As a double immigrant who worked his way through high school and university, I am a big believer in the lifelong benefits of working on the front line, early in life. My first job was an eye opener to say the least.

As a double immigrant who worked his way through high school and university, I am a big believer in the lifelong benefits of working on the front line. My first job was in frontline customer service at age 16 for Canada’s largest sports store chain, Collegiate Sports (now Sport Chek), in a flagship mall in Toronto. I started as a salesclerk selling shoes, retail apparel, ski equipment, and stringing tennis racquets.

As a student athlete, I was fortunate to work in a large sports department store situated in a multicultural city and to serve all kinds of people across various ages and income groups.

Our customers ranged from consummate “old stock Canadian” athletes, who were fanatical about every detail when ordering custom equipment, to wide-eyed gullible immigrants whose children were seeking to learn a new sport like ice hockey or snowboarding. It was a fast paced atmosphere with dense traffic in the evenings and buzzing with energy on the weekends like a casino hotel on the Las Vegas strip.

It was also a very demanding job because it required being on your feet for 8 hours per shift and being constantly “switched on” to anticipate customer needs. Employees engaged in their first front line customer service role developed emotional intelligence through hundreds of daily interactions with customers. Over time, I learned how to read customers’ non-verbal facial expressions and body language, which varied widely by their ethnicities, stage of life, and other factors.

The job required meticulous knowledge of every major sporting activity, current and incoming inventory, and prices for disparate product lines and brands while also including labor intensive tasks such as tagging the products, stocking the shelves, and cleaning the store after hours. Determining the best allocation of shelf space was a key decision. There were no “smart technologies” such as sensors, cameras, big data, and analytics used by retailers today to manage inventories and shelf-space. Hence arranging the optimal product assortment on the floor to generate traffic was an essential part of the job that required teamwork and an entrepreneurial mindset of experimentation through trial and error.

The store manager was a flamboyant French-Canadian named Guy who was a die-hard Montreal Canadiens fan with a profound sense of humor.

Typical of 1980s Toronto, the staff was composed of up-and-comers, including many Asian, European, and Caribbean immigrants. Guy was great at motivating staff, casting people in the right departments, creating internal sales contests, and holding us accountable. He had a keen eye for talent and was adept at identifying and investing in adaptive learners who could conquer a multifaceted department such as ski equipment or hockey skates by efficiently conveying product knowledge to outsell others.

Guy’s greatest skill was building an informal talent marketplace to grow the business in one of the world’s most diverse cities. He understood that a high performing diverse team of employees who felt like the store was their own business would not just generate loyal customers but grow the sports retail business by engaging new communities. Under his leadership, the store became an incredibly diverse meritocracy of over 500 full time and part time employees: Caribbean kids rose from selling track shoes to managing winter sports and Asian women ascended from selling apparel to assistant manager roles overseeing budgets and purchasing. I remember training a Jamaican immigrant, who happened to be the best sprinter in Toronto, how to string tennis racquets at optimal tensions depending on the player’s style, and she taught me about the subtle differences in track and field spikes depending on specific events and surfaces.

Like any store environment, it was not always pleasant. When the store missed its numbers by a wide margin, Guy scolded us for not being sufficiently productive.

He would curse at us with Quebecois nouns, poke fun at our beloved Toronto Maple Leafs, and if revenues were under budget, walk us back to his office which doubled as “banc des pénalités” (“penalty box”). His diminutive office was adjacent to the boisterous warehouse receiving truck shipments, welding, and assembling equipment. Here Guy would shout out the disappointing financial results and present the dormant inventory and the blue-collar workers whose strenuous labor made it possible for us to sell these products on the floor. He reminded us that even the most talented players end up in the penalty box and cost their team when they fail to play together and trust their teammates.

Over the course of four years, this job taught me three things I would use in the rest of my career: First, the benefits of building a high-performing team of diverse colleagues who could teach each other through an apprenticeship model rather than formal training; second, how professional development is accelerated by highly demanding customers who make purchase decisions in a matter of seconds; and third, how the real world has a magical way of revealing where your greatest talents reside, even if it contradicts what your teachers and test scores suggest are your perceived strengths.

In my last year on the job, Guy got promoted to regional VP overseeing 100 stores in Eastern Canada.

Still, he sought me out once every few months. In our last few meetings, he expressed his gratitude that I helped recruit tens of what he called “gens talentueux” or highly talented and diverse employees – mostly high school athletes and musicians – that drew waves of new customers into his stores and grew the business. The last few times we met, Guy tried to persuade me to become a store manager and retail executive like he was. As an Asian immigrant with Ivy League dreams, I was not ready to take the store manager career path.

However, years later after graduate school and a stint in management consulting, I joined the hospitality industry where I was able to harness this cross-cultural competence to achieve breakthrough results. And when I became an operating executive and eventually a hospitality CEO, it made an even bigger difference. Thanks to years on the front line, I was able to swiftly unearth customer needs, connect deeply with front line employees and build collaborative cross-cultural teams. My front line experience was most helpful in relating to employees in emerging markets such as Shanghai where I had no prior work experience, did not speak the language, and had to motivate migrant workers, mostly mothers living apart from their children.

It was my years serving on the frontline in retail, sports, and healthcare that taught me to how to collaborate with colleagues, look customers in the eye and resolve their complaints, form teams to solve thorny problems, and meet the litmus test of becoming a leader by identifying and developing other people’s talents.

Service industries are not just the largest employers: they are engines of human development for communities, cities, countries, and entire civilizations. From the United States to China and Saudi Arabia, business, and government leaders “get it” and are investing billions to rebuild human capital in hospitality centric service industries after the pandemic. These diverse stakeholders recognize the critical role of service industries in rebuilding their countries, diversifying their economies, and facilitating meritocracy for domestic and foreign employees of all ages, races, ethnicities, and genders.

Surprisingly, their efforts are increasingly lost on the workforce. Instead, a talent disruption, powered by innovative technologies such as generative AI, changing attitudes towards work-life balance, and a growing mistrust of capitalism and governments is changing the equation. Millions of Gen Xers and Millennials are choosing the gig economy or hybrid jobs where they can effortlessly circumvent human interaction and avoid the discomfort of face-to-face conflicts. Groundbreaking technologies such as generative AI may accelerate this talent disruption, further distancing employees and contract workers and hence brands from their customers.

Consequently, brands that achieved differentiation through personalized service may suffer from commoditization. What is more troubling are the long-term career development implications for individuals, especially Gen Xers and Millennials who are set to become the next generation of service managers and grew up performing these gig economy jobs.

Driving around town and leaving bags at a front door with pictures, communicating via text confirmations, and receiving tips based on algorithms is not an equivalent experience to being on the frontline in a service operation.

It may provide contractors with flexibility and income, but it comes at the cost of a lack of learning and customer contact that will serve to stunt their professional growth. What is the solution here? Given this historic talent disruption, what is the path forward for business and government leaders in industries such as hospitality, retail, and healthcare that are experiencing long-term labor shortages and growing unionization? Should employers, including entrepreneurs such as franchisees, increase their investments in acquiring, developing, and compensating talents? Or should they invest in AI and other technologies to automate and reduce their investments in building human capital? What other alternatives, if any, exist?

When selling a house, one of the most challenging decisions is determining whether to accept the first offer and move on or wait for a better one to come along. According to Denis Smykalov, founder and broker of Wolsen Real Estate, there are several factors to consider when deciding whether to accept the first offer.

Mr. Smykalov believes that the quality of the offer goes beyond the price tag.

Denis Smykalov

A strong offer could entail fewer contingencies or a flexible closing date. If a buyer is pre-approved for a mortgage and is not asking for many contingencies, it may be in the seller’s best interest to accept the initial offer.

The current real estate market can also play a significant role in deciding whether to accept the first offer. It may be wise to accept a reasonable offer in a buyer’s market to avoid the property staying on the market for an extended period. On the other hand, in a seller’s market, where demand outpaces supply, sellers may receive offers that meet or exceed the asking price. If the buyer has strong financing, it could be a good idea to accept the first offer.

Speed is also a significant factor in determining whether to accept a first offer.

If the seller needs to move quickly or has already purchased another home, accepting the first offer might be the best option. In these cases, a bird in the hand is often worth two in the bush.

Feedback from a real estate agent is also essential in making a decision. A good agent understands the market and can advise whether the initial offer is competitive based on the current conditions.

Lastly, if the seller believes they have priced their home correctly and the first offer aligns with their expectations, it may be a good idea to accept it. Ultimately, only the seller can determine what offer price they are comfortable with. If the first offer meets that threshold, it could be a good time to make a deal.

It is essential to remember that each selling situation is unique, and these guidelines only provide a starting point. Sellers should always consult a real estate professional who understands their specific situation and the local market conditions.

In conclusion, accepting the first offer is a decision that requires careful consideration.

Denis Smykalov’s insights provide valuable guidance in determining whether the initial offer is the best option. With extensive experience in the industry, Mr. Smykalov’s expertise can help sellers make informed decisions when it comes to selling their home. For the Silo, Katherine Fleischman.

More about Denis:

Denis Smykalov built his career in the real estate industry over the last nine years by following his passion for being innovative, people and bringing the two together in the ideal environment. Achieving this goal so young, Smykalov decided to open an office in Sunny Isles Beach and became the owner of Wolsen Real Estate.

With business on the rise, at one point there were 65 agents. Now there are 25 agents, a marketing department, social media department sales department and 3 assistants that have successfully helped bring in almost 80 million dollars in sales this year. His most notable accomplishments with Wolsen Real Estate were two crypto transactions. One was a resale at Marina Blue for $465,000, pre-construction at Waldorf Astoria for over $2.5 million as well as a villa sale on Hibiscus Island for $19 million.

May 9, 2023 – Investor-state disputes are proliferating around the globe as business investors seek redress for government actions they deem unfair or contrary to investment agreements, according to report from the C.D. Howe Institute. In “Investor-State Disputes: The Record and the Reforms Needed for the Road Ahead,” author and C.D. Howe Institute Senior Fellow Lawrence L. Herman reviews the record of investor-state dispute settlement (ISDS) procedures, the criticisms directed at them, and the reforms required.

“Despite concerns and criticism, ISDS procedures in international investment agreements are an important development in global governance that should continue to be a part of our international fabric,” says Herman.

Herman examines both Canadian and global cases involving ISDSs, which give private parties the right to bring binding arbitration against governments under International Investment Agreements (IIAs). These rights can be invoked when investors allege a lack of fair and equitable treatment, discrimination or expropriation without adequate compensation contrary to a country’s treaty obligations.

“ISDS has become a significant feature for investments, particularly into developing countries in many parts of the world,” according to Herman.

“However, because of the rights given to private parties, these agreements have become increasingly controversial – especially in an era of increasingly expanding governmental measures on climate change, sustainability, human rights and other issues impacting foreign investors and their investments in one way or another.”

In response to these concerns, multilateral, regional and bilateral efforts are making continuing improvements to ISDS mechanisms when it comes to efficiency, transparency and aspects such as permanent appointments and a system of appeals.

“While some countries have embarked on a program of terminating their bilateral investment agreements, these agreements will continue to remain as a part of the international fabric in many parts of the globe,” says Herman. “They are an important development in global governance and, even if not perfect, they not going to disappear in spite of concerns and criticisms.”

Creating permanent rosters of tribunal members as well as adding an appellate review processes to existing IIAs would help improve ISDS procedures. Short of this, Herman says ongoing efforts could include: i) promoting model arbitration clauses to reduce legal uncertainty and enhance consistency and predictability of outcomes; ii) developing codes of conduct and best practices for adjudicators plus rules to ensure their independence; and iii) making sure appointments to tribunals are of highest quality. Governments should also publicly support the value of third-party arbitration as an objective and neutral process that leads to peaceful resolution of differences, he adds.

Ultimately, investment protection treaties are about risk mitigation with host states bound by treaty to respect obligations of fair and equitable treatment and other rule-of-law standards and providing investors with a degree of assurance, says Herman. “While there are legitimate questions about the process and whether and to what degree investment treaties accomplish these objectives, these suggestions can assist in providing ways forward,” he concludes.

There are some 2,500 international investment agreements (IIAs) in force around the world, whether as stand-alone treaties or incorporated into bilateral or regional free trade agreements (FTAs). They are a significant feature of the international business scene.

A main feature of these agreements is to allow foreign investors to invoke binding arbitration where it is alleged that the host governments have breached fair and equitable treatment and other treaty obligations towards the investors. This is known as Investor-State Dispute Settlement or “ISDS”.

The process gives foreign investors comfort that if things go wrong in host countries, they have recourse to neutral, third-party dispute resolution. It thus provides important elements of risk reduction for foreign investors and their investments, notably aiding the flow of capital from industrialized countries to the developing world.

There has been dramatic escalation of investor arbitration claims over the last two decades. This makes it timely and useful to review the situation, looking at the value of ISDS as well as the criticisms that have emerged over the years. The conclusion is that IIAs and the arbitration process are valuable parts of the corpus of international order and will remain an integral part of the international business scene for the foreseeable future. The issue facing governments, therefore, is how to respond to criticisms by improving, as opposed to abandoning, the ISDS process. This paper suggests some pragmatic ways forward.

A Canadian company, First Quantum Minerals, and the government of Panama are reported to have settled a long-standing tax dispute allowing the company to resume operations at the Cobre Panama mine in that country. Earlier reports were that if the dispute was not resolved by negotiation, the company would invoke arbitration rights under the Canada-Panama Free Trade Agreement.

Had the dispute proceeded, it would have been another example of hundreds of arbitrations that have proliferated around the globe, initiated under various international investment agreements (IIAs) that give private parties the right to bring binding arbitration against governments under Investor-State Dispute Settlement ( ISDS) procedures. Those rights can be invoked, for example, where investors allege lack of fair and equitable treatment, discrimination or expropriation without adequate compensation contrary to that country’s treaty obligations.

In addition to investment treaties, numerous free trade agreements incorporate separate investment dispute settlement provisions, including the former North American Free Trade Agreement (NAFTA); the Canada-EU trade agreement (CETA); the Trans-Pacific Partnership (CPTPP) Agreement; and bilateral free trade agreements, such as those between Canada and countries like Chile and South Korea, among others.

As a consequence, ISDS has become a significant feature of the ground rules for investments in many parts of the world, particularly those made into developing countries. Because of the rights given to private parties, these agreements have become increasingly controversial, especially in an era of expanding governmental measures on climate change, sustainability, human rights and more that impact foreign investors and their investments.

In light of these developments, it is useful to briefly update the ISDS record with regard to Canada, look at what lessons might emerge, both in the global and the Canadian context, and suggest some elements to monitor as we go forward.

Criticisms Of ISDS Agreements

As investor arbitrations have proliferated, so have the criticisms, making ISDS one of the more controversial aspects of global governance. Here are some of the main ones:

IIAs have given private companies broad rights to challenge host-country actions that can fall within legitimate fields of public regulation, especially now in an era of decarbonization and other national crises like COVID 19.

The process involves one-way litigation, with no corresponding right of host countries to bring arbitration cases against investors for disregarding laws, practices and standards of business conduct.

The growth of third-party financings of investor claims has stimulated, or at least encouraged, the initiation of ISDS cases.

Investment agreements bypass the customary international law norm that requires claimants to first exhaust local remedies before bringing an international claim against a host country.

The ISDS structure is defective because its ad hoc tribunals – put together to hear a particular case – make long-term, binding decisions affecting laws or policies enacted for the public interest.

Arbitrators’ decisions are final and binding with no avenue of appeal, whether on errors of fact or of law.

Because of its ad hoc nature, the system lacks institutional continuity. Public confidence in the system suffers.

Arbitrators are appointed from a small — if not closed – pool of international lawyers who are free to act for private interests as counsel in other cases, leading to appearances of conflict and adding to diminished public confidence in the process.7

There are answers to these critiques but the over-arching response, as alluded to above, is that resolving investor-state disputes based on legal norms within an accepted procedural framework remains a significant achievement in the progressive development of international law. As observed in one analysis,

“During the last decade a number of the shortcomings have indeed been addressed and remedied. It is reasonable to assume that this has been done – at least partially – based on the realisation that investment treaty arbitration is the most efficient and reliable dispute settlement mechanism for disputes between foreign investors and host States. There is simply no better, realistic alternative.”8

As already mentioned, ISDS in its various manifestations provides an important element of stability and risk insurance when investing in jurisdictions where legal rules may not be mature or respected, aiding the flow of capital to developing countries and thus presumably helping to meet the international community’s aid and development goals. The system may not be perfect, but efforts are afoot to improve it at many levels.

The author thanks Daniel Schwanen, Charles-Emmanuel Côté, Rick Ekstein, Ari Van Assche, Gus Van Harten and anonymous reviewers for comments on an earlier draft. The author retains responsibility for any errors and the views expressed.

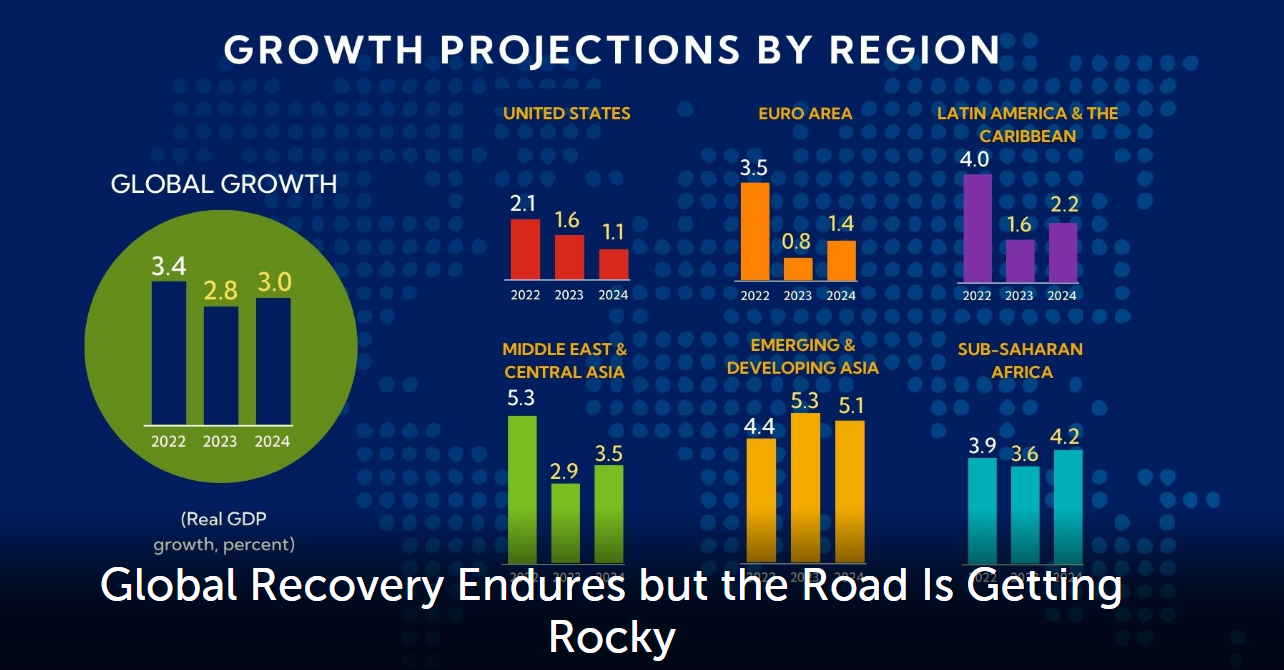

The IMF announced today (Tuesday, April 11, 2023) in the World Economic Outlook’s press briefing that the baseline forecast for global output growth is 0.1 percentage point lower than predicted in the January 2023 WEO Update, before rising to 3.0 percent in 2024.

“The world economy is still recovering from the unprecedented upheavals of the last three years, and the recent banking turmoil has increased uncertainties.”

“We expect global output growth to fall from 3.4% last year to 2.8% in 2023, before rising to 3% in 2024, mostly unchanged from our January projections. Advanced economies are expected to see an especially pronounced growth slowdown from 2.7% in 2022 to 1.3% in 2023. Global headline inflation is set to fall from 8.7% in 2022 to 7% in 2023 on the back of lower commodity prices but underlying core inflation is proving to be stickier. Importantly, this outlook assumes that recent financial stresses remain contained,” said Pierre-Olivier Gourinchas, the IMF’s Chief Economist.

Much uncertainty clouds the short- and medium-term outlook as the global economy adjusts to the shocks of 2020–22 and the recent financial sector turmoil. Recession concerns have gained prominence, while worries about stubbornly high inflation persist.

“Once again, risks are heavily tilted to the downside, they have risen with the recent financial turmoil. Most prominently, recent banking system turbulence could result in a sharper and more persistent tightening of global financial conditions. The simultaneous rate hikes across countries could have more contractionary effects than expected, especially as debt levels are at historical highs. There might be a need for more monetary tightening if inflation remains stickier than expected. These risks and more could all materialize at a time when policymakers face much more limited policy space to offset negative shocks, especially in low-income countries,” added Gourinchas.

With the fog around current and prospective economic conditions thickening, policymakers have a narrow path to walk towards restoring price stability while avoiding a recession and maintaining financial stability. Achieving strong, sustainable, and inclusive growth will require policymakers to stay agile and be ready to adjust as information becomes available.

“First, as long as financial stress is not systemic as it is now, the fight against inflation should remain the priority for central banks. Second, to safeguard financial stability, central banks should use separate tools and communicate their objectives clearly to avoid unwarranted volatility. Financial policies should remain laser focused on preserving financial stability and watch for any buildup of risks in banks, non-banks, and the real estate sectors. Third, in many countries fiscal policy should tighten to ease inflation pressures, restore debt sustainability, and rebuild fiscal buffers. Finally, in the event of capital outflows that raise financial stability risks, emerging market and developing economies should use the integrated Policy framework, combining temporary targeted foreign exchange interventions and capital flow measures where appropriate,” said Gourinchas.

Over 5,800 Metaverse Trademark Applications Filed Last Year = Surging 200% Year-Over-Year

In 2022, there was a significant surge in trademark applications related to the Metaverse and non-fungible tokens (NFTs), indicating the growing importance and potential profitability of these emerging industries.

According to data collected by Blockchain Centre, there were 5,850 new Metaverse trademark applications and 7,746 NFT trademark applications registered last year.

This represents a growth rate of 205.64% and 259.61%, respectively, from the previous year. The monthly trends for trademark registrations steadily increased throughout the year, with at least 300 new applications filed every month.

Increasing interest in the Metaverse

Many big companies, including Meta, Formula One, Mastercard, McDonald’s, Gatorade, and the US Space Force, have also filed applications with the USPTO in 2022, indicating their interest in virtual products and involvement with crypto and blockchain.

The rise in trademark applications related to the Metaverse and NFTs has prompted an investigation by the US Patent and Trademark Office and US Copyright Office to examine how NFTs impact intellectual property rights.

According to the research:

“Recently, several prominent brands have faced challenges when their intellectual property or products were infringed upon by NFT marketplaces or platforms.”

Despite the ongoing ‘crypto winter’, the rise in trademark applications and growing interest in metaverse products have served as a counterbalance to concerns that the market is being negatively impacted. For the Silo, Lina Alisauskaite.

A major money saving and environmentally beneficial smart kitchen app launched waaaaay back in 2015, on World Environment Day, and deserves another look as it still works well and saves users up to $1,000 every year and helps reduce food waste.

The “Smart Kitchen” EatBy App reduces food waste, saving households up to $1,000 per year and helps the environment.

The staggering amount of wasted food continues to make headlines and back when the app was first created, husband and wife developers, Steffan and Barbara Lewis were focusing their passion for finding a solution to the environmental issues surrounding food waste and came up with the idea to develop and launch “Smart Kitchen” EatBy as soon as possible.

“We had the idea one lunchtime after we had to throw out the food we’d hoped to eat because it had passed it’s use by date. That led to a purge of all the out of date food in our kitchen. And quite frankly, we were shocked and disgusted with ourselves when we realised how much we waste.” said Barbara Lewis.

They decided to make the app free to download and offer expanded use with an optional shopping list that can be activated with an in app purchase.

“It’s important to us that the app’s basic functions have to be free in order to gain and benefit the maximum number of users. Collectively we can all make a huge difference to the environment. And it’s an added bonus that we’ll save around £700 ($1,000) each year.”

And the numbers add up.

Recent reports state that the average household wastes $80 usd ($109.23 CAD) every month on un eaten food. With over 123 million U.S. households that’s $9,840,000,000. Factor in similar habits throughout the rest of North America and an equivalent amount in Europe, the tally is somewhere around a staggering $236 Billion each year. It’s known that about one third of all food produced is discarded but the real cost to the environment is misunderstood: 1.3 billion tonnes of wasted food contributes 10% of worldwide total greenhouse gases.

Many strategies for reducing food waste have been proposed by environmentalists, government agencies and industry specialists. But the husband and wife creators of the EatBy App claim their app is the first practical personal tech solution to the problem of food waste. It is a simple to use Smart Kitchen App that effectively helps manage the food in your kitchen and lets you know when food items expire. The optional integrated shopping list will also help reduce buying too much food in the first place.

“We are under no illusion that our app will immediately solve this global problem,” Said Steffan Lewis, “But if only a few million people download and use it, then it’ll already make an impact and that’d be a great start. Obviously, we’d like everyone to use our app and benefit from it!”

The EatBy App is available for both Android and Apple devices. More information about the project’s history can be found at https://www.eatbyapp.com

The recent rise of Artificial intelligence (AI) programs such as ChatGPT has created a frenzy around AI-related stocks.

C3.AI, a pure play AI stock, is up over 100% since late December.

But is this rally sustainable? After all, the public was already surrounded by AI without realizing it. Almost everything people use in daily life is affected by AI already:

advertising

entertainment streaming services

social media

cars (collision detection and blind spot monitoring)

fraud prevention

screening job applicants

email spam filters

many other applications

C3.AI is a company that creates software to help other companies deploy AI projects. C3 software is being used in multiple ways, including managing inventories, monitoring for energy inefficiencies, and predicting system failures. [Of particular note is one new product from C3 called ex machina which allows users to program AI initiatives without using any coding at all but instead via a series of visual programming tools. CP]

AI stocks, and technology stocks as a whole, were a neglected market in 2022. The Nasdaq 100, an index heavy in technology stock, fell more than 30% in 2022. C3.AI fell over 65% in 2022, and is currently down almost 90% from its 2020 high (even after the 100% rally in 2023). All currency quotes that follow are in USD.

C3.AI recently peaked at $30.92 on February 6. It then reached a low of $20.31 on March 1 before rallying back to $29.98. It has since fallen and is back near the $20.33 low.

This puts the stock at a crucial level.

An analyst from SafeTradeBinaryOptions.com had this input: “Right now, the stock is in an uptrend, albeit a precarious one. The price has been making higher swing lows and higher swing highs throughout 2023. But if the price drops much below $20, that will no longer be the case. The price will have made a lower high on March 6 (compared to February 6) and if the price drops below the March 2 low, that is a lower low. These are signs of a downtrend starting — not an uptrend.”

All facets of our modern world are already in the embrace of A.I. whether we know it or not.

This $20 region is important because if the area holds, this indicates the price is moving in a range, with the possibility of the price moving back up to the top of the range near $29. If that happens, there is still hope that the price will eventually break out of the range to upside, continuing its advance to $40, for example.

However, if the price drops below the $20 region, the range is broken and the uptrend is in jeopardy.

It’s important to watch C3.AI to see how investors are perceiving the future of AI, and what that may mean for the industry’s future.

As of March 2023, C3 doesn’t have a lot of direct competition. The company is not yet even profitable. How the stock moves is based on whether investors believe the company can eventually generate profits — and in this case, its profits largely depend on whether AI becomes even more widespread than it already is. For the Silo, Kat Fleischman.

Pi Network increased its team member headcount by nearly 33% over the past year, debuted new developer features and KYCd 3.8M community members to-date

PALO ALTO, Calif., March, 2023 /– Pi Network, a community of tens of millions of humans mining Pi cryptocurrency to use and build the Web3 app ecosystem, today announced a series of milestones for the growing organization, including a notable spike in full-time Core Team members, multiple app developments and new improvements to its native KYC ID review algorithms.

March 14 (3-1-4) is Pi day

Despite the overall crypto market contraction, the Pi Core Team continues to grow, signaling the speedy development of the Pi Network ecosystem and its long-term vision.

Since February of 2022, full-time team member headcount has increased almost 33% in critical areas such as product, engineering, and community. Pi Network’s most recent hires include a new Senior Engineering Manager who will add more bandwidth to its technology management. The Pi Core team now stands around 40 strong and continues growing as the network expands and the ecosystem evolves.

“Given the breadth of work at Pi Network, the Core Team’s growth will continue to enable more decentralized efforts from our community of over 35 million engaged members who collectively build this network. Pi Network’s work is to empower those members in alignment with Pi’s vision of an ecosystem that is built on the blockchain to support a new Web3 social network of a large community, all of whom are empowered to create and use utilities through its developer’s platform and Pi apps. Building for that ambitious vision requires an all-hands approach from Pioneers, community developers, external partners, and the Core Team together,” said Chengdiao Fan, a Founder and Head of Product at Pi Network.

“By prioritizing the human aspect, focusing on building substance and adopting non-consensus long-term strategies, we’ve taken a more careful and deliberate path. We know that patience isn’t a strength in the crypto space but we’re confident in our approach: that’s why we’ve been able to continue the Network’s steady growth despite the downturn we’ve seen impacting some other crypto projects.”

In addition, Pi Network has taken great strides in the product and ecosystem fronts with numerous updates and developments.

Pi’s current Enclosed Network period of Mainnet allows Pi to focus on completing KYC and Mainnet Migration for the majority of the network, and bootstrapping the Pi ecosystem with meaningful apps and utilities, without undue influence from external factors.

To that end, Pi has been diligently improving its KYC ID algorithms to expand access to its native KYC solution, officially launched March 14, 2022, as the primary mechanism to validate Pioneers’ identities for Mainnet Migration. Since enabling mass KYC in June of last year, Pi has successfully validated over 3.8 million Pioneers to date.

Simultaneously, Pi has made significant efforts in building Developer Platform features and expanding community collaboration to foster Pi ecosystem growth, including the launch of PiOS, Pi’s Open Source Software License which allows Pi Community Developers to create open source applications and tools and exclusively extends to use within the Pi Ecosystem. Recent ecosystem-related updates include work on App-to-User payments and Developer Wallets for improved Mainnet payment flows, the Pi “Brainstorm” app (where “Pioneers” can propose and explore various ideas and pair up with like-minded Pioneers to build real Pi platform apps, and more.

Moreover, Pi has emphasized app development through Core-Team-developed apps, external business partnerships, and the most recent Pi Hackathon which hosted over 6,400 participants, all to better source talent, concepts, and utilities for the community.

“With the much-anticipated ‘Pi Day’—which celebrates the 4th anniversary of Pi’s official launch—happening this March 14, we have some exciting programs in the pipeline that we are eager to introduce to the Pioneers and developers for our decentralized efforts to build the Pi ecosystem,” said Dr. Nicolas Kokkalis, a Founder and Head of Technology. “At Pi, we’re creating things and solving problems in a way that the world hasn’t seen before.”

To learn more about Pi Network, please visit minepi.com.

ABOUT PI NETWORK

Pi Network is a community of tens of millions of humans mining Pi cryptocurrency to use and build the Web3 app ecosystem. Founded in 2018 by Stanford University PhDs with specializations in blockchain and social computing, Pi Network is a utilities-based ecosystem for third-party apps on a mobile web platform, with widespread (rather than concentrated) token distribution. The blockchain platform offers a mobile-first mining approach, with low financial cost and a light environmental footprint within the crypto space.

Bookkeeping is tedious for most business owners unless you are a seasoned accountant or a fan of working with numbers. That is because businesses have a lot of financial details that need to be recorded, for instance, which supplier should be paid, outstanding customers, equipment to buy, significant purchases to make, and more. Without an accounting and bookkeeping system, you may lose essential business data, miss important goals, or make uninformed decisions that may affect your company’s finances.

Proper money-handling strategies are integral in any business as it helps you keep track of your long-term goals, improve your profits, and streamline seasonal cash flow changes. In addition, it will help your business stay out of trouble with the Internal Revenue Service or IRS.

By adopting good bookkeeping habits, you can avoid costly errors when it comes to record keeping. You can opt to have an in-house team to handle all your bookkeeping services, but this can be un-economical for small business owners. To save on cost, you can work with a bookkeeping agency, which often offers professional online and virtual services in Canada at very fair rates.

Here are seven tips for better bookkeeping for businesses in Canada.

Separate Your Business and Personal Finances

If you are a sole business owner, you should learn to separate your personal and business accounts. This will help you maintain records of every business and personal spending and help you keep the boundary to alleviate eating into the business growth finances.

For limited liability companies, the business is a separate entity from you, and your finances should be kept separate. That means you need to know which assets belong to the business and which are yours. By eliminating all personal transactions from the business accounts, you will lower the number of transactions the bookkeeper needs to categorize and reconcile. Additionally, your tax preparation and filing process will be seamless. You can find a bookkeeper in Canada to help you separate your accounts and provide outsourced business and personal bookkeeping services.

Control Your Business Credit

One of the common signs of an insolvent business is the inability to make payments promptly. The company may need better credit scores, lack of funding, or challenges in fulfilling its working capital needs.

When your business depends on bank financing to fund everyday operations, you will need help to pay back your high-interest debt. Therefore, you need to do due diligence before taking external funding.

You should set strict deadlines for your clients to pay what they owe and consider blocklisting repeat offenders that are taking advantage of you. Eliminate any late payments, as it is just like an interest-free loan. Your business may quickly become a cash-flow crisis if you lack rigorous credit control.

Track Business Expenses

Business expenses may be claimed against tax; therefore, tracking them is crucial if you want to cut overhead and maintain a healthy cash flow. You should always use a business credit card and keep records of expenses based on business activity.

Categorizing your expenses can be crucial, especially when your business is undergoing an CRA audit. The numbers on tax returns are often estimates, and these records help offer supporting evidence. Always remember that even trivial expenses will add up, and having records of everything can be helpful in the long run.

Overspending negatively affects any business; hence, keeping track of your expenses will ensure you track all your expenditures. Always remember that every dollar that you spend takes the business one step away from making a profit. Therefore, when running a business, keep a close watch on all your expenses, understand the benefit you gain from each expense, and document everything carefully. With outsourced online bookkeeping services, you can keep track of all your business expenses and maintain good records.

Schedule Routine Bookkeeping Times

As a business owner, you are handling many things at once, which can eat into the time you can use to monitor your financial record books.

The best way to keep your accounts is by consistently scheduling times to balance your books or working with a bookkeeping company in Canada. You can set aside time when your credit card statement is due and check through your monthly transactions to ensure everything is accurate. Although this task will take about one or two hours, it will simplify your life during the tax season by making tax preparation and filing much more effortless.

Create Budgets For Your Expenses And Set Financial Goals

Planning for business expenses, especially significant purchases, can help you best utilize your business resources and credit while giving you the peace of mind you need. Setting up and reviewing business budgets is directly related to the success of your business.

According to research, small businesses that regularly review their budgets on a weekly, monthly, and annual basis have success rates of 95%, 75%, and 25%, respectively. Therefore, if you want your business to succeed, you must have relatively high unused credit balances. In addition, you should also ensure your budget is monitored regularly, understand the benefits of using credit for your company, and be able to earmark the right amount of business payroll expenses.

Automate Manual Processes

One of the best accounting tips for growing businesses and start-ups is automating routine bookkeeping. Most accounting and bookkeeping activities are repetitive, and automating them will make your work easier and seamless.

Some repetitive bookkeeping processes you can automate include paying employees’ salaries monthly, following up on late invoices, and tracking invoices you send to customers. In addition, you can also automate the calculation of mileage payments for employee reimbursements and document utility bills in a central database.

Business owners can make life much easier by utilizing unified accounting project management solutions to help track expenses, automatically send invoices, and generate customized reports.

Consider Hiring a Tax Accountant

Investing in a seasoned tax accountant near me can be valuable for your business, even if the professional commits just a few hours every week or month to work on your small business bookkeeping and accounting needs.

A certified bookkeeper will record income and expenses and categorize them for a specified period. Conversely, a chartered accountant will help file your business taxes and set up your business’s accounting backbone. A reputable bookkeeping company will have certified tax consultants near me ready to assist you.

With an expert bookkeeper or chartered accountant handling all financial tasks, business owners can focus entirely on their business to attract customers and satisfy existing clients. They can also develop new products and services and grow their business.

Final Thoughts

Bookkeeping is a necessary evil that businesses cannot escape because almost everything depends on it. With an accurate and robust accounting system, you will get information about the business’s cash flow, performance, and financial condition, and it will help you make informed financial decisions. With the tips mentioned above in mind, you can ensure your small business bookkeeping records are available and can make better decisions for your business. You can also eliminate the headache of bookkeeping by outsourcing this function to a certified bookkeeper to help you out. Having a safe pair of skilled hands providing bookkeeping services for small businesses will give you, as the business owner, the confidence and freedom to lead from the front by focusing more on growing your business.

The gaming industry is undergoing a significant shift. The payments ecosystem is evolving towards a new era of cryptocurrencies and e-wallets and away from conventional online banking accounts. According to our friends at LotteryCritic.com, the impact of this changing payments ecosystem is multifaceted, affecting everything from the speed of transactions to how funds are stored and managed. Freddie Smith, CEO of LotteryCritic, commented:

Integrating crypto and e-wallet payments into the gaming industry is particularly advantageous because it eliminates the need for third-party payment processors. This means that users don’t have to go through traditional banking channels, which can be slow and unreliable. Moreover, crypto and e-wallet payments are more secure than traditional systems since they use sophisticated encryption algorithms.

Advantages and Opportunities of Cryptocurrency and E-wallets in the Gaming Industry

Cryptocurrency has widespread recognition as a form of payment, and the gaming industry is no exception. Many online gaming platforms now accept cryptos. Therefore, players can use them to buy in-game items or to place bets. The use of cryptos in the gaming industry offers several benefits. They include lower transaction fees, fast and secure transactions, and anonymity for players. E-wallets have also become increasingly popular in the gaming industry. Players use them to store funds and make transactions within the gaming platform. E-wallets offer several advantages, such as ease of use, fast dealings, and storing multiple currencies in one account. With the integration of e-wallets and cryptos, players can make quick and secure transactions.

The adoption of cryptos and e-wallets in the gaming industry has also opened up new revenue streams for gaming companies. For example, some gaming companies now offer in-game purchases using cryptocurrencies. Thus, allowing players to buy items using their digital assets. This has created a new market for gaming companies and has provided an opportunity for them to increase their revenue.

Challenges in the Adoption of Cryptocurrency and E-wallets in the Gaming Industry

The gaming industry has seen a rise in adopting crypto and e-wallets as payment. While these payment methods offer several benefits, adopting cryptos and e-wallets has challenges. One of the significant challenges is the volatility of crypto prices. Crypto prices can fluctuate rapidly and unpredictably. Thus, it can affect the value of in-game purchases made using cryptocurrencies.

The unpredictability can create confusion for both gaming companies and players. Besides, there is also a need for more regulation in the cryptocurrency market. The lack of rules makes it difficult for gaming firms to operate within a legal framework.

Moreover, the lack of regulation also exposes players to security risks, such as hacking and theft. Integrating cryptocurrencies and e-wallets into the gaming industry can also present technical challenges. Investors must ensure systems and processes used for transactions are secure and user-friendly. This requires significant investment in technology and infrastructure. The cost implications can hinder small and medium-sized gaming firms from investing. For the Silo, Elizabeth Kerr.

Pi- the only crypto you can mine from your smartphone.

Royalties Are Bullshit: A Musician’s Case For Basic Income….. “This song is Copyrighted in U.S., under Seal of Copyright #154085, for a period of 28 years, and anybody caught singin’ it without our permission, will be mighty good friends of ourn, cause we don’t give a dern. Publish it. Write it. Sing it. Swing to it. Yodel it. We wrote it, that’s all we wanted to do.”

-Woody Guthrie, copyright notice, This Land Is Your Land

Royalties are bullshit.

I say this as a musician, and as a songwriter. But let me go a step further: royalties have always been bullshit. The first problem? They’re not going to musicians, and they never have.

If money is being made, something is being sold. That something has to be a product, something that can be counted. Originally it would have been sheet music, before recorded music was widely available. Later on, it meant records, then tapes, CDs, downloads, streams, as well as licensing rights – use in a specific film, or for a particular commercial. There is a product. Someone is buying it. Some of that money goes towards the cost of producing, distributing, and marketing that product; some of it goes to the artist, as royalties.

Well, a little bit of it goes to the artist.

As Billboard notes, “An accurate map of royalty pathways would be a tangled mess.” It’s not easy to get paid.

Some royalties are set by the government, some are negotiated, some are paid through groups. For example, I license my music through TuneCore, which strikes deals with a series of digital music outlets, like iTunes and Spotify, each of which offers different terms of payment. Spotify pays artists, on average, $0.007 cents per stream.

Example of royalties earned for artist Jarrod Barker. Russian streamer Yandex awarded 8/100th of a penny for track streaming. Mr. Barker would need 99,992 additional streams to earn a dollar!

Beyond that, if you are “fortunate” enough to work with a major record label, there are restrictive terms and conditions. Techdirt quotes Tim Quirk of Too Much Joy explaining the Kafkaesque math [emphasis mine]:

A word here about that unrecouped balance, for those uninitiated in the complex mechanics of major label accounting. While our royalty statement shows Too Much Joy in the red with Warner Bros. (now by only $395,214.71 after that $62.47 digital windfall), this doesn’t mean Warner “lost” nearly $400,000 on the band. That’s how much they spent on us, and we don’t see any royalty checks until it’s paid back, but it doesn’t get paid back out of the full price of every album sold. It gets paid back out of the band’s share of every album sold, which is roughly 10% of the retail price. So, using round numbers to make the math as easy as possible to understand, let’s say Warner Bros. spent something like $450,000 total on TMJ. If Warner sold 15,000 copies of each of the three TMJ records they released at a wholesale price of $10 each, they would have earned back the $450,000. But if those records were retailing for $15, TMJ would have only paid back $67,500, and our statement would show an unrecouped balance of $382,500.

Of course, none of this is new, really. The history of artistsgettingscrewed by record labels is as long as the history of record labels, and includes everything from the creative math above to outright theft, failure to count sales, or inventive stunts like Fantasy Records accusing John Fogerty of plagiarizing himself. But bear with me, because it gets worse.

In the music industry today, there are a few people who are making money from royalties- and they’re making nearly all of it. More specifically, the top one percent of earners are taking in 77% of the recorded music revenue. Strikingly, these are many of the same artists who are now “at war” with YouTube. Artists such as Taylor Swift and Paul McCartney are convinced that YouTube is making money from their music by selling ads and subscriptions, and not paying adequate royalties. And they’re not wrong; YouTube is definitely making money by selling ads and subscriptions, and there’s no question that most of that is not going to the artists.

However, this is a stupid argument.

It’s a stupid argument because a tiny group of people that’s making the lion’s share of all recorded musical income is concerned that a new service doesn’t adequately compensate them; the major record labels feel the same way, of course. It’s a “war” that leaves out 99% of the musicians out there trying to make music and make a living, and it doesn’t really matter how they settle the conflict.

So let’s say, hypothetically, that we eliminate royalties. This raises a fundamental question.

How do we compensate and credit artists for their work?

I believe the answer is basic income, but first let’s take a closer look at that question. At a glance, it seems like it should be simple: pay them for their music. But what does that mean? It quickly gets complicated.

Part of the problem is that we as a culture equate value with ownership. If musicians have created a song, this thinking goes, and that song has value, they must own it, like any other form of property. But that’s ridiculous, and it’s pretty easy to see how quickly it becomes truly absurd.

For example, take a classic blues song, like Big Mama Thornton’s “Hound Dog.” Is that her tune? Yes! Does she deserve credit for it? Absolutely. Big Mama Thornton has a special place in blues history, and rightly so. But is it the first example of a 12-bar blues? No, of course not. Is it the first time someone used lyrics about a dog? Is it the first time someone used the call-and-response verse structure of a repeated first line and different last line? No, and no. And even though she made it a hit, the lyrics were by Leiber and Stoller. So which part of the song does she “own”? Is it just that specific recording? If so, how much does the bass player own, or the drummer? Do you pay royalties for playing it on the radio? What if it’s on the radio, and you tape it? What if you give that tape to a friend? I know, I know, nobody tapes anything off the radio anymore. What if you cover it in a bar? What if you sing it in your living room? What if you sing it in your living room and upload it to YouTube? What if you share the MP3? Where do we draw the lines?

Woody Guthrie, speaking from the folk music tradition, said “New words, new song.” Bob Dylan took that lesson to heart, both in early works like “Masters of War,” which took a melody from an English folk song called “Nottamun Town,” and in more recent releases. On Modern Times he lifted lines from a Civil War era Confederate poet named Henry Timrod, and used the arrangement of Muddy Waters’ “Rollin’ and Tumblin'” with re-written lyrics and the same title.

I don’t mean to discount Big Mama Thornton, or disparage Bob Dylan. I’m a big fan of both. What I want to illustrate is that “property” and “ownership” is a meaningless way to look at music, because it’s a living, inherited tradition. Everybody got something from somebody. Every electric guitar player owes something to T-Bone Walker, and T-Bone owes something to Blind Lemon Jefferson. Every folk singer owes something to Woody Guthrie and Pete Seeger. And more to the point, if you ask any great musician, they will tell you who they got it from. Eric Clapton tells people about Buddy Guy, but if you put a microphone in front of Buddy he’s going to tell you about Muddy Waters, BB King, Guitar Slim. The greats are always ready to turn around and credit the people who came before them, because that’s how a living musical tradition works.

So again: how do we compensate and credit artists for their work?

Splitting the question

One answer is to split up the question. When you think about it, it’s really two different questions. Let’s look at the second part first: how do we acknowledge and appreciate and credit the work that artists do? This is especially important because many important contributions to music, art, and human history generally, were made by people who get erased from popular culture- in particular women, LGBTQ folks, and people of color (Ma Rainey, for example, was all three). They are erased, in part, because there is money to be made by erasing them.

The uninformed still think “Hound Dog” and “That’s All Right” are Elvis Presley tunes. And while Presley himself was quick to credit his influences, most people have never heard of Arthur Crudup, and everyone’s heard of Elvis. Sometimes people were erased several times over; early blues music was driven by women like Bessie Smith, Ma Rainey, and Sister Rosetta Tharpe, who were largely displaced by black men, who then had their music co-opted by white guys playing rock’n’roll versions of the same songs. Some made serious efforts to show people where the music had its roots – The Rolling Stones, appearing on the show Shindig in 1965, insisted that Howlin’ Wolf also get to perform. On the other hand, Led Zeppelin took Willie Dixon’s song “You Need Love,” and recorded it as “Whole Lotta Love,” without ever mentioning where they got it. It’s ironic, since Dixon himself was notorious for taking credit and royalties for other people’s work, often by offering to “take care of the paperwork” on a new tune.

So how do we make sure we credit and acknowledge artists? One way, I believe, is to end a system of compensation based on owning something that cannot be owned. In a system like we have now, where the focus is on ownership of a particular sound, or song, or style, there is a real financial incentive to take credit. In the case of the record labels, you can even get the actual rights to an artist’s songs. If we disconnect the money from the “ownership” of the music, we are removing part of the incentive to pretend that new music doesn’t freely flow from old music.

Universal Basic Income

To be clear, I’m not suggesting artists should not be paid. There are different ways to support artists, and the internet has allowed for a lot of direct interaction between artists and fans. There are crowdfunding sites like Kickstarter and Patreon, there are independent music platforms like BandCamp and CDBaby. They’ve got their advantages and disadvantages, but what I’m advocating is something simpler, more widespread and direct: universal basic income.

Universal basic income, sometimes called emancipatory basic income or simply “basic income,” is an easy idea to understand: you give everybody money. Everybody. Rich people, poor people, working people, the unemployed, the young, the old, everybody. Everybody gets a salary. It’s not a lucrative salary, but enough to make sure you can provide for yourself.

First, let me clear something up: this is not a wild, crazy, utopian idea. It’s a serious proposal, that is increasinglybeingtreated as such. Even Forbes ran a piece called “Universal Basic Income Is Not Crazy.” Of course, it works better if you already have some of the social framework much of the world takes for granted: child care, family leave, health care. But let’s leave those aside for a moment to look at basic income from the musician’s perspective. What is the impact for working musicians?

Quit Your Day Job

Many, if not most, working musicians [and artists CP] support themselves with a day job. This includes long-time performers with steady gigs, people who have gone on world tours and recorded on dozens of albums. Buddy Guy drove a tow truck into his thirties. Composer Philip Glass worked as a plumber and taxi driver until he was 41. Wes Montgomery worked in a factory from 7am to 3pm and played gigs until 2am.

Let me tell you: it’s not easy. As a musician, you already have to balance many competing demands: playing gigs, traveling, booking and promoting shows, recording new material, rehearsing a band. Being a professional musician is, effectively, more than one job already. Now try to schedule all that around a conventional job structure that wants you working at 8 or 9 in the morning, 5 days a week, regardless of where you played last night or when you got home. It’s hard to fit all of it in, and that’s without stopping to consider that it might be nice to sleep occasionally or even see your family now and then.

One reason basic income is sometimes called “emancipatory” is because it frees you from this burden. You’re still going to be out there hustling for gigs, scheduling sessions, trying to record and promote and – let’s be real – get paid. Basic income doesn’t eliminate the desire or possibility for people to make money by working, it just means you don’t have to worry about starving or getting evicted while you do it. And let’s remember, most of the money musicians make doesn’t come from royalties anyway. People are getting paid for gigs, for shows, for studio sessions, for tours, sometimes for merchandise or direct sales (in particular if you’re producing your stuff independently).

Make The Music You Want To Make

Musicians make compromises all the time. Sometimes it’s about timing: you want to put something out, and you can’t afford to wait, so you settle- you keep a take that could have been better, you scratch a song that needs a few more sessions to come together. Sometimes it’s about the sound: a record label wants to market you a particular way, a track needs to be “radio friendly” to get airplay. Sometimes it’s just about resources: recording and producing music, even with all the advances in digital technology, is a laborious, expensive process. For some players, there’s also the trade-off between taking gigs that might pay better but be musically unfulfilling (think wedding band or corporate events) versus pursuing a musical vision that might not have a ready-made market. And, of course, there’s that most precious of all resources, time, which is often given over in huge amounts to the aforementioned day job.

Basic income removes the immediacy of financial pressures, and frees up a lot of time. Does that mean we won’t have choices to make? No, of course not. There are always choices, and there are always constraints, and even if we get basic income that won’t turn time itself into a limitless resource. But it changes the balance of the decision.

Creative Liberation: Supported By Research

Right now, across the country, there are brilliant artists whose music could change and enrich our culture in ways we can’t imagine, and we don’t get to hear them. They’re stuck working day jobs, playing the gigs that pay the bills, and trying to fit their creativity into commercial constraints. Pause for a moment, and imagine the explosion of new sounds and ideas we can liberate with basic income.

As a musician, that paragraph felt intuitively true to me. However, a number of people who were kind enough to review an early draft of this essay suggested that my point might be better served if I backed it up with “evidence” and “examples.” Of course, there’s not exactly a one-to-one comparison available, so I’m going to draw on some similar programs and related ideas.

First: the MacArthur “Genius” grants. These fellowships are awarded to people who are already recognized to be exceptional; they provide a no-strings-attached stipend of USD$625,000 over five years. Obviously that’s a lot more than “basic” income, but they underpin the idea that simply providing creative people with resources allows them greater freedom to explore, discover, and create. In a review of their program and its effectiveness, The MacArthur Foundation found that 93% of the fellows reported greater financial stability (no surprise) and 88% reported an increased opportunity to express creativity. Three quarters felt it lead them to make riskier, more ambitious choices in their work.

Some might argue that the fellowships exhibit a selection bias, since they go to people already known to be creative. However, there’s good reason to believe that supporting the poorest and most marginalized offers even greater benefits. Dissent magazine recounts the history of the Federal Writers Project, which offered “unemployed” writers guaranteed income by giving a fixed salary to produce travelogues or other commissioned writings:

…with regular paychecks, FWP writers could experiment with more creative projects at the same time. Over the course of eight years, the program employed over 6,600 writers, including Nelson Algren, Jack Conroy, Zora Neale Hurston, Richard Wright, and Ralph Ellison. The FWP enabled new classes of Americans to become “professional” writers.

While employed by the FWP, these writers—most notably writers of color—wrote fiction that challenged the political status quo, and they revolutionized literary form in order to do so. To be sure, many of these writers developed their politics in pre-FWP years, but stable employment facilitated their political and artistic ambitions—by providing them with steady income, connecting them to other writers, and offering literary inspiration. From 1936–37, between posts at the Federal Theatre Project and the FWP, Hurston wrote her beautiful and troubling novel Their Eyes Were Watching God, a book celebrated today for its inventive use of black vernacular. Wright spearheaded the “Chicago Renaissance,” a creative community strengthened and supported by FWP projects in the state of Illinois. Meanwhile, in New York City, Ellison was conducting FWP oral histories when, as he reported it, he stumbled across a man who described himself as “invisible.” This encounter would be the genesis for his Invisible Man, surely one of the strangest and most significant novels of the twentieth century.

I recognize that the subjective self-evaluation of MacArthur fellows and even the impressive work of FWP authors can be considered, to some extent, anecdotal evidence. But there is also controlled research, and what it shows is the flip side of the coin: that poverty impedes cognitive function. Lead by Harvard economist Sendhil Mullainathan, the team found that “experimentally induced thoughts about finances reduced cognitive performance among poor but not in well-off participants.” They also found that farmers showed diminished cognitive ability before harvest, when they were poor, compared to after harvest when they were relatively rich. That’s after controlling for free time, nutrition, work effort, and stress.

If you’ve ever been broke and had bills to pay, this is not news. It’s hard to focus when you have a huge bill hanging over your head and no immediate prospect for paying it off. When you’re in a position of financial hardship, a portion of your brain is effectively set aside to repeating over and over again, “AAAH THE RENT AAAH THE RENT AAAH THE RENT.” Or the hospital bill, or the car payment, etc. You know the classic sci-fi trope that imagines what you could do if you could harness the full power of your brain? Turns out it doesn’t require genetic engineering – you just need to be able to pay your bills.

I would argue that we are effectively paying a cultural opportunity cost in the form of lost creativity. Coming back to music, anthropologist David Graeber puts it this way:

“Back in the 20th century, every decade or so, England would create an incredible musical movement that would take over the world. Why is it not happening anymore? Well, all these bands were living on welfare! Take a bunch of working class kids, give them enough money for them to hang around and play together, and you get the Beatles. Where is the next John Lennon? Probably packing boxes in a supermarket somewhere.”

The Robot Imperative – It’s Not Just About Musicians

I realize we’re covering a lot of ground here, and we’re about to talk about robots. So first, a quick recap

Royalties don’t go to (most) musicians.

Royalties don’t make sense because they rely on ownership of something that cannot be meaningfully owned.

This system of ownership creates financial incentives to take credit for other people’s work.

Eliminating royalties forces us to confront the fundamental question of how we credit and compensate artists for their work.

Basic income answers part of that question – compensation – while eliminating royalties removes, at least in part, the financial incentive to take credit.

Basic income liberates musicians from the constraints of a day job and the pressures of commercial music.

Evidence supports the idea that this liberation leads to more, and more adventurous, creative work.

In short, basic income separates the idea that people have value from the idea that they must own something valuable.

All of that has been true for quite some time, and in fact arguments for basic income are as old as Thomas Paine. But there is a huge, disruptive change happening that makes this a much more urgent question, not just for musicians but for everyone. Namely, robots. Robots and computer automation are about to eliminate huge numbers of jobs (think tens of millions). Some are in the news right now: Uber is testing self-driving cars in Pittsburgh. Driverless trucking is not far behind, taking 3.5 million jobs with it. And it’s not just truckers: designers, fast food workers, accountants, financial analysts, doctors, hotel concierges. Thousands of news stories are being written by robots. An Oxford University study estimates that 47% of total employment may be at risk. Even jazz musicians have to be worried.

In short, the day job could be going away, and not just for musicians. The question is, what will we do with these millions of people, once they’re out of work? Will we insist that truckers can all get jobs doing social media? Will a few wealthy people retreat behind high walls and leave the rest of us to fight for the scraps of employment through a fog of financial worry and expensive, short term trade-offs?

Or will we embrace basic income, recognize that people have innate value, and unleash a wild torrent of creative exploration the likes of which we’ve never heard before? For the Silo, Anthony Moser.www.anthonymoser.com

@mosermusic

PS – My music is available on iTunes, Spotify, YouTube, Bandcamp, and a host of other digital music services. If you catch me at a gig, you can buy an album for name-your-price. And if anyone ever uploads it to The Pirate Bay, torrent with my blessing. As Woody Guthrie would say, “Publish it. Write it. Sing it. Swing to it. Yodel it. We wrote it, that’s all we wanted to do.”

New customers are essential to long-term business growth. The more customers you attract, the easier it will be for your company to grow. But how to attract new customers every day? Here are some ideas for gaining new customers.

Understand your customers

To gain new clients, you must first understand who your ideal customers are. This allows you to target and nurture them into making a purchase. So, before you do anything else, make sure you have accurate information about the customers you want to reach. Creating a buyer persona is a great way to improve your targeting.

Find the best channels for attracting new customers

When you know your customers, it’s easier to find them in the places they frequent the most. This could be done on social media platforms such as Facebook, Twitter, or Instagram. Or at your physical store. Analyzing your current customers to understand where they came from is the best way to know where you are likely to gain more customers.

Wall mounted prisma-print makes for a perfect outdoor display sign.

If you got them through mail or social media, you’re likely to get more if you target the same channel. However, if most of your customers discovered you with your physical store, you should focus on an outdoor display sign for example.

While it is acceptable to focus on one channel, especially if it is promising, a multichannel marketing strategy is recommended. Keep in mind that one channel can backfire.

Set objectives for attracting new customers

Setting goals motivates you to stay on track. Consider the following for the best experience when and after setting goals:

Make a list of everything you want to accomplish.

Analyze and prioritize your objectives.

Set a time limit to meet those objectives.

Begin with short-term objectives.

Recognize the purchasing procedure

How do customers contact you to make a purchase? If you know the answer to this question, it will be much easier to make the necessary changes to attract new customers. For example, if you discover that the majority of your customers are completing purchases on your site (which is not mobile-friendly), you can speed up the improvement process to attract more people.

Create compelling content

There is no other way to put it. Simply ensure that every piece of content you publish or share with your prospects establishes you as an expert in your field. This will encourage more people to interact with your content. You can even hire someone to create content for you if you find the DIY route too difficult.

Nothing can stop you from gaining new customers if you create content that your target audience is looking for and do it well. Remember that people enjoy reading and sharing rich content.

Having side cash from time to time, or even better continually, is a great source of wealth.

Not only that it enables you to collect money for something that you really need, but it really can boost your emergency fund, or just let you spoil yourself from time to time.

To get extra money and get it fast you can do several different jobs from ride-share services to doing some online surveys – they all pay differently, but they all will get you extra money.

Here are some of the best ways to earn money quickly this year.

Start With Home Care Services

You will be surprised to learn that additional help in-home care areas are always more than welcome.

With Boomers retiring and Millennials taking over the job market, it seems only logical for Millennials to provide additional care for senior citizens. Not only that you can find home care services jobs in Canada easily and fast, but next to quick money this type of job will also bring you a safe working environment, great companionship, and also provide you with a flexible work schedule, and an opportunity to learn new skills.

Sell Your Used Items

This is an old one, but a gold one.

Use well-known offline and online marketplaces, such as Craigslist, to sell items that no longer serve you.

You may not enjoy them anymore, but someone will be more than happy to welcome an original lamp from the 19th century or a preserved CD from ’90.

Do your best to present the product well:

Take great photos

Provide an accurate and brief description

Post items online

Pro tip: High-quality clothes and perfumes are the first to sell

Think also about selling old electronics, including tablets, fitness trackers, game consoles, and laptops.

The great thing about electronics is that if you cannot sell them, you can always trade them and get something that you can actually sell.

Freelance Online

Use large platforms for freelancers such as UpWork and Fiverr to get an online gig.

These sites are more than packed with different opportunities for people of various skills to land a job. Think about a position such as a virtual assistant, or a data entry assistant.

Good to know: It may take a while to get your first job, but in the long run this can be an ongoing source of additional money.

Can you guess how these gift cards tie in?

10 Ideas On How To Make Money Quickly

Sell unused gift cards

Be an affiliate marketer

Take online surveys

Tutor students

Delivery

Sell on eBay

Sell photos

Teach English online

Pet sitting

Dog Walking

There are dozens of different ways to earn money quickly and continually.

Before you start, be honest and know how much time you can invest in working on the side.

Once you determine that know what skills you can actually use to get that extra money. From there, find a place where your skills can be put to good use and sold.

In the meantime, check your loft and see what you have around collecting dust and sell.

MOGADISHU – The United Nations World Food Programme is delivering life-saving food and nutrition assistance to record numbers of people in Somalia, with over 4 million people a month receiving urgent humanitarian support to prevent famine in the face of the region’s worst drought in over 40 years.

The scale-up has helped keep the worst outcomes of Somalia’s hunger crisis at bay so far.