year, while the lowest has sunk deeper into dissaving, spending nearly $39,000 more than its disposable income. The middle and second fifths have also slipped further into the red. Higher earners are pulling away as lower earners draw down savings and borrow to keep spending. For more on the health of Canada’s economy, see this C.D. Howe Institute memo.

Note: Negative values denote dissaving (consumption exceeds disposable income). Quintiles averaged the following income: Lowest quintile $33,000, second quintile $62,000, third quintile $88,000, fourth quintile $120,000, fifth quintile $219,000.

Source: Statistics Canada, Distributions of Household Economic Accounts (Table 36-10-0587-01). Figures are average net saving per household.

Connecting donors with the urgent humanitarian needs of displaced families living in tents across Gaza.

The city of Baltimore, Maryland, recently hosted the 51st annual convention of the Islamic Circle of North America (ICNA) in collaboration with the Muslim American Society (MAS), attracting nearly 25,000 attendees from around the world. This year’s convention expanded significantly, featuring a large exhibition hall that brought together hundreds of exhibitors, sponsors, community organizations, and charitable institutions.

Humanitarian and relief organizations, particularly those supporting displaced families living in Gaza’s tent camps, played a central role throughout the event. Beyond showcasing their projects, the convention serves as one of the largest annual platforms in North America for fundraising, partnership development, and direct engagement with Muslim communities.

A Platform Connecting Humanitarian Action with Community Engagement

Speaking about Life for Relief and Development’s participation in the convention, Vicki Roob, Director of International Programs, emphasized that the event is among the most significant annual Islamic gatherings in the United States and North America. It serves as a strategic platform that brings together humanitarian, charitable, and community-focused initiatives while providing valuable opportunities for direct engagement with diverse segments of American and Muslim communities.

Roob explained that the organization’s participation reflects its commitment to maintaining a strong presence at events that unite thousands of individuals passionate about humanitarian and charitable work. Each year, the convention attracts tens of thousands of attendees from across the United States and Canada, including community leaders, activists, volunteers, donors, charitable organizations, and humanitarian agencies. This environment offers a valuable opportunity to showcase Life’s mission, programs, and global humanitarian projects.

She added that visitors demonstrated significant interest in global humanitarian issues, particularly communities affected by conflict, disasters, and the ongoing displacement crisis in Gaza. This provided an important opportunity to highlight the growing needs of vulnerable populations and mobilize additional support for those most affected.

Life: A Trusted Bridge Between Donors and Those in Need

Omar Mamdouh, Director of Executive Projects, explained that the organization used the convention to spotlight a wide range of humanitarian programs and initiatives, including food security projects, assistance for vulnerable families, orphan sponsorship programs, and water, health, and education initiatives. Special attention was also given to Life’s emergency relief efforts in countries facing escalating humanitarian crises, particularly its support for displaced families living in Gaza’s tent camps and the delivery of humanitarian aid throughout the Gaza Strip.

Mamdouh noted that one of the convention’s most important benefits is the opportunity to connect directly with donors and demonstrate the impact of their contributions. The organization provided attendees with a comprehensive overview of living conditions inside Gaza’s displacement camps, including the severe shortages of essential supplies, the challenges faced by displaced children, the effects of extreme weather conditions, and the broader housing and shelter crisis affecting families throughout the region.

To help donors better understand these realities, Life displayed one of its newly developed shelter tents used in Gaza. Whereas previous tents measured 4 by 4 meters, the updated model measures 4 by 6 meters and includes a dedicated bathroom space to provide greater privacy, particularly for women. Visitors were also shown a model of daily life inside the tents, along with improvements and modifications made in response to feedback from displaced residents.

The exhibition further highlighted Life’s humanitarian projects around the world, its partnerships with universities to raise awareness about global humanitarian challenges, and samples of food assistance, including canned meat products distributed to beneficiaries.

Mamdouh emphasized that face-to-face engagement with donors provides an invaluable opportunity to share success stories and demonstrate tangible results made possible through their generosity, strengthening public confidence in sustainable and organized humanitarian work.

Engaging Youth and Channeling Their Efforts Toward Good

According to Khalil Meek, Director of Development, the convention also serves as an important platform for promoting a culture of giving and volunteerism. Life actively seeks to recruit new volunteers and involve them in its humanitarian mission while introducing young people and families to opportunities for community engagement and charitable service both within the United States and internationally.

He further noted that participation in the convention enables the organization to establish partnerships and collaborative relationships with other humanitarian and charitable organizations, facilitating the exchange of expertise and best practices that ultimately enhance the effectiveness and reach of humanitarian programs and joint initiatives.

Life’s Gaza Tents Featured in Al Jazeera Coverage

The organization’s activities during the convention received coverage from Al Jazeera, as Life’s exhibition booth attracted significant interest and engagement from participants. Many visitors took part in solidarity activities and wrote messages of support expressing compassion for communities affected by humanitarian crises.

Palestine maintained a strong presence throughout the convention. Participants were invited to write messages of solidarity on a tent that is scheduled to be sent to Gaza through Life for Relief and Development. This initiative builds upon the organization’s shelter support projects launched since the beginning of the war, including nine displacement camps established across northern, central, and southern Gaza.

These camps feature durable, standards-compliant tents that have provided shelter for approximately 46,000 displaced individuals. Designed for easy assembly and relocation to accommodate repeated displacement, the tents are also fire-resistant, helping protect civilian lives. Each tent is equipped with bedding and blankets, while every camp includes a medical clinic, sanitation facilities, solar energy systems, and insulation materials designed to protect residents from winter rains and extreme summer heat.

Life: Ranked Among the World’s Leading Humanitarian Organizations

Life for Relief and Development has been operating in more than 60 countries for over 33 years through a network of 16 international offices. The organization holds Special Consultative Status with the United Nations Economic and Social Council (ECOSOC).

According to Charity Navigator, Life ranks third globally among leading humanitarian organizations, fifth among organizations supporting displaced Palestinians, and fifth among organizations combating poverty worldwide. The organization also received a perfect 100% rating for 2026. In addition, it has been recognized by the United States Agency for International Development (USAID) and named by Impactful Ninja as one of the leading humanitarian organizations in the United States.

Life for Relief and Development was also awarded the Dubai Humanitarian Award for Best Partnership in recognition of its Gaza shelter camp initiative.

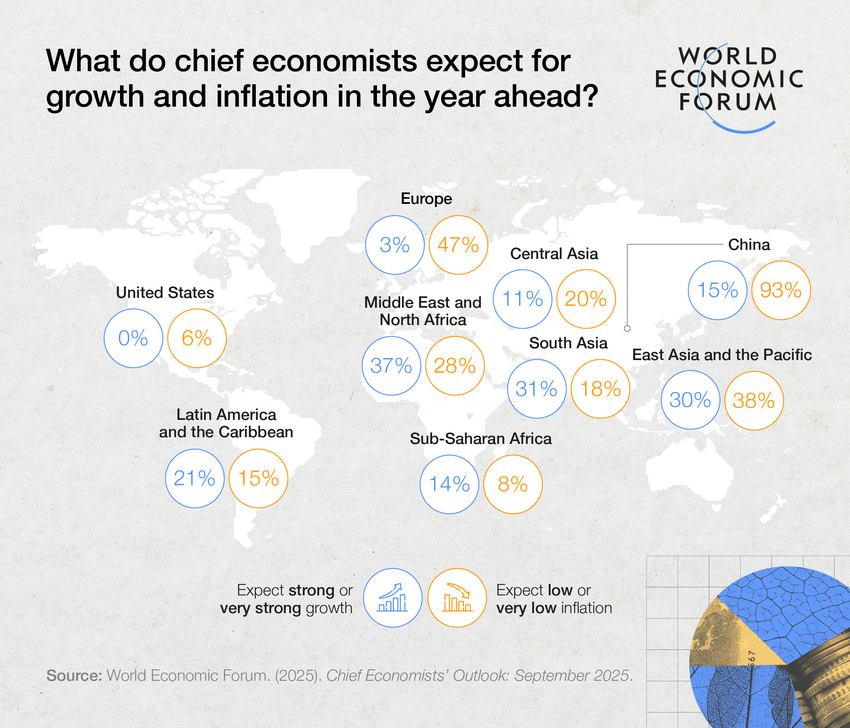

Fragmentation is already costing the global economy $213–$307 billion annually, while adding 0.2–0.3 percentage points to global inflation.

Fragmentation is spreading beyond geopolitical rivals to traditionally allied economies, including the EU, Canada, Japan and South Korea.

Emerging markets are likely to be hit the hardest by these shocks as countries outside the major geopolitical blocs face an estimated 10.7% hit to GDP growth versus 6.4% globally, even as regional initiatives offer new solutions.

New York, USA, June 2026 – Geoeconomic fragmentation imposing an annual cost of $213–$307 billion usd/ $296- $426 billion cad on the global economy, according to a new World Economic Forum report release today. Driven by geopolitical tensions, economic security concerns and shifting trade relationships across major economies, fragmentation accelerated through 2025 and 2026 and is increasingly affecting trade, finance and investment systems.

Deepening Divides: The Cost of a More Fragmented Financial System — published in collaboration with Oliver Wyman, a Marsh business, and the second in the Forum’s fragmentation series — finds that these pressures are playing out through escalating tariffs, investment restrictions and retaliatory measures.

The report finds that the growing use of economic statecraft in 2025 and 2026 marked a turning point for global trade and finance. While the first report focused primarily on fragmentation risks between geopolitical rivals, the latest findings suggest a broader structural shift is underway. Tariffs and investment restrictions are increasingly affecting traditionally aligned economies, including the US, the EU, Canada, Japan and South Korea, raising costs for businesses and increasing uncertainty for cross-border trade and investment.

“The global financial system has faced increasing pressures from geopolitical and economic fragmentation,” says Matthew Blake, Managing Director and Head of the Centre for Financial and Monetary Systems World Economic Forum. “Despite these pressures, the financial system has remained resilient. Markets have continued to provide real-time feedback on evolving policies while policy-makers have generally avoided actions that could erode confidence in the international financial system. As fragmentation persists, preserving the trust and stability that underpin global finance will be critical to supporting long-term growth and prosperity.”

The economic costs are rising As fragmentation becomes more embedded across markets and financial systems and barriers rise even among allies, the risks of escalation and long-term economic disruption increase. If current trends accelerate into more severe fragmentation scenarios, global losses could reach as much as $6.9 trillion usd, or 6.4% of global GDP, according to the report’s modelling, an economic impact larger than every economy in the world except the US and China.

Ultimately, fragmentation impacts both businesses and households. Current fragmentation policies are estimated to add 0.2–0.3 percentage points to global inflation, eroding purchasing power across most economies. The sharpest real wage impacts are seen in the United States, where real wages are estimated to be 0.33% lower for low-skilled workers, 0.49% lower for medium-skilled workers and 0.66% lower for high-skilled workers, with similar purchasing-power pressures visible in other major economies.

“In conversations with business leaders around the world, the message is remarkably consistent: What businesses need most right now is predictability, and they are not getting it,” says Daniel Tannebaum, Partner and Global Leader, Anti-Financial Crime Practice, Oliver Wyman, a Marsh business. “Without clearer guardrails around tariffs, sanctions and other economic measures, the risks to investment, growth and financial stability will continue to mount.”

Emerging markets face the sharpest exposure Emerging markets and developing economies (EMDEs) are likely to be the hardest hit by the impacts of growing financial fragmentation. In the most extreme fragmentation scenario, countries outside the major geopolitical blocs, most of which are EMDEs, could face output losses of 10.7%, compared to a global decline of 6.4%.

Structural factors like shallower capital markets make EMDEs more dependent on international capital flows and more vulnerable to the negative impacts of a less integrated financial system.

Africa exemplifies both the risks and potential resilience pathways. The continent’s exposure to external capital flows means a more fragmented system would make development financing more expensive and less predictable. At the same time, regional integration – through initiatives like the African Continental Free Trade Area (AfCFTA) and payment systems such as Pan-African Payment and Settlement System (PAPSS) – offers pathways to build resilience in Africa, which also stands to benefit from such secular trends as population growth and an abundance of critical raw materials.

While fragmentation is unlikely to reverse in the near term, it can be managed. The report identifies five actions policy-makers can take to mitigate fragmentation:

Policymakers can limit the damage

Establish shared guardrails to protect the financial system from fragmentation, emphasizing principles like safeguarding the rule of law and independent monetary policy, limiting the seizure of sovereign assets, and protecting the integrity of government data.

Align on rules to guide the use of economic statecraft policies that advance national security and resilience objectives without undermining global growth.

Ensure policy predictability to sustain investment flows and allow for the continued functioning of cross-border capital and financial markets.

Maintain interoperability across payment and digital currency systems and prepare businesses for a more fragmented geoeconomic operating environment.

Advance regional integration initiatives such as the AfCFTA and PAPSSP, as well as support the development of domestic and regional capital markets, including the European Savings and Investments Union.

Together, these measures can help preserve financial stability and resilience even as the global economy becomes more fragmented.

Report methodology

The report updates the Forum’s 2025 fragmentation analysis to reflect policy and market developments across 2025 and early 2026. Its quantitative modelling estimates the economic impact of current trade and financial policies and examines multiple escalation scenarios across output, inflation, trade flows and wages.

The analysis also incorporates updated assumptions on tariffs, countermeasures, pass-through rates and restrictions on services trade, alongside qualitative insights from business leaders, policy-makers and financial-sector experts, including regional perspectives from Africa.

About the Annual Meeting of the New Champions 2026

The 17th Annual Meeting of the New Champions will take place from 23 to 25 June 2026 in Dalian, People’s Republic of China, under the theme “Innovating at Scale”. The meeting will bring together 1,500 cross-sector leaders to explore how innovation and emerging technologies can unlock new growth models and drive positive economic momentum in a fast-shifting global landscape.

The United States is taking coordinated action to sever the Iranian regime’s access to the revenue streams that fuel its regional aggression and global terrorism.

The Department of State is sanctioning numerous entities, individuals, and vessels that form the backbone of Iran’s illicit oil economy, directly targeting the financial lifelines of the Islamic Revolutionary Guard Corps (IRGC) and Iran’s military apparatus.

As part of this action, State is designating eight entities and identifying eight vessels as blocked property for their transportation of Iranian petroleum, or petrochemical products, and also designating three entities and an individual in connection with trade in Iranian-origin petrochemical products.

Concurrently, the Department of the Treasury is sanctioning key players in an oil sales network that has moved tens of millions of barrels of Iranian oil worth billions of dollars. These Hong Kong-based entities have facilitated the storage, transport, and sale of this oil, directly funding the IRGC, Iran’s Armed Forces General Staff, and its military apparatus. This network represents a critical node in Iran’s ability to generate revenue for destabilizing activities across the Middle East.

The United States will not hesitate to take action against anyone, anywhere, funding the Iranian government’s ability to attack its neighbors and its own people. Any entity cooperating with Iran’s illicit oil trade or trading Iranian energy products faces the risk of exposure to U.S. sanctions.

Additionally, the Rewards for Justice (RFJ) program is offering a reward of up to $15 million usd/ $20.7 million cad for information leading to the disruption of the financial mechanisms of Iran’s IRGC and its various branches. More information is available on the RFJ website.

Today’s actions are being taken pursuant to Executive Order (E.O.) 13224, as amended, and Executive Order (E.O.) 13846. All Department of Treasury targets are being designated pursuant to E.O. 13224, as amended, which targets terrorist groups and their supporters. All Department of State targets are being sanctioned pursuant to Executive Order (E.O.) 13846, which authorizes and reimposes certain sanctions with respect to Iran. These actions continue the robust sanctions campaign targeting Iranian oil sales in support of Economic Fury and the President’s National Security Presidential Memorandum 2 (NSPM-2), instituting a campaign of maximum economic pressure on Iran.

For more information on this action, please see the Department of the Treasury’s press release Press Releaseand the Department of State’s Fact Sheet.

Life for Relief and Development calls for increased global support as rising living costs and food insecurity intensify humanitarian needs worldwide

World’s Most Vulnerable Is An Increasing Demographic

As the costs of food, fuel, housing, healthcare, and necessities continue to climb across the globe. Humanitarian organizations are warning that the world’s most vulnerable populations are facing increasingly devastating consequences. In 2024, more than 295 million people across 53 countries experienced acute hunger, marking the sixth consecutive year global food insecurity has worsened. That number has since risen to 343 million. Families already living in poverty are now being pushed further into crisis, forced to make impossible decisions between food, medicine, education, and shelter.

Surging Inflation

According to international economic and humanitarian reports, surging inflation, supply chain disruptions, ongoing conflicts, climate-related disasters, and economic instability have significantly increased the cost of living worldwide. While these rising pressures are affecting households everywhere, the burden falls disproportionately on low-income communities and developing nations, where millions are already struggling to meet basic daily needs.

Life for Relief and Development (LIFE), a global humanitarian organization dedicated to providing aid regardless of race, gender, religion, or cultural background, is witnessing firsthand the growing impact economic pressures have on crisis-affected communities across the Middle East, Africa, Asia, Eastern Europe, and beyond.

Limited Resources

“In many of the communities we serve, families were already surviving on very limited resources,” said Dr. Hany Saqr, CEO of LIFE. “Now, with food prices soaring and essential goods becoming increasingly unaffordable, many parents are struggling simply to feed their children. What may feel like inflation in one part of the world can become a matter of survival in another.”

LIFE’s humanitarian teams continue to respond through emergency food assistance, orphan support programs, healthcare initiatives, clean water projects, seasonal aid distributions, and long-term development efforts aimed at helping families regain stability and self-sufficiency. Working in more than 60 countries, LIFE has helped deliver $667 million usd/ $922.4 million cad in humanitarian assistance over the past three decades, supporting vulnerable communities affected by conflict, hunger, displacement, poverty, and disaster.

“Humanitarian aid is no longer just about responding to emergencies after they happen,” Dr. Saqr added. “For millions of families, assistance is what prevents a difficult situation from becoming a catastrophe.”

In addition to its ongoing humanitarian initiatives, LIFE will perform Udhiyah/Qurbani distributions this year in 32 countries. Through the annual program, fresh meat will be distributed to families experiencing difficulty during Eid al-Adha. Last year, the initiative helped combat food insecurity for nearly 200,000 people worldwide, including families in Gaza who received canned meat distributions due to ongoing access restrictions. LIFE says the program not only helps provide nutritious meals but also allows vulnerable families to participate in Eid with dignity.

Growing Challenges

As the world continues to face growing economic and humanitarian challenges, compassion, shared responsibility, and collective action can play a significant role in shaping a more just and hopeful future. Life for Relief and Development believes that meaningful change begins when people choose not to turn away from suffering but instead work together to help create a more humane, equitable, and sustainable world while opening pathways toward greater stability and opportunity for future generations.

Since its creation in 1987, the Office of the Superintendent of Financial Institutions (OSFI) has served as Canada’s federal micro-prudential regulator, operating under a single-head governance model that was suitable at the time but has not undergone a major review in nearly three decades.

Particularly following the 2008 financial crisis, OSFI’s activities have expanded in response to a more complex and rapidly evolving environment in which Canadian financial institutions operate. Meanwhile, governance practices across the financial sector have modernized, leaving OSFI’s structure increasingly out of step with its domestic and international peers.

To modernize OSFI’s governance, policymakers should mandate regular parliamentary oversight and introduce a multi-member model, such as a board of directors supported by advisory committees. These changes would strengthen transparency, accountability, and diversity of perspectives, ensuring that OSFI remains a credible and responsive regulator.

OSFI would also benefit from a periodic review of its governance framework. A formal review cycle, at least once every decade, would help keep its governance model current, effective, and aligned with its expanding responsibilities.

Introduction

Canada’s financial system faces a brave new world of risks, from geopolitical fragmentation and cyber threats to climate-related shocks, that place new demands on its regulators. But the governance structure of the Office of the Superintendent of Financial Institutions (OSFI), the country’s federal prudential regulator, has remained largely unchanged for decades.

OSFI was established in 1987 to ensure the safety and soundness of the Canadian financial system, based on recommendations from the Estey Commission. It was formed by consolidating the Department of Insurance and the Office of the Inspector General of Banks.

A Superintendent, supported by deputies and staff, holds sole responsibility for prudential regulation and supervision. While OSFI is an independent agency, it is accountable to Parliament through the minister of finance. Its internal governance includes a Departmental Audit Committee (DAC), which advises on risk management, control, and governance frameworks, and an internal audit team that reports to the Superintendent.

This structure differs meaningfully from those of comparable domestic and international regulators. And there are reasons to ask whether its governance structure remains appropriate for today’s environment.

We start with the premise that, since 1987, governance practices, financial services, the risk environment, and OSFI’s mandate and activities have all evolved significantly. Yet the model underpinning OSFI’s structure (see Box 1) has not undergone a major review since the MacKay Task Force in 1998, nearly 30 years ago.

Historically, Canada’s financial system included five main groups: chartered banks, trust and loan companies, the co-operative credit movement, life insurance companies, and securities dealers. These pillars began to dissolve shortly after the formation of OSFI with the 1987 and 1992 revisions to the Bank Act, as large banks acquired trust and loan companies and securities dealers. Recently, some credit unions have become federally regulated.

Today, Canada’s financial sector faces a convergence of risks that challenge traditional prudential supervision and place new demands on regulatory governance. Beyond post-financial crisis concerns about capital adequacy and credit risk, the current landscape includes geopolitical tensions that could disrupt cross-border resolution and capital flows (Zelmer 2025), increasingly sophisticated cyber threats (including state-linked attacks [OSFI 2025]), and escalating physical and transition risks from climate change (IMF 2025a). While OSFI has strengthened its supervisory frameworks in areas such as cyber resilience and climate risk, these pressures highlight the importance of a governance structure capable of navigating complex trade-offs between stability, competitiveness, resilience, and public confidence.

OSFI’s responsibilities have also expanded. Since 2012, it has overseen the insurance activities of the Canada Mortgage and Housing Corporation (CMHC). In 2016, it introduced a mortgage stress test, increasing its direct impact on individual Canadians. More recently, the passage of Bill C-47 in 2023 requires OSFI to examine whether federally regulated financial institutions have adequate policies and procedures related to integrity and security.

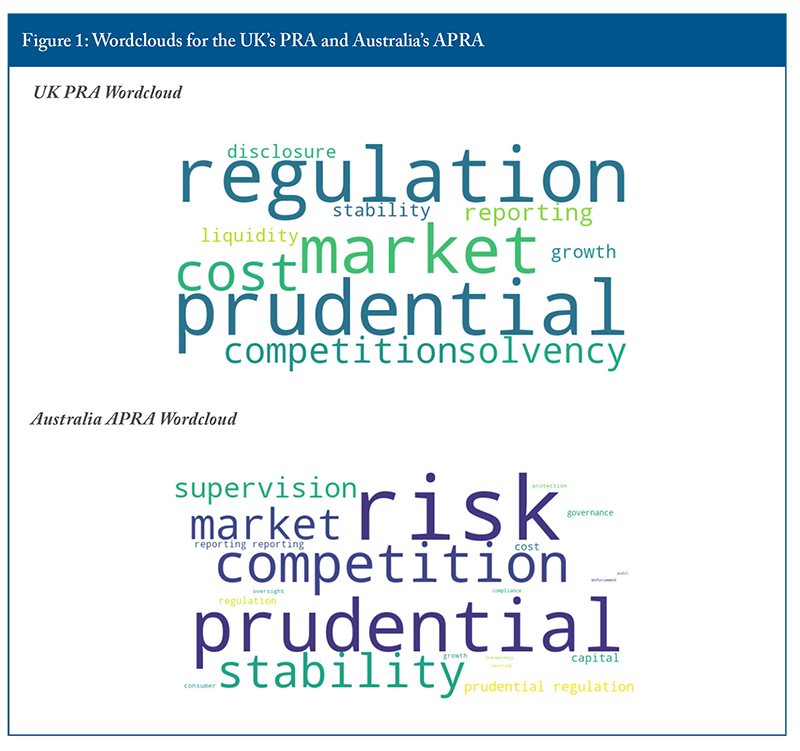

Compared with its peers, OSFI’s governance model is unusual. Many comparable regulators operate with boards (OECD 2010). The OECD (2014) identifies several advantages of multi-member governing bodies: they are less susceptible to regulatory capture than a single decision-maker; they better balance judgment in complex, principles-based regulatory environments; and they provide collective support for strategic oversight. All three apply to OSFI. While its track record reflects strong leadership, distributing authority would reduce institutional vulnerability by design, rather than relying on any one individual. A multi-member body would also provide a structured forum for debating complex trade-offs and challenging internal decision-making as OSFI confronts emerging risks such as AI and cyber threats.

International counterparts following such practices include the UK’s Prudential Regulation Authority and Australia’s Prudential Regulation Authority. Domestically, newer regulators such as the Financial Services Regulatory Authority of Ontario (FSRA), along with securities regulators like the Ontario Securities Commission (OSC), have adopted board governance structures.

Given the evolving financial landscape, a shift from a single-head model to a multi-member structure is warranted. Regulating the financial system requires a balancing act that collective decision-making provides by offering a diversity of opinions, expertise, and perceptions. As OSFI’s activities expand into areas such as cybersecurity and financial institution governance, it also requires new subject-matter expertise to develop compliance and enforcement capabilities in new areas.

We therefore recommend that OSFI transition to a multi-member governance structure, including a board of directors and advisory councils. This would strengthen independence, enhance transparency and accountability, and align OSFI with best practices in regulatory governance.

OSFI’s governance model should also undergo periodic review – something that has not occurred since the MacKay Task Force nearly three decades ago (see Box 2). This absence has left the framework misaligned with international best practices. Conducting a formal review at least once every 10 years would ensure that the model remains current and fit for purpose in fulfilling OSFI’s mandate and Canadians’ expectations.

OSFI Expanded Responsibilities and Activities

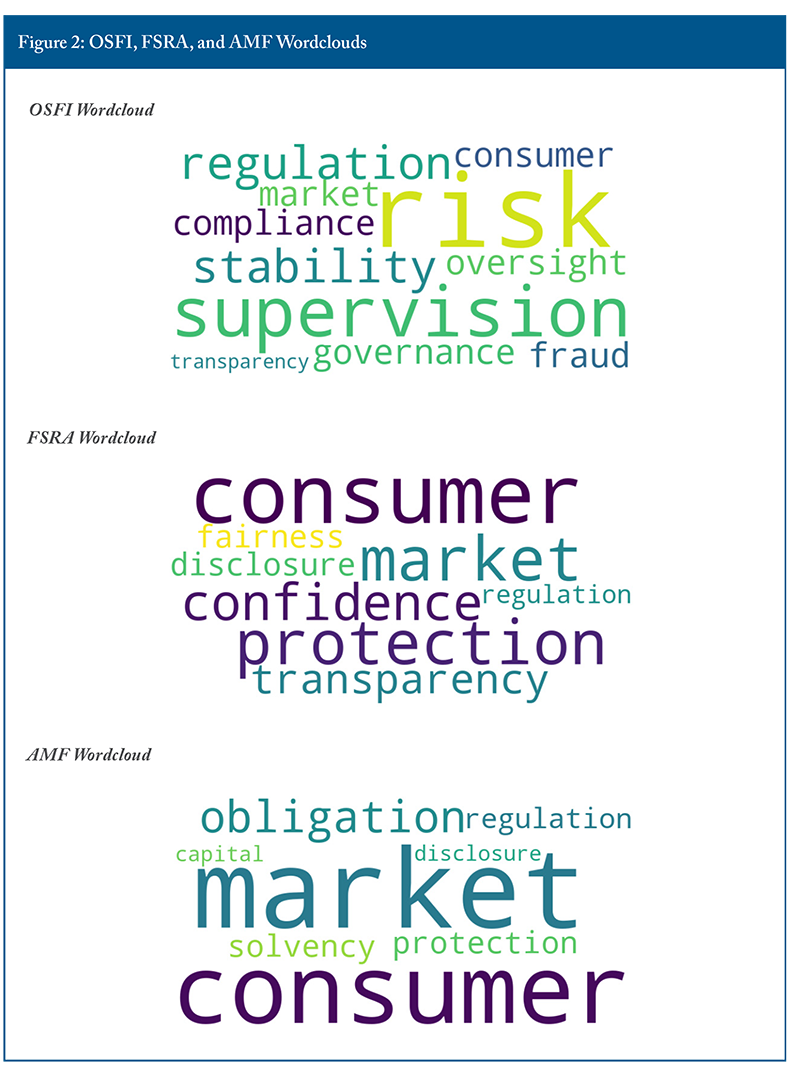

Since the 2007-08 global financial crisis, OSFI’s mandate and responsibilities (Figure 2) have broadened significantly in response to rising systemic risks and a more complex financial landscape. As noted, OSFI oversees CMHC, particularly its commercial activities in the mortgage insurance sector – an area critical to housing market dynamics and, by extension, to household debt and consumption patterns.

OSFI has also taken a more proactive role in setting regulatory expectations. Since 2016, it has accelerated the issuance of guidelines on governance, capital adequacy, and insurance practices of federally regulated financial institutions (FRFIs). In some cases, these guidelines go beyond traditional supervisory functions and increasingly influence Canadians’ everyday financial experiences.

One prominent example is the Minimum Qualifying Rate (MQR) or “mortgage stress test” introduced by OSFI in 2018. It requires lenders to verify income and apply a minimum qualifying rate to uninsured mortgages. The stress test is designed to evaluate the solvency of mortgage holders under adverse interest rate conditions, reduce systemic risk in the housing market, and support sound financial management of financial institutions. While it strengthens system resilience, this approach may limit household credit availability and affect Canadians’ capacity to purchase homes.1

More recently, the passage of Bill C-47 by the federal government in 2023 further expanded OSFI’s authority. It allows OSFI to assess whether FRFIs have adequate integrity and security policies and procedures. This change reflects the shift toward a broader conception of financial stability. As a result, the Superintendent’s responsibilities have grown in both complexity and impact.

Although OSFI has developed the in-house expertise2 to manage its expanded functions, its evolving role would benefit from greater external input.3 Incorporating diverse perspectives would strengthen its ability to challenge prevailing internal perspectives and ensure that its regulatory approach remains well-informed, while anchored in its prudential mandate.

The Pros and Cons

Before making the case for transitioning OSFI to a multi-member model, it’s useful to set out the advantages and limits of each governance model. Regulators generally use three models. The first is a multi-member body that sets strategic direction and operational policy, while delegating regulatory decisions to a chief executive officer. The second is a commission model, also multi-member, in which a collective makes most substantive decisions. The third is a single-head model, where one individual holds primary decision-making authority.

The Organisation for Economic Co-operation and Development (OECD 2014) provides the established international framework for evaluating regulatory governance, including the choice between single-member and multi-member governance structures for independent regulators. It identifies when a multi-member governance model adds value, outlines the design considerations, and offers a framework for applying these factors to a specific regulator. Table 1 summarizes the main advantages and disadvantages of a multi-member body.

When a multi-member body adds value

The OECD (2014) identifies five factors in determining whether a multi-member governing body adds value.

Potential consequences of regulatory decisions: A collective is less susceptible to regulatory capture4 than an individual and benefits from a wider range of perspectives.

Need for diverse judgment: In complex or principles-based regulation, collective decision-making better balances judgment factors and minimizes the risks of varying judgments.

Degree of strategic guidance and oversight required: This is especially important when developing new regulations and deploying resources because a multi-member model provides the necessary collective support for strategic considerations.

Maintaining regulatory consistency over time: A group can better maintain consistency by providing “corporate memory” in decisions that rely heavily on judgment.

Decision-making independence: Boards are generally less susceptible to political or industry influence than a single decision-maker.5

What the single-head model offers that a multi-member model risks losing

By identifying when multi-member governance adds value, the OECD framework implicitly identifies the conditions under which a single-head model is better suited.

One of the clearest advantages of the single-head model is that responsibility is unambiguous. At OSFI, the Superintendent is directly accountable to the minister of finance, Parliament, and the public. Having a board does not automatically improve accountability. It can, if poorly designed, diffuse it.

The single-head model also enables faster, more decisive action. It avoids the delays of consensus-building and supports rapid responses to emerging risks or mandate changes. It can also minimize the risk of policy conflict that may arise when multiple board members hold divergent views.

These are not trivial considerations. As a microprudential regulator, OSFI must often respond rapidly to emerging risks and take swift decisions on a case-by-case basis. The ability to act without delay is valuable. A poorly designed multi-member body could slow responsiveness and introduce the kind of internal disagreement that undermines regulatory certainty. The OECD (2014) acknowledges this risk, noting that where a regulator has a high volume of time-sensitive decisions, the full governing body may need to delegate extensively.

The tension between models is genuine.

The OECD framework does not prescribe a single model but asks whether, on an honest assessment of the five criteria, the case for collective governance has been met. As the following sections argue, OSFI’s expanded mandate, the more complex risk environment, and the breadth of judgement now required shift that balance toward a multi-member model, provided the design risks are carefully managed.

The Evolving Risk Environment: A Case for Enhanced Governance

As this section demonstrates, Canada’s financial sector faces an unprecedented convergence of risks – geopolitical instability, cyber threats, climate change, and complex capital regulation trade-offs – that has expanded well beyond post-financial crisis concerns and fundamentally challenges traditional regulatory approaches. This shift raises the question of whether OSFI needs a new governance approach.

The answer is yes. As these risks grow in scope and complexity, OSFI’s governance structure should evolve accordingly. While the current model concentrates decision-making authority in a single Superintendent, a board could bring together experts in geopolitics, cybersecurity, climate science, international finance, and domestic economic policy to inform OSFI’s strategic direction. It would provide a forum for debating complex trade-offs, such as balancing financial stability with economic growth or weighing international regulatory coordination against domestic competitive concerns, in a more transparent and accountable manner. Most importantly, it would enhance OSFI’s legitimacy and public confidence in its decision-making during periods of intense scrutiny.

Geopolitical Risk and Cross-Border Vulnerabilities

Rising geopolitical tensions present fundamental challenges to Canada’s internationally active financial institutions. As Zelmer (2025) notes, weakening cross-border cooperation, particularly involving the United States, could make it harder to manage the recovery or orderly resolution of internationally active Canadian financial institutions during periods of distress. Foreign regulators may ring-fence assets within their jurisdictions, limiting Canadian authorities’ access to the capital and liquidity needed to protect domestic depositors and creditors. This risk is especially significant because Canada’s six major banks have substantial operations and exposures in the United States and other foreign markets.

These emerging and potentially politicized risks highlight the value of a board in providing independent, collective support for OSFI’s strategic direction.

Cyber Risk and Technological Threats

Cyber threats targeting financial institutions have increased in frequency and sophistication. In 2023, 26 percent of finance and insurance firms experienced cybersecurity incidents, compared with 16 percent across the private sector.6 Furthermore, the threat of cyberattacks remains high in Canada (IMF 2025b), and money laundering and fraud attempts from criminals and state-linked actors are becoming more advanced and difficult to detect (OSFI 2025). These activities will likely intensify with advances in AI and digitalization.

OSFI has acknowledged that foreign actors may target Canadian institutions for financial gains and geopolitical purposes (OSFI 2025). Repeated incidents in the financial sector could erode confidence and threaten its stability, causing spillovers to the rest of the economy.7

A 2025 IMF Financial Sector Assessment Program review of Canada found that while OSFI’s cyber risk supervisory framework is strong, gaps remained in coordination with federal and provincial authorities, and that OSFI’s integrated mandate enables it to detect advanced cyber threats beyond conventional risks (IMF 2025b). Given the complexity of these risks, a well-designed board with the right expertise could offer appropriate support in developing a strategic plan to mitigate these risks.

Climate Risks

Climate change presents both transition and physical risks to Canada’s financial system, with broader macroeconomic effects. It can reduce GDP (Dahlhaus 2025), increase inflation volatility (Duprey and Fernandes 2025), and negatively affect employment (Duprey et al. 2024). The 2016 Fort McMurray wildfire alone caused an estimated $9.9 billion in damages and reduced quarterly GDP by 0.4 percent (Statistics Canada 2024). These risks are expected to intensify, with projections indicating more frequent and severe weather conditions and longer wildfire seasons across much of Canada (IMF 2025a).

OSFI’s Guideline B-15 sets out expectations for FRFIs’ management of climate-related risks.8 However, the IMF’s recent assessment of climate risk in Canada’s financial sector recommends that OSFI strengthen its climate risk supervision through better data, coordination, and stress testing (IMF 2025a). A board with relevant expertise could help guide OSFI’s strategic response, while an advisory committee could support technical policy development in this area.

Domestic Regulatory Complexity: Basel III and Capital Requirements

Implementing Basel III reforms has created significant domestic challenges. In 2024-2025, OSFI faced intense public scrutiny over its approach to implementing the Basel III standardized capital floor (Zelmer 2024), with Superintendent Peter Routledge noting that the intensity of attention was new to OSFI and provided an opportunity to communicate more clearly to Canadians (OSFI 2024). The Superintendent noted that some observers argued that OSFI’s decision would have “a consequential and negative impact on economic growth, arguing that dramatically rising capital requirements would slow lending and then economic growth” (OSFI 2024).

OSFI’s decision to indefinitely defer increases to the Basel III standardized capital floor level reflected concerns about competitive balance in the international banking system, as uncertainty remained about when other jurisdictions would fully implement Basel III.9 These are precisely the kinds of complex, multi-dimensional trade-offs that a board, equipped with expertise in international finance, economics, and competition policy, could be designed to support and challenge. A structured deliberative process within a governing board could provide a forum to assess these issues transparently and reduce perceptions of reactive or politically influenced decision-making.

The General Case for Multi-Member Governance at OSFI

The previous sections have shown that, across multiple dimensions of OSFI’s expanded mandate and activities, a multi-member governance structure could create net benefits over the current single-head model. This section shows how OSFI’s governance structure is out of step with comparable regulators domestically and internationally and draws lessons for reform.

International Comparison of the Governance Structures of Financial Institutions’ Regulatory Supervisors

We compare OSFI’s governance structure with the Australian Prudential Regulatory Authority (APRA), the UK’s Prudential Regulatory Authority (PRA), and Switzerland’s Financial Market Supervisory Authority (FINMA). All have similar mandates: they regulate financial institutions but are not responsible for promoting consumer protection.10

APRA uses a commission model that supports collective decision-making and incorporates a range of perspectives, thereby reducing dependence on any single leader. Its executive board of three to five government-appointed members, including the CEO as chair, manages operations and sets strategy. However, the responsibility for balancing immediate operational demands with long-term strategic priorities ultimately remains concentrated in a single authority. A clearer separation of these roles might yield a more effective balance. Consequently, this governance approach remains vulnerable to some of the same challenges faced by the single-head model. Furthermore, a lack of external views may hinder strategic decisions, given that the members are all employees and thus not independent of APRA.

Switzerland’s FINMA represents a cleaner governance board model and is widely seen as best practice (OECD 2014). An independent board of seven to nine expert members from academia and industry sets the strategic oversight and long-term planning, and oversees an executive team led by a CEO. No FINMA employees or ministry of finance officials sit on the board, ensuring independence. Its architecture creates a clear distinction between strategic and operational management. The board enhances the executive team’s accountability, and its composition strikes the right balance of multidisciplinary expertise between market practitioners and academics. Bringing expertise from law, finance, economics, and insurance helps align long-term strategy with evolving risks. However, safeguards are needed to prevent decision-making delays and mitigate potential biases.11

The PRA in the UK functions uniquely as part of the country’s central bank, and the Bank of England (BoE) employs the PRA staff. As a microprudential regulator, the PRA focuses on ensuring individual financial institutions are well capitalized and avoid excessive risk-taking, but through the lens of the effects those firms can have on system stability.12

Its structure is similar to the APRA’s in that it’s also governed by a commission, the Prudential Regulation Committee (PRC). At least six external expert members appointed by the government sit on the PRC, which makes it more independent.13 External members bring both market experience and academic insight, balancing practical relevance with historical and policy context. However, the presence of the BoE Governor on the board of both institutions, though a deliberate institutional choice given the PRA’s mandate orientation toward the systemic effects of firm-level risk, may raise questions about accountability and the separation of firm-level and system-level considerations in a crisis.

While OSFI’s single-head governance model offers advantages, experience across comparable jurisdictions reinforces the view that a multi-member governance structure is the most adequate for financial sector regulators. Diverse expertise and collective judgment improve decision-making and help regulators meet increasingly complex mandates. Given OSFI’s similar responsibilities, industry context, and evolving risk environment, these international experiences offer practical lessons for transitioning to a multi-member structure.

The Evolution of Provincial Financial Regulators

Recent Canadian reforms also support this shift. In 2022, the Ontario government revised the governance structure of the OSC (see Figure 3)14 to embrace evolving governance best practices as recommended by the Ontario Capital Markets Modernization Taskforce. The Taskforce determined that the OSC’s previous single-headed leadership structure hindered strategic oversight and operational execution, thereby limiting the organization’s overall effectiveness. It separated the Chair and CEO roles and established a board of directors (Capital Markets Modernization Taskforce 2021). Under this new model, the CEO oversees day-to-day regulatory operations, while the board sets strategic direction and governance.

Prior to that, Ontario adopted modern governance standards when it created FSRA in 2019, replacing FSCO and DICO with an agency led by an independent board and a separate CEO responsible for day-to-day management (FSRA 2025). The board sets strategic direction, oversees governance, and monitors the regulator’s performance against its mandate. The Chair of the Board serves as the primary liaison with the responsible ministry. The board has 12 members (up to 11 independent permitted plus the CEO), all with financial sector experience.15

The Canada Deposit Insurance Corporation as Institutional Comparator

The case for external board governance at OSFI is not limited to international and provincial precedents. The Canada Deposit Insurance Corporation (CDIC), which is part of Canada’s federal financial safety net, has a similar institutional structure.

CDIC operates with a board of directors, handles institution-specific supervisory data of comparable sensitivity to OSFI’s, and carries a mandate – deposit insurance, financial system stability, and resolution authority – that is functionally interdependent with OSFI’s prudential supervision role.

CDIC’s board comprises 12 members: six ex officio public sector directors drawn from the Department of Finance, the Bank of Canada, OSFI, and FCAC; and six private sector directors appointed by the Governor in Council for terms of up to four years. The CDIC Act16 bars current federal public servants, members of Parliament, and anyone affiliated with a federal or provincial financial institution from sitting on the board as private sector director. This exclusion addresses conflicts of interest while preserving access to relevant expertise. This demonstrates that statutory design can resolve the tension between independence and sectoral knowledge without foreclosing either.

The board’s mandate extends beyond administrative oversight to include strategic direction and decision-making authority over interventions in member institutions. These decisions are sensitive and time-critical, and often cited as incompatible with OSFI’s operating environment. CDIC’s experience suggests otherwise: a board can exercise strategic authority without displacing management.

Confidentiality concerns are also manageable. CDIC’s board routinely handles granular information on member institutions, subject to the conflict-of-interest rules and confidentiality obligations set out in the CDIC Act and the FAA. The practical management of confidential supervisory information within a board governance structure can be an established operating condition. There is no clear reason why similar arrangements could not function at OSFI, which is subject to comparable statutory confidentiality provisions and operates within the same inter-agency information-sharing framework.

The Office of the Auditor General of Canada has validated this model,17 finding CDIC’s governance sound and its board effective. This is further evidence that board governance of a federal financial body operating in a confidential supervisory environment is institutionally sustainable and withstands rigorous independent scrutiny over time.

In addition, the OSFI Superintendent already sits on CDIC’s board as an ex officio member, participating in board governance. The Superintendent is therefore already a participant in board-level governance of a federal financial institution operating under the same confidentiality constraints.

Taken together, the CDIC model helps in making the case for an OSFI board and shows that confidentiality constraints don’t render external governance impractical and need not compromise operational independence. The relevant question for reform is not feasibility, but how to define the boundary between board oversight and the Superintendent’s authority to preserve supervisory independence. We turn to that question next.

OSFI’s Next Review

The preceding sections have shown that board governance can coexist with operational independence across a range of international and domestic institutional comparators. The next question relates to design – how to structure such a board and allocate authority among the board, the Superintendent, and the minister.

OSFI’s mandate and governance structure have not been reviewed since 1998. This lack of periodic reviews is itself a structural gap. Comparable financial regulators in Canada and abroad undergo regular assessments of their mandate, governance, and accountability. OSFI has not. A review is warranted not because of weak performance, but because its governance framework has not been evaluated against current institutional standards, peers, or international norms in nearly 30 years.

A review focused on board governance should address, at minimum:

What public policy outcomes should OSFI deliver?

What operational, legislative, or regulatory changes would improve its effectiveness in the face of changing market realities?

Would a new governance model strengthen or weaken political oversight needed to keep legislation and enforcement up to date?

How would alternative governance structures affect the risk of stakeholder regulatory capture?

How can governance design account for Canada’s unique federal/provincial division of financial sector regulatory responsibilities and ensure desired regulatory outcomes can be effectively achieved?

How should statute define the boundary between board strategic oversight and the Superintendent’s authority?

What appointment criteria and processes would ensure board independence without limiting access to relevant financial sector expertise?

How should the board be accountable to Parliament, and how would this differ from the Superintendent’s reporting obligations?

What, if any, role should the board play in the use of macroprudential tools such as the Domestic Stability Buffer?

How should the accountability relationship between the Superintendent and the minister of finance be preserved or clarified in the context of a multi-member governance structure?

The next section addresses some of these questions and sets out a proposed governance architecture that draws on the institutional comparators examined and the design lessons from the MacKay Taskforce.

A Roadmap to Improve OSFI’s Governance

We now turn to how OSFI can improve its governance structure by incorporating diverse perspectives and enhancing its credibility with stakeholders. Effective governance frameworks for government agencies must safeguard against undue political or industry influence.

While OSFI maintains a professional relationship with regulated institutions, there is no evidence of regulatory capture within the Canadian financial system (IMF 2014). Nonetheless, a board structure could further strengthen OSFI’s independence by reducing vulnerability to such influence. Collective governance bodies are less susceptible to capture than individual decision-makers and can enhance institutional credibility (OECD 2014; Jabotinsky and Siems 2017). This is not to suggest that any Superintendent has been susceptible to such influence. Rather, distributed authority and diverse membership provide a durable safeguard that does not depend on any one individual.

Given OSFI’s expanding mandate and activities, the board could provide strategic oversight and support, while reinforcing institutional memory and consistency. It would allow the Superintendent to focus more on day-to-day operations while contributing to long-term strategy.

To achieve this, we recommend two changes: an independent board of directors to provide strategic oversight and expertise; and advisory councils to supplement OSFI’s knowledge in emerging risk domains such as cybersecurity and artificial intelligence.

1. Board of Directors

The board would:

Approve strategic direction, policies, culture, and risk appetite, and provide independent advice to the Superintendent.

Be accountable to Parliament and subject to its oversight and scrutiny.

Periodically review OSFI’s policy effectiveness (e.g., the MQR stress test or the Domestic Stability Buffer).

Approve the budget, review OSFI’s Annual Risk Outlook, and provide a challenge function.

Execute decisions on prudential tools such as the MQR or the Domestic Stability Buffer.

Structure of the Board

To provide OSFI with diversity of expertise and perspective, the board of directors should:

Exclude members from FISC and regulated industries to maintain independence.19

Draw members from academia, former regulators (including those from other jurisdictions), risk specialists, and former industry practitioners.20

Include an independent chair and five to nine members with multidisciplinary expertise. The Superintendent should serve as a member, and a government representative (e.g., deputy minister of finance) could serve ex officio.21

Use three-year renewable terms with staggered appointments to ensure continuity.22

This structure differs fundamentally from the existing DAC. The DAC is an advisory body within OSFI that provides independent advice and recommendations to the Superintendent on risk management, internal controls, and governance frameworks. The DAC is composed of a majority of external members drawn from outside the federal public administration, with relevant experience in private and public sector financial reporting. Members are selected by the Superintendent and approved by the Treasury Board. At least one member must hold a professional accounting designation. The Superintendent sits as an ex officio member.

The proposed board of directors differs from the DAC in many respects (Table 2). Where the DAC looks backward to verify that established processes were followed, the board looks forward to challenge whether OSFI is pursuing the right strategic priorities. Where the DAC reports to the Superintendent, the board exercises independent oversight over the Superintendent. And where the DAC has no parliamentary accountability function, the board would serve as a formal mechanism linking OSFI’s governance to parliamentary scrutiny, which is a function that currently does not exist.

The distinction is substantive, not incremental: the DAC strengthens process integrity, while the board would strengthen the legitimacy of OSFI’s direction. Both are necessary, but one cannot substitute for the other.

2. Advisory Committees

Financial regulators commonly use advisory committees to access industry expertise and incorporate market perspectives into policymaking. For example, the OSC is supported by seven distinct third-party advisory committees to provide input on new policies, assess regulatory impacts, and communicate stakeholder concerns.23 These committees focus on specific technical or sectoral topics and provide advice to staff, drawing on both market participants and regulators.

Internationally, the UK’s PRA uses the Practitioner Panel to represent the interests of industry practitioners to fulfill a statutory duty. This independent panel provides expert input on the PRA’s policies and constructive challenge and advice to ensure that practitioner perspectives are reflected in regulatory decision-making. It meets about six times a year with PRA leadership and has contributed feedback on a range of policy issues, including the implementation of Basel 3.1.

While it is true that financial services regulators already incorporate the views of market participants and stakeholders into their regulatory rules through public consultations, they control these processes by setting the agenda and framing the questions. This approach is episodic and tied to specific rule-making initiatives.

Advisory committees would:

Provide OSFI with a diversity of expertise and perspectives on risk-related issues, particularly in emerging areas where in-house capacity may be limited (e.g., cybersecurity).24

Challenge OSFI’s policy responses on issues such as technology, security, and integrity risks.

Transparency around such bodies would contribute to the credibility of OSFI’s policy responses. Publishing the membership of each group and any recommendations that the body may provide to OSFI would further enhance credibility.

Advisory committees would not:

Engage in federally regulated financial institution work, preserving confidentiality.25

Manage OSFI’s operations, including staffing, budgeting, and internal structure.

Review OSFI decisions and actions for specific institutions.

Participate in OSFI-specific decisions regarding systemic prudential tools such as the MQR or the Domestic Stability Buffer.

Structure of the Advisory Committees

Advisory committees should:

Be independent.

Include members from academia, regulatory bodies (including other jurisdictions), risk specialists, and selected industry practitioners.26

Have an independent chair and at least five expert members with multidisciplinary backgrounds.

Be reviewed periodically to ensure expertise remains aligned with emerging risks, informed by sources such as OSFI’s Annual Risk Outlook and the IMF’s Global Financial Stability Report.

Be time-limited where appropriate (e.g., three-year terms or until a specific policy issue is addressed), reflecting their specific topic of focus.27

While an independent board and advisory committees will minimize the risk of industry influence through normal course operations, it would not, on its own, address the issue of accountability.

Since OSFI derives its authority from Parliament, we recommend that Parliament play an active role in overseeing OSFI. One option would be to legally require OSFI to regularly appear before the House of Commons Standing Committee on Finance (FINA) and the Senate Standing Committee on Banking, Commerce, and the Economy (BANC). To our knowledge, the Superintendent last appeared before BANC in October 2025 and before FINA in 2024.

Regular appearances have proven effective for other institutions, such as the Bank of Canada, by strengthening transparency without compromising independence or responsiveness to emerging risks. Although not legally required to do so, the Bank of Canada appears before Parliament at least twice a year (Binette and Tchebotarev 2019). In 2024, the Standing Senate Committee on Banking, Commerce, and the Economy released a report on the conduct of monetary policy in Canada, in which it recommended formalizing this practice to strengthen accountability and transparency (Senate 2024).

In addition to stronger governance and parliamentary oversight, OSFI would benefit from a structured periodic review of its governance framework, similar to the IMF’s Financial Sector Assessment Program but focused on the regulator itself. In its nearly four decades of existence, the MacKay Task Force has been the only review of OSFI’s governance, and that was nearly 30 years ago. Establishing a formal review cycle, at least once every decade, would ensure that OSFI’s governance remains current, aligned with international best practices, and capable of supporting an increasingly complex financial sector.

Conclusion

The OSFI Act states that its purpose “…is to ensure that financial institutions and pension plans are regulated by an office of the Government of Canada so as to contribute to public confidence in the Canadian financial system.” Since its creation in 1987, OSFI has played an important role in upholding that confidence. Yet the environment in which Canadian financial institutions operate has changed dramatically and continues to evolve due to forces such as digitalization, artificial intelligence, climate-related risks, and geopolitical uncertainty.