The intersection of logistics, data-driven retail, and social equity offers a unique opportunity for #ValueTransformation. By leveraging the existing infrastructure of modern commerce—specifically barcodes, dynamic pricing, and automated inventory management—we can pivot from bureaucratic stagnation to a lean, responsive governance model. This is not theoretical.

These systems already operate at scale, in real time, with measurable outcomes. The question is not whether the capability exists, but whether the will to repurpose it does.

The Geometry of Taxation: Moving Beyond “Flat”

In Tennessee, the conversation around fair taxation often stalls at the state’s reliance on sales tax. From a value-stream perspective, the current tax system is a “dumb” system; it applies a blunt force to every transaction regardless of the consumer’s economic position or purchasing context.

However, Tennessee already possesses the technology for Granular Fiscal Scaling. Retailers use advanced POS systems that can instantly differentiate between taxable and non-taxable goods, apply promotions, and even personalize pricing models. The infrastructure exists to move beyond a one-size-fits-all tax approach.

To achieve a system where “those with the most pay the most,” we do not necessarily need new forms, agencies, or bureaucratic layers. We need better algorithms at the Point of Sale—rules-based systems that can dynamically adjust tax burden based on product type, purchasing patterns, or other proxies for economic capacity.

In short, taxation can evolve from a static policy to an adaptive system.

Grocery Operations & the Barcode Revolution

Grocery stores are among the most operationally sophisticated environments in everyday life. They are masterpieces of inventory management, demand forecasting, and waste reduction. When a rotisserie chicken nears its “best-by” hour, a clerk applies a “Reduced” sticker. This is not just a discount—it is a real-time adjustment of value to prevent loss.

In Tennessee, grocery receipts already reveal the complexity of the tax code. Consumers routinely see different rates applied within a single transaction, such as a lower state rate on groceries versus higher combined rates on prepared foods or general merchandise. The system is already segmented; it is simply not optimized for equity.

The Proposed Policy Shift- The Bean Protocol:

To incentivize home-cooked nutrition and support economically constrained households, a deliberate tax gap can be introduced. Uncooked, shelf-stable staples like dried beans would carry a 0% sales tax, reinforcing low-cost, high-nutrition choices.

In contrast, prepared or convenience versions—“heat-and-eat” beans—would carry a significantly higher tax rate, such as 12%, reflecting their added convenience and positioning them as a discretionary purchase.

This is less about beans and more about behavioral economics. The tax code becomes a nudge engine.

The Store-within-a-Store (SwaS) Model: Every participating retailer would aggregate all “Reduced” or near-expiration items into a clearly defined, centralized zone. This “Value Zone” would be tax-free and highly visible. The goal is to create a frictionless experience for consumers who are maximizing every dollar, while simultaneously reducing food waste at scale.

This is lean thinking applied to hunger: eliminate waste, increase flow, and deliver value where it is most needed.

The Immigration & Infrastructure Myth The rhetoric surrounding “free benefits” for immigrants often overlooks the mechanical reality of how Tennessee collects revenue. Most taxation in the state is fundamentally location-based, not identity-based.

Sales Tax: The POS system does not check citizenship or residency status. It does not distinguish between a lifelong resident and a first-time visitor. If a purchase is made in Tennessee, tax is collected. Participation in the economy equals participation in funding the state.

Property Tax: Property taxes are tied to ownership and location. The obligation is attached to the asset, not the individual’s background or identity. By recognizing that economic participation drives tax contribution, the conversation can shift away from entitlement debates and toward optimization.

The more relevant question becomes: how do we best allocate and reinvest the value already being generated by everyone within the system?

Feeding the Foodless: The “Wimpy” Integration The gap between political promises and lived reality is often most visible in food insecurity. The challenge is not just supply, but access, dignity, and system design. The “Wimpy” philosophy—“I’ll gladly pay you Tuesday for a hamburger today”—can be modernized through digital infrastructure. For individuals who are food-insecure or temporarily without means, the self-checkout kiosk can become an access point rather than a barrier.

Identity-Linked Accounts: Using a state-issued ID or secure digital wallet, individuals in immediate need can scan essential items, particularly within the SwaS Value Zone. The “Tuesday” Account: Instead of declining the transaction, the system logs it to a state-managed account. Repayment can occur later through direct payment, payroll deduction, community service credits, or other structured mechanisms. The emphasis is on continuity of access, not denial. Risk Management: What retailers currently classify as “shrinkage” (loss through theft or spoilage) can be reframed as a measurable, trackable social investment. With proper data, the state can quantify outcomes, adjust thresholds, and continuously improve the model. This approach treats people not as liabilities, but as participants in a system designed to stabilize and eventually strengthen their position.

Conclusion: The Green For Governor Vision

The Jerri Green campaign and soon-to-be administration challenge citizens to stop treating governance like a paper-ledger business in a fiber-optic world. The tools of transformation already exist in grocery aisles, retail systems, and supply chains across Tennessee. By adopting #ValueTransformation, the state can convert everyday commercial infrastructure into a distributed network for social equity. Every barcode becomes a data point. Every transaction becomes an opportunity to align economic efficiency with human need. The result is a system where “Common Sense, Compassion, and Courage” are not just campaign language, but embedded logic—executed in real time, at the point where policy meets daily life.

The Fiscal Update the Government Should Have Produced and the Budget Canada Needs

by William B.P. Robson, Don Drummond and Alexandre Laurin

Introduction: No Budget, No Plan

The federal government has said it will not release a budget until the fall. Delaying a budget until the fiscal year is more than half over is never good, but Canada’s current high spending trajectory makes this delay especially bad. The government is making costly commitments without showing us the key numbers: how much more tax it expects to collect; how far its new spending will exceed its revenues; and what the resulting higher deficits imply for interest costs and our debt burden.

To fill in at least some of the information the government should be providing, we present our own fiscal update: the outlook that provides a context for the next federal budget. We then discuss possible measures the next budget could contain to address runaway spending, perpetually high deficits and debt, and vulnerabilities Canada should avoid at a time of severe economic challenge.

A Deteriorating Fiscal Outlook

To calculate the federal government’s bottom line in the current fiscal year, 2025/26, and the three following years, we followed the steps summarized in Table 1 (on page 3):

We started with the Liberal Party’s costing document for its election platform (Liberal Party of Canada 2025). Based on a March 2025 economic scenario from the Parliamentary Budget Office (PBO), it did not reflect the impact of US tariffs or Canada’s countermeasures (PBO 2025).

We updated the economic assumptions based on the Bank of Canada’s April 2025 Monetary Policy Report, using the more optimistic of the two scenarios examined by the Bank, both regarding the severity of tariffs and resulting economic damage (Bank of Canada 2025).

We calculated a revised baseline fiscal projection by including policy initiatives that appear firm – either because of definitive statements, such as the cancellation of the proposed changes to capital gains taxation and the June 2025 plans to first accelerate defence spending to 2 percent of GDP and then gradually increase it to 5 percent by 2035, or because legislation is currently before Parliament, as is the case for cuts to the bottom personal income tax rate, the GST break for first-time homebuyers under Bill C-4,1 and the government’s announcement that it will not proceed with the digital services tax (DST).

We added the spending measures from the Liberal platform’s costing document that were not included in the previous step.

We added platform proposals for increasing revenue from higher fines and penalties and, more significantly, for reducing spending through a review of public sector operations to boost productivity. We show these as a memo item, since the lack of concern about the bottom line evident in the platform and subsequent announcements, and the lack of urgency evident in the government’s decision to delay the budget, makes it reasonable to doubt that these savings will materialize.

The resulting bottom line represents a marked deterioration, as Table 1 shows. As recently as the April 2024 budget, the government projected the deficit to decline to $20 billion by 2028/29.2 With this baseline, and even if the imagined fines and savings were realized in full, the deficit that year would be more than three times that level. Even in this optimistic scenario, the deficit would average $78 billion annually over the four years, and the net debt-to-GDP ratio would remain stable around the elevated level of 2025/26. Excluding the speculative savings, the cumulative deficit would be almost $350 billion over four years – or an annual average of $86 billion – and the net debt-to-GDP ratio would increase to 44 percent. Further, the baseline deficit without any of the non-implemented initiatives in the electoral platform is still elevated at $66 billion per year on average.

These projections include our estimates of the potential impact of the new defence spending commitments made at the recent NATO summit. At that summit in The Hague, Canada joined a pledge to raise defence and security-related spending to 5 percent of GDP by 2035 (3.5 percent for direct military needs and 1.5 percent for security-related investments).

No details on the year-to-year increases have been announced, but countries are expected to submit multi-year roadmaps by mid-2026. Prime Minister Mark Carney also indicated that some of the 1.5 percent for security-related investments – such as critical mineral infrastructure, ports, telecommunications, and cyber – could be counted from existing budget envelopes.

In Table 2, we present a hypothetical scenario where annual defence spending rises gradually from 2 percent of GDP to 5 percent of GDP over 10 years, with half of the spending allocated to depreciable capital assets. Under this scenario, we estimate the increase would add $2.3 billion to the deficit this fiscal year, rising to $11.8 billion in four years. Assuming half of the new spending on security-related investments comes from existing envelopes, the deficit would be $17.8 billion higher in four years. These amounts continue to grow over the 10-year period as the 5 percent target approaches and the stock of amortized capital outlays increases. By year 10, new defence commitments could add a staggering $68.4 billion to the deficit under this scenario.

Separating Operating and Capital Spending is Unhelpful

The large deficits projected in this update cannot be downplayed or disguised by dividing the budget into two new categories – operating and capital – and targeting a balanced operating budget only, as proposed in the election platform. No firm details have been released about what each category will include, but logically, the operating budget will consist of whatever does not fall under the new capital category.

The rationale for introducing a capital budget is unclear. Under Public Sector Accounting Standards, the federal government, like all Canadian governments, uses accrual accounting. So its capital costs are amortized over the useful life of the assets. As a result, the government’s Statement of Operations already shows costs related to capital investments: depreciation (about $7 billion per year) and interest on debt incurred when the outlays occur. As more capital assets are added – such as ports or defence equipment – amortization expenses will rise. But amortization reflects the current consumption of capital assets and should remain part of the bottom line. Excluding it would disconnect the federal budget presentation from the audited financial statements – a serious blow to transparency and accountability.

More troubling is the pledge to recharacterize as capital spending “new incentives that support the formation of private sector capital (e.g., patents, plants, and technology) or which meaningfully raise private sector productivity” (Liberal Party of Canada 2025). Governments like to call many categories of spending “investment.” Would the new classification mean the government would exclude subsidies for housing construction or incentives for first-time homebuyers from the bottom-line target? Would it reclassify other subsidies – for clean technology, artificial intelligence, or training programs, for example – as capital? What qualifies as capital under this framework appears open to subjective interpretation, undermining accountability. Without clear standards audited by independent sources, this approach is ripe for abuse.

And for what purpose? The government appears intent on showcasing how much it is doing for growth. But this does not require a new accounting convention. Their efforts could be highlighted through words and dedicated tables – not by altering the definition of the bottom line.

What Canada Needs in the Next Federal Budget

Notwithstanding rhetoric about transforming Canada’s economy in the face of US trade threats and prioritizing growth, federal fiscal policy and promises do not support the transformation of Canada’s trade relations or promote investment over consumption. Adding $300 billion in federal debt while doing nothing to raise investment and productivity will make Canada more vulnerable, not less. The new 5-percent defence commitment, even if its fiscal impact will be felt mostly in the later years, further highlights the need for difficult tax and spending trade-offs. Given the scale of the new defence commitment, on top of the fiscal challenges created by the old one, it is all the more important for the government to ensure proper accountability.

For that reason, the next federal budget – which should come as soon as possible – should have the following features:

Dropping more costly platform initiatives. Recent developments, including diminished US support for environmental action and related impacts on Canada, suggest that some potential spending items may cost less or be delayed. Still, it seems surreal to contemplate introducing another $28.3 billion in deficit-increasing platform measures this fiscal year, when the projected deficit would already be close to $60 billion. One of the more straightforward options for the government in the 2025 budget is to forgo implementing some of its platform commitments or fund them through existing envelopes. The list is extensive. For example, the platform proposes to allocate over $10 billion to various infrastructure transfer funds, including nation-building initiatives, trade corridors, digital infrastructure, rural transit, critical healthcare, and community development. In addition, more than 64 small-scale platform measures, each costing under $200 million, collectively amount to over $3.1 billion. These areas clearly present opportunities for reallocation or funding within existing envelopes.

Finding deeper savings from existing operating spending. The C.D. Howe Institute’s 2025 Shadow Budget contemplates $97 billion in non-defence direct program expense savings over the budget horizon (Robson, Drummond, and Laurin 2025). Such savings are possible, but not achievable without strong leadership from the very top.

Rely more on less damaging taxes. Canada’s personal income tax rates are already high – the top rate is over 50 percent in most provinces – and our corporate income taxes are uncompetitive, undermining the investment we need to become more productive and raise workers’ wages. Those rates should come down: if the federal government is determined to fund spending that requires higher revenues, the least damaging option is to raise the GST rate, as proposed in the Institute’s Shadow Budget.

Cut federal transfers to provinces and territories. The Institute’s latest Shadow Budget also proposed cuts to transfers that fund programs that are not in the federal government’s jurisdiction (Robson, Drummond, and Laurin 2025). Provinces and territories would not welcome such a move – indeed, many might raise their own consumption taxes in response – but deficit-financed federal transfers are less consistent with fiscal sustainability and accountability than tax-financed ones, and the Canadian federation will be healthier if provinces and territories become more fiscally self-sufficient.

The Need for Clarity and Serious Choices

It is widely accepted that Canada’s economy is at a critical crossroads. So are Canada’s public finances. Beyond the economic drag of high deficits and rising debt, it is unfair to pass these burdens onto the current young and future generations.

The fact that the 2025/26 Main Estimates are before Parliament does not mean that the government has made itself accountable to the legislature for its fiscal plans.3 The Estimates support the appropriation bills through which Parliament authorizes funding for program spending not already provided for in existing legislation. They exclude any forward-looking policy initiatives typically included in a budget. They omit revenues and only account for a subset of expenses. They are prepared on a different basis of accounting than regular budgets and financial statements, making direct comparisons difficult. And they cover only a single fiscal year, making it impossible to assess the medium-term outlook.

The federal government itself should release full economic and fiscal projections to enable a proper national debate. But in their absence, this informal update will have to suffice.

Canada is on a troubling path. We need Parliament and the public to discuss the best way forward – economically and fiscally. The next federal budget should launch us on that path.

The authors extend gratitude to Colin Busby, Jamie Golombek, John Lester, Daniel Schwanen, and several anonymous referees for valuable comments and suggestions. The authors retain responsibility for any errors and the views expressed.

This article courtesy of our friends at www.cdhowe.org The Fiscal Update the Government Should Have Produced and the Budget Canada Needs for The Silo by William B.P. Robson, Don Drummond and Alexandre Laurin.

Presenters at last year’s C.D. Howe Institute’s conference on Canada’s debt problem had some pointed advice for our federal and provincial governments:

Canada’s public debt should be reduced about 10 percentage points of Canada’s GDP to ensure fiscal policy can be used to cushion the effects of future economic crises. Since major crises happen frequently, prudence suggests that the target should be achieved before the decade is out.

Tax increases harm economic performance, so elimination of public spending that does not provide enough benefits to offset this damage should be the first step in reducing deficits and debt. This will require undertaking comprehensive value-for-money assessments to identify wasteful spending.

Post-conference analysis found that achieving this prudent debt target would require increasing the combined federal-provincial primary balance by 1.4 percent of GDP, or $43 billion, starting in 2025/26. This amount includes a buffer – ensuring an 80 percent probability of meeting the debt target – to account for inevitable economic downturns, other crises that raise deficits and debt, and the uncertainty posed by fluctuating interest rates on financing costs.

The conference was one of four on deficits and debt held in Canada over the past 40 years. A clear and consistent message from these conferences – which politicians have yet to fully absorb – is that debt has economic costs and, therefore, imposes a burden on future generations. In this Commentary, the authors report on, and offer their analysis of, the findings of the latest conference.

Introduction

Does Canada have a debt problem? The answer from a recent C.D. Howe Institute conference is a resounding “yes.” Canada’s public debt should be about 10 percentage points of GDP lower to ensure sustainability. Given that major crises, which put upward pressure on deficits and debt, happen frequently, this target should be achieved before the decade is out.

The May 2024 conference was one of four on deficits and debt held in Canada over the past 40 years. Each aimed to provide guidance to policymakers on managing deficits and debt. While a common thread was concern about the economic cost of public debt, each conference provided context-specific policy advice.

The first conference, “Deficits: How Big and How Bad?” (Conklin and Courchene 1983), occurred when debt levels were rising rapidly but still relatively low. The key policy issue then was whether fiscal consolidation or expansion to support the economy was appropriate.

In the 1994 conference, “Deficit Reduction – What Pain, What Gain?” (Robson and Scarth 1994), and the 2002 conference, “Is the Debt War Over?” (Ragan and Watson 2004), there were clear recommendations to reduce debt levels. In 1994, this was motivated by concerns over economic damage caused by debt approaching 100 percent of GDP and questions about fiscal sustainability. By 2002, although the debt ratio had fallen substantially, further debt reduction was still advocated to reduce the burden on future generations who will not benefit from the spending.

A combination of discretionary measures and sustained economic growth led to a substantial reduction in the combined federal-provincial debt ratio from 2002 until the global financial crisis of 2007-2009. The debt ratio stabilized at a relatively high level after the crisis until the pandemic. The massive increase in debt during the pandemic and subsequent government spending raised the overall federal-provincial net debt ratio to about 75 percent of GDP, nearing levels from the time of the “Debt War” conference. This surge, combined with concerns about further increases, refocused attention on debt sustainability. This concern was reflected in the May conference, “Does Canada Have a Debt Problem?”, which recommended a debt target based on the need for fiscal prudence.

The latest conference included sessions on the economic costs of debt, the sustainability of federal debt, guidance for policymakers on a prudent and fair debt target, and reforming the federal fiscal framework. However, given the one-day format, not all issues could be thoroughly addressed. This report not only summarizes the proceedings but also fills some gaps by providing additional analysis to complement the presenters’ advice.

Economic Costs of Public Debt

Interest expenses were central to the analysis by University of Calgary economist Trevor Tombe of the economic costs of public debt. Interest paid on the public debt is often considered a transfer among individuals with no real impact on the economy. However, higher interest payments for a given level of program spending necessitate higher taxes, which harm economic performance by affecting incentives to work, save and invest. If not financed by tax increases, higher interest payments will crowd out valued program spending.

When discussing the opportunity cost of interest payments – the benefits of lower tax rates or higher program spending – Tombe cited work by Dahlby and Ferede (2022). They estimate the economic cost of raising an extra dollar of tax revenue, referred to as the “marginal cost of public funds” (MCPF). The MCPF includes both the dollar taken from the private sector and the loss in output per dollar of tax revenue raised due to reduced incentives to work, save and invest. Higher taxes shrink the tax base not only because of reduced economic activity but also due to efforts to reduce taxable income without changing economic behaviour.

Dahlby and Ferede (2022) find a very high cost from raising taxes. For the corporate income tax, the federal MCPF in 2021 was approximately two.1The MCPF from raising the top federal personal income tax rate has been higher than its corporate tax counterpart since 2012, when the corporate tax rate was reduced to 15 percent. The gap increased in 2016 when the top federal marginal personal income tax rate increased to 33 percent, pushing the MCPF to about 2.9.

The federal government expects to pay $54.1 billion in public debt charges in the current fiscal year. The economic cost of these payments is substantial. If the opportunity cost of these payments is lower corporate income taxes, their economic cost would also be about $54 billion. If their opportunity cost is a lower top personal income tax rate, their economic cost would exceed $100 billion. If the contribution from corporate income and top personal income tax were equal, the economic cost would be about $75 billion.

Other costs of public debt arise from a reduction in the national savings rate, which is the sum of public and private sector savings rates. Government deficits represent public sector dissaving, so with a constant private savings rate, national savings will decline when governments run deficits. Tombe highlighted the impact of lower national savings on investment, presenting data showing a negative correlation between debt ratios and investment ratios across countries (Figure 1). He stated there is “probably” a causal relationship between higher debt ratios and lower investment ratios.

Although Tombe did not elaborate, there are reasons to be circumspect about asserting causality. One reason is that the private savings rate may rise in response to budget deficits if economic agents anticipate higher future taxes to service the debt. Households might increase savings in anticipation, partially offsetting the decline in national savings. There is evidence that expansionary fiscal policy is partially offset by increased household savings. Johnson (2004) concluded that household savings would increase by 30-50 percent of the increase in government debt. In a recent study of fiscal expansions in the Euro area from 1999 to 2019, Checherita-Westphal and Stechert (2021) found that 19 percent of a fiscal stimulus is offset by higher household savings in the short-term, rising to 41 percent in the long-term.

Another reason for being cautious about inferring causality is that in an open economy, a decline in national savings does not necessarily lead to lower domestic investment, as any shortfall can be offset by borrowing from abroad. However, interest payments on borrowed funds and the return on foreign-owned capital reduce national income. An additional cost arises because the resulting current account deterioration must be offset by higher net exports, which requires a reduction in real wages in the export sector.

To complement Tombe’s analysis, we present an estimate of the economic cost of reduced national savings. In a closed economy with constant household savings, a budget deficit leads to a dollar-for-dollar crowding out of investment. Using historical returns on capital and assuming that national savings decline by 60 percent of the deficit due to offsetting increases in household savings, the $1,372 billion in federal net debt in the current fiscal year would have an economic cost of about $90 billion.2 This calculation does not capture the impact of lower capital intensity on productivity, so it underestimates the true cost.

If foreign savings offset the decline in national savings and foreigners invest directly in Canada, they receive the return on this capital, so the gross economic cost remains the same. However, the return is subject to corporate income tax, so the net economic cost would be about 25 percent lower. If Canadian firms borrow abroad to finance domestic investment, the economic cost is the interest paid to foreigners. While gross interest payments to foreigners will be less than the return on capital unless there is a large country-risk premium, interest payments are taxed more lightly.3 Therefore, the net economic cost may not differ substantially.

An additional cost of accessing foreign savings arises because higher capital servicing charges put downward pressure on the current account balance, which must be offset by an increase in net exports. In a small economy, export and import prices are determined in world markets, so the increase in net exports requires a decline in real wages in the export sector. However, if a country’s exports have unique features, increased supply can lower export prices, adding to the economic cost of borrowing from abroad (Burgess 1996).

Calculating the economic cost of investment crowding out when foreign borrowing is possible as the net-of-tax return on capital paid to foreigners establishes a minimum cost because it excludes the reductions in real wages required to increase net exports. The minimum cost would, therefore, be 0.75 x $90 billion = $68 billion, where the $90 billion reflects the economic cost of lower investment, adjusted by a factor of 0.75 to represent corporate income taxes on the returns paid to foreign investors. The $75 billion cost associated with raising taxes to finance higher federal interest expenses does not change with the availability of foreign financing, so the overall cost of the federal debt is approximately $142 billion, or 4.7 percent of GDP in 2024/25.

A similar calculation can be performed for overall provincial debt. In 2021/22, provincial net debt amounted to $784.7 billion, with debt service charges of $30.6 billion. Using the same weighted average economic cost of taxation as for the federal government, the economic cost of provincial debt service charges was $42 billion. The cost of investment crowding out adds another $39 billion, bringing the total cost of debt at the provincial level to $81 billion, or 3.2 percent of GDP in 2021/22. Assuming provincial debt remains at the same percentage of GDP from 2021/22 to 2024/25, the overall cost of Canada’s debt is about 8 percent of GDP.

Benefits of Debt and Its Optimal Level

Tombe also discussed the benefits of public debt, noting its role in financing long-lived assets, stabilizing the economy and smoothing tax rates over time. Governments should borrow to finance investments that will benefit future generations and should finance current expenditures out of current taxes. Spending on education, health and knowledge creation raises special concerns because it benefits both current and future generations. However, since each generation must make these investments, financing them through current revenues typically aligns with the benefit principle.

Counter-cyclical fiscal policy enhances social well-being by mitigating costly deviations from full employment. Additionally, governments can reduce the harmful effects of distortionary taxes by keeping them stable. Since the efficiency cost of taxes is higher when rates are above average than when rates are below average,4 governments should set tax rates at levels sufficient to support expected spending over the cycle and allow deficits to rise and fall in response to unexpected expenditures.5

An issue absent from discussions at the conference was the role of public debt in addressing market imperfections, which can improve efficiency. One such imperfection is the lack of adequate insurance markets against individual-specific wage income losses. As a result, individuals “self-insure” by increasing savings, which is more costly than paying the premiums in a well-functioning insurance market. Public debt puts upward pressure on interest rates and provides a safe savings instrument, allowing households to reduce their savings closer to the efficient level.

Unlike the efficiency gains from using public debt to stabilize the economy and smooth tax rates, mitigating the impact of inadequate insurance markets may justify a permanent increase in public debt. With a well-functioning insurance market, the optimal public debt ratio would be negative – governments should be net savers rather than net debtors. This would allow governments to finance expenditures from interest received on assets rather than from distortionary taxes.6

Empirical issues raised by the inadequate insurance-market approach include whether correcting the market failure is sufficient to make the optimal debt ratio positive and whether the penalty for deviating from the optimal ratio is significant enough to affect the choice of a debt target. Early analyses of incomplete markets found a positive optimal debt ratio. For instance, Aiyagari and McGrattan (1998) calculated an optimal debt ratio of 66 percent of GDP for the US economy. However, Peterman and Sager (2018), using a model with many of the same features as Aiyagari and McGrattan but incorporating multiple generations with standard life cycles instead of a single generation with an infinite life span, found that net government saving is optimal in the US economy. The main reason for the different result is that individuals in a life-cycle model spend a substantial fraction of their working lives accumulating enough savings to make self-insurance possible, so the benefit from self-insurance is smaller than if infinite life spans are assumed.

These results are less relevant for Canada for two reasons. First, employment insurance and other income support measures are more generous in Canada, so self-insurance leading to excess saving is less of an issue. Second, the US analysis assumes deficits are financed entirely by domestic savings, which is a much less realistic assumption for Canada. Foreign borrowing reduces the optimal debt ratio because it lessens the upward pressure on interest rates, which diminishes the impact of public debt on “self-insurance” savings and raises the cost of debt. James and Karam (2001) modified the Aiyagari and McGrattan model to allow borrowing from abroad, which changes the optimal debt ratio from 66 percent to about -80 percent. This qualitative result – that access to foreign savings reduces the optimal debt ratio – has been confirmed by other researchers (Nakajima and Takahashi 2017; Okamoto 2024; and Cozzi 2022).

This review suggests that the inadequate-markets approach does not reverse the conclusion from standard models that the optimal debt ratio is negative, implying that welfare gains can be realized when debt levels are reduced. However, the studies reviewed indicate that the penalty for deviating from the optimal debt ratio is small. In three of the six optimal debt studies reviewed, it is possible to compare the estimated economic costs. In the Peterman/Sager and Nakajima/Takahashi studies, a one-percentage-point increase in the debt ratio reduces consumption by .003 percent. The corresponding figure in the Cozzi study is much higher, approximately .02 percent. These estimates are very low relative to the estimates presented earlier, which imply a loss of .05 percent per percentage-point increase in the debt ratio.

It seems likely that these models are substantially understating the cost of debt. The benefits would have to be understated by an even larger percentage to overturn the conclusion that governments should be creditors not debtors. Since the argument for incurring debt to improve market efficiency is weak, the debt ratio should be chosen by considering only its impact on generational fairness. However, since debt is one of several factors affecting generational transfers, debt policy may have to deviate from the benefit principle to achieve a desired balance of the well-being of current and future generations.

Sustainability Analysis

High debt also raises concerns about its prudence or sustainability: can the interest expense be financed without requiring tax increases or cuts in program spending in the future? In his presentation, Alex Laurin, the Institute’s Vice President and Director of Research, challenged the federal budget’s claim that federal public finances are sustainable (Canada 2024, 382). The federal government’s sustainability claim is based on long-term projections showing a continuously declining debt-to-GDP ratio, reaching nine percent by 2055/56. Moreover, this trend holds even with less optimistic assumptions about interest rates and economic growth.

Laurin argued that this projection is not a convincing demonstration of sustainability for three reasons:

1) Interest Rate Assumptions: In the base case, the effective interest rate on federal debt (r) remains below the growth rate of the economy (g) for 32 years, which puts continuous downward pressure on the debt ratio. This assumption is inconsistent with the historical record. Over the past 35 and 45 years ending in 2022/23, averages of r-g are positive, at 0.8 and 0.4 percentage points, respectively. Only when the averaging period is extended back to include the high-inflation period starting in the 1970s does the multi-year average turn negative.7

2) Program Spending Assumptions: While revenues are assumed to grow in line with GDP, program spending decreases by about one percentage point of GDP over the projection period, causing the primary surplus to rise and putting downward pressure on the debt ratio. A more realistic “no policy change” assumption would keep the share of program spending roughly constant, allowing an assessment of the sustainability of current spending levels.

3) Exclusion of Economic Downturns: The projection fails to explicitly include economic downturns. Over the last 60 years, Canada has experienced five recessions, each prompting discretionary temporary stimulus measures that permanently increased debt. The policy response averaged 1.09 percentage points of potential GDP for each percentage point deviation from potential GDP (Table 1).

Laurin presented an alternative debt projection, assuming that overall program spending grows in line with GDP from 2029/30 to 2055/56 and that r equals g on average over the projection period.8 With these changes, the decline in the federal debt ratio is less pronounced, reaching 29 percent in 2055/56 compared to 9 percent in the budget projection.

Economic downturns were included in the projection by simulating 1,000 random probabilistic scenarios – assuming the frequency and magnitude of recessions over the past 60 years are representative of the future. Laurin assessed debt sustainability by calculating the probability that the debt ratio remains at or falls below its initial value over the projection period.9 The simulations showed an even chance that the debt ratio will exceed its 2028/29 value late in the projection period. Under the International Monetary Fund’s classification (IMF 2022), Canada’s federal debt would be considered unsustainable.

Some conference participants suggested that Laurin’s analysis might not fully capture the risks associated with the federal fiscal position because it assesses a single r-g profile. They also emphasized the importance of including provincial and territorial governments in any sustainability analysis, as these levels are most affected by demographic aging.

For this report, Laurin modified his approach to include provincial and territorial governments’ net debt and to capture the risks of r-g deviating from its assumed zero average over the long term. He introduced variability in the interest-rate growth-rate gap based on historical data, allowing for a more comprehensive risk assessment (methods and assumptions are provided in Appendix).

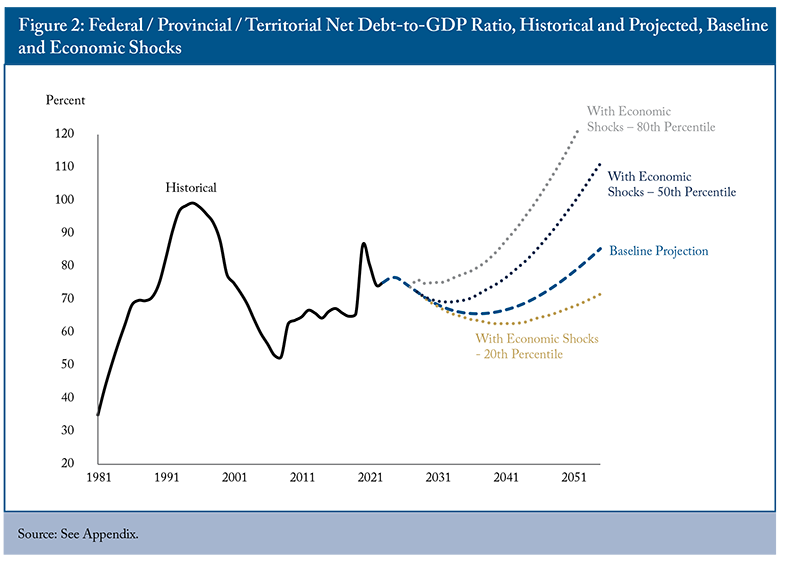

The modified analysis showed that, without any simulated shocks, the combined federal and provincial/territorial net debt-to-GDP ratio initially declines and then stabilizes until 2041/42, when rising healthcare costs due to demographic aging – and the associated interest on provincial debt – cause it to rise steadily (Figure 2, black dashed line). Introducing interest rate and recession shocks significantly alters the outlook, indicating a 50 percent chance that the debt ratio will begin its long-term rise in 2035/36, eventually surpassing 100 percent of GDP (black dotted line). There is a 20 percent chance (the 80th percentile) that the debt ratio will not decrease substantially from its current level and start a steady increase in 2033/34 (grey dotted line). Conversely, there is only a 20 percent chance (the 20th percentile) that the ratio will stay below its near-term value for the entire projection period (gold dotted line).

A Prudent and Fair Target

Prudence

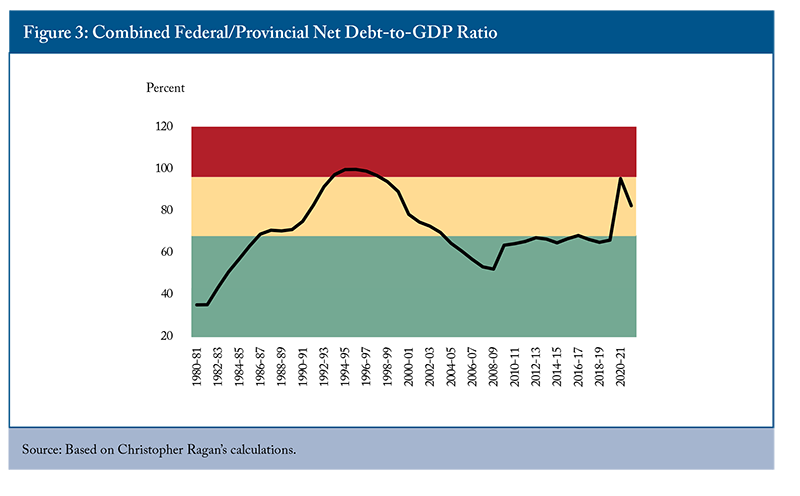

According to McGill economist Christopher Ragan, the main concern about Canada’s high public debt is that it will reduce our ability to borrow to address the next economic crisis. He analysed this issue using three zones for the debt ratio: red (top), yellow (middle) and green (bottom) (Figure 3). The red (top) zone, which represents unsustainable debt, starts roughly five percentage points below the 1995 federal-provincial debt ratio’s peak of 100 percent, when Canada entered a period of “forced austerity.” This entry point to the red (top) zone is higher than the 90 percent threshold for negative effects on growth developed by Reinhart and Rogoff (2010). However, the threshold would be lower if the interest rate on public debt (r) were higher than the rate of economic growth (g).

Ragan argued that the current combined federal-provincial debt-to-GDP ratio is in the yellow (middle) “cautionary” zone. The height of this zone is determined by the buffer required to avoid being pushed into the red (top) zone by an economic crisis. Entering the red (top) zone would mean sharply higher interest rates and lower growth.

To avoid this, Ragan set the buffer at 28 percentage points of GDP, about a quarter more than the increase in the debt ratio during the COVID-19 pandemic. Given the frequency of economic crises, he advocated returning to the green (bottom) zone by 2029/30, nine years after the end of the pandemic-induced recession. This requires reducing the federal-provincial debt ratio by about 10 percentage points.

Laurin followed up by determining the fiscal effort required to return to the green (bottom) zone with high probability. His calculations show that, starting in the next fiscal year (2025/26), the combined federal-provincial primary balance would need to increase permanently by 1.38 percent of GDP – or $42.9 billion in 2025/26.10 If implemented through spending reductions, provincial spending would have to decline by about 7 percent, or federal spending would have to fall by almost 9 percent. Note that such spending reductions would still not fully return the combined federal-provincial program spending/GDP ratio to its pre-pandemic 2018/19 value. The federal government could achieve the same effect by raising the GST to 8.5 percent. However, since most spending pressures from an aging population are on provincial governments, it would be sound policy for the federal government to transfer tax points to provincial governments (Kim and Dougherty 2020). Even with near-term fiscal adjustment, additional consolidation may be necessary in the future to prevent a rise in the debt/GDP ratio.

Ragan favoured achieving the debt target through expenditure restraint rather than raising taxes, which he thinks may have reached their limit. Restraining expenditures will be particularly challenging given medium-term pressures from an aging society, rising military and security needs, and potentially increased public investments for the transition to a green economy. Canada, therefore, needs an ongoing and thorough program review to identify low-priority spending.

Fairness

Financing current government spending with debt is generally considered fair if the debt-to-GDP ratio is constant or declining over time, implying that future generations can receive the same level of government services without facing higher tax rates. However, stable tax rates alone are insufficient to prevent intergenerational transfers. Taxes must increase to finance the interest on the debt or remain higher than they would be otherwise. If the tax increase applies to both current and future generations, tax rates would be stable but higher than they would be without the increased debt. The higher tax rates required to finance debt interest and the deficit-induced reduction in national-savings transfer part of the cost of government spending to future generations who do not benefit from the spending.

Assessing generational fairness requires understanding the extent of intergenerational transfers resulting from fiscal policy. The presentation by Parisa Mahboubi, a Senior Policy Analyst at the Institute, offered insights into this issue using generational accounts. These accounts show lifetime net taxes imposed by federal and provincial governments for each birth cohort from 1923 to 2023 and for a composite future generation consisting of all persons born after 2023. The lifetime tax burdens of the 2023 birth cohort and future generations are comparable because a complete life cycle is captured in both cases. Her analysis shows that future generations are expected to face a slightly higher lifetime net tax burden than the youngest living generation.

Preparing generational accounts requires information on lifetime taxes and transfers for each birth cohort alive today and for future generations. Projected values of taxes paid by current birth cohorts are developed based on age-specific profiles of different types of taxes,11 assuming unchanged tax policies. Spending on health, education, elderly benefits, child benefits, social assistance and GST credits vary by age, while other government expenditures are evenly distributed per capita. Per capita taxes, transfers and expenditures are assumed to grow at the same rate as productivity.

The lifetime net tax burdens for currently alive birth cohorts are calculated as the present value of projected tax payments less the present value of projected government transfers the cohort will receive. Lifetime net tax burdens of future generations are calculated using the “no free lunch” constraint: someone, sometime, must pay for all that the government spends (US Congressional Budget Office 1995). The lifetime net tax burden of future generations equals the amount of future spending not paid by currently alive generations.12

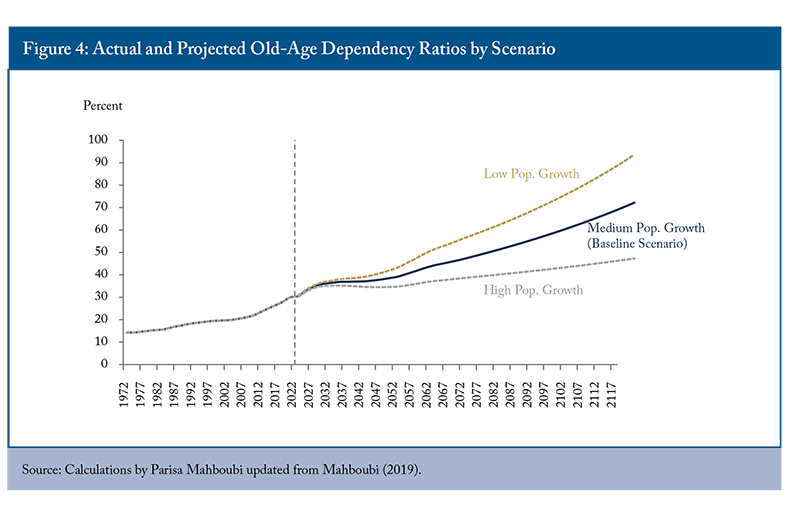

In the baseline scenario, productivity grows 0.94 percent annually, the average GDP per capita growth from 2002 to 2022. The discount rate is the average return on real return bonds over the same period, 1.3 percent.13 Statistics Canada’s medium-growth scenario14 is used for demographic projections, with population growing at an average annual rate of 0.85 percent over the 100-year projection, driven entirely by net immigration. The ratio of those over 65 to those aged 18-65 – the old-age dependency ratio – more than doubles over the projection period, rising from 30 percent to 72 percent (Figure 4).

The increase in the old-age dependency ratio drives upward trends in elderly benefits and health-related expenditures as a share of GDP. Other categories of age-specific spending remain roughly constant.

In the baseline scenario, the lifetime net tax burden of future generations (“unborn”) exceeds that of the cohort born in 2023 (“newborn”) by $23,000 per person (Figure 5). Factors influencing this result include:15

Fiscal Position in the Base Year: In 2023, federal and provincial tax revenues exceeded program spending by over one percent of GDP. A smaller primary surplus would have decreased the lifetime net tax burden of the newly born, increasing the burden on the unborn.

Population Growth: Faster population growth reduces the relative tax burden on future generations by slowing the rise in the old-age dependency ratio and reducing the per-capita burden of existing debt.

Healthcare Costs: If real healthcare costs increase faster than productivity growth, the recently born will pay a smaller share, leaving more for future generations.

The baseline assumptions represent the midpoint of a range of plausible values. While results are sensitive to changes in assumptions, the baseline is considered the most likely outcome. The generational accounts, therefore, suggest that fiscal policy is generationally fair.

However, other factors must be considered when assessing fairness:

Population Stability: If there were no net population growth, the tax burden on future generations would be much higher, even if the old-age dependency ratio did not change, because the cost of existing debt would be spread over a smaller population. This observation draws attention to the fact that future generations will be paying for services they did not receive, even with stable lifetime net taxes.

Income Growth: Future generations will likely be richer due to productivity growth, which could justify asking them to bear some costs of current consumption. However, parents may not wish to pass on costs to their children, even if incomes are rising over time. Population growth through immigration substantially reduces intergenerational linkages, which could encourage the current generation to increase the target size of intergenerational transfers.

New Spending Pressures: The generational accounts do not capture new pressures like rising military and security commitments or higher spending to achieve a net-zero emissions economy. In both cases, underspending in the past has pushed costs into the future. Pre-funding some of this spending by increasing taxes in the near term would even out contributions across generations.

Comparisons with Near Term Future Generations: Generational accounts compare a representative future generation with the most recent birth cohort. Comparing the tax burden of living generations with the burden on near-term future generations is also relevant.

While the generational accounts indicate that the federal-provincial fiscal stance is fair to future generations under current assumptions, it is beneficial to supplement this analysis with assessments over shorter time horizons. For example, virtually all living generations benefited from the debt-financed income stabilization and health measures implemented during the pandemic-induced recession. There is a strong fairness argument for paying down pandemic-related debt before the next generation starts working and paying taxes, which would occur over the 2035-to-2045 period (Lester 2021).

Federal and provincial Covid-related spending amounted to approximately $430 billion from 2020/21 to 2022/23.16 Federal and provincial debt was $2,092 million in 2022/23. Reducing the level of debt to $1,660 million no later than 2045/46 would be fair to generations born in 2019 and later. However, in Laurin’s prudent scenario, in which debt is sustainable with 80 percent probability, the level of debt rises continuously over the projection period. The gap between the prudent and fair level of debt is $1,200 million in 2035/36. Achieving a fair level of debt would require more fiscal consolidation than is needed to achieve sustainability.

Reforming Expenditure Management

Ragan’s debt target and the recommendation to achieve it through expenditure restraint raise two issues:

1) Building Consensus: How to build a consensus on the proposed debt target and increase the likelihood of achieving it.

2) Identifying Savings: How to identify programs that don’t provide enough value to justify raising taxes to finance them.

Economist and C.D. Howe Institute Fellow-in-Residence John Lester emphasized that achieving a political consensus on a more prudent fiscal approach requires vigorous and sustained advocacy. Part of this advocacy involves convincing governments to surrender some policy flexibility to increase the odds of achieving the target reduction in debt and reduce the risk of relapse after the next crisis.

Lester and Laurin (2023) propose a principles-based fiscal governance framework intended to reduce the bias toward deficit financing in both good times and bad. Governments should adopt guiding principles for fiscal policy, set operational rules for achieving target outcomes and transparently assess consistency with these principles.

At the conference, Lester expanded upon one element of the governance framework: a binding multi-year ceiling on non-cyclical spending. A key motivation for this proposal is the failure to adhere to spending tracks set out in budgets and fiscal updates. For example, in the federal government’s 2019 Economic and Fiscal Update, program spending was projected to decline as a share of GDP, reaching 13.8 percent by 2024/25. The spending ratio projected for 2024/25 increased in successive budgets so that in 2024-25 it will be almost 2 percentage points higher than projected in 2019.18

Binding multi-year expenditure ceilings apply in 11 OECD member countries (Moretti, Keller, and Majercak 2023).19 In the Netherlands and Switzerland, the ceilings are set out in legislation that constrains expenditure growth. Alberta has recently adopted a similar approach.20 However, in most countries, expenditure ceilings are set by the government to ensure consistency with its self-defined fiscal objectives, which may or may not include expenditure restraint. This is the general approach recommended for Canada, although the hope is that the self-defined objective will be to achieve the debt target through expenditure restraint.

The expenditure ceiling would be binding for five years, ideally developed in the first year of a new electoral mandate after a campaign outlining spending plans in detail. The ceiling would cover all categories of spending directly affected by policy decisions. It would be updated annually to account for forecasting errors in program determinants (e.g., inflation, population growth). There would be escape clauses for major economic recessions, natural disasters and war. The ceiling could include a reserve for new policy initiatives, but in the context of expenditure restraint new initiatives may need to be funded by eliminating or modifying existing programs.

Identifying the programs that should be scaled back or eliminated because they don’t provide enough benefits to justify raising taxes to finance them requires, according to Lester, an overhaul of the way the government manages its spending, particularly the performance management framework that is key to establishing value for money. Yves Giroux set the stage for this discussion by describing the federal government’s current expenditure management system.

The requirement to evaluate programs was formalized following the creation of the Office of the Comptroller General in 1978. Despite several modifications, program evaluations have not been successful in affecting strategic spending decisions. The Ministerial Task Force on Program Review (the Nielsen Task Force) from 1984 to 1986 described evaluations as “generally useless and inadequate for the work of program review” (quoted in Grady and Phidd 1993). More recently, McDavid et al. (2018, 302) conclude that evaluations do not “address questions that would be asked as cabinet decision-makers choose among programs and policies.”

Under the current evaluation policy, federal government departments have considerable flexibility in conducting evaluations. They may focus on design and delivery, program beneficiary responses or a comparison of program costs and benefits. A review of 48 evaluations prepared since 2020 in eight departments21 found that only four went beyond assessing operational efficiency and impacts on beneficiaries to examine whether the program represented value for taxpayer money. Three of these applied formal benefit-cost analysis, which is the standard for assessing regulatory proposals.22

Evaluating programs in terms of operational efficiency and beneficiary impacts helps improve programs, but if evaluations are to inform strategic spending decisions, value-for-money assessments must be mandatory. These assessments should be based on the benefit-cost framework applied to regulatory proposals.

Benefit-cost analysis of regulatory proposals – and by extension, spending programs – assesses the overall social benefits and costs of policy initiatives. The quantitative analysis attempts to determine if the economic pie is larger or smaller after government intervention. For example, economic development programs (business subsidies) are implemented with the expectation that they will increase overall real income. To assess this, benefit-cost analysis considers not only the additional investment and employment resulting from the subsidy but also the opportunity cost of workers and capital – the amount that would have been earned otherwise. The net increase in the economic pie is the incremental earnings of workers and capital less efficiency losses from raising taxes or issuing debt to finance the subsidy and resources used to administer and apply for it.

The nature of the assessment should vary by program type. Business subsidies, labour market development programs and climate change mitigation/adaptation measures have benefits and costs measurable in monetary terms. These programs could be ranked by their net social benefits, allowing comparisons within and across program categories. Programs where benefits are less than costs would be candidates for elimination or modification.

A more nuanced approach is needed when assessing social programs and other measures with a fairness goal for several reasons. Their economic impact is ambiguous, and a negative economic impact is not a sufficient reason to eliminate a program. In addition, support for an income redistribution program depends on who benefits from it. As a result, evaluations of social programs should be more descriptive than prescriptive. They should present information on the economic impacts of measures, their fiscal cost, including administration expenses, and a discussion of who benefits from the program and how they benefit. Evaluations should also assess how the program fits into other measures providing support to the target population. This information will allow elected officials and, since all evaluations would be made public, Canadians, generally, to form an evidence-based opinion on the value for money of social programs.

A thorough assessment of government programs through a value-for-money lens may not identify enough wasteful spending to achieve deficit and debt targets. If so, tax increases should be used to achieve the objectives.

Adopting and achieving the debt target will require a political commitment that currently does not exist. The task for policy analysts is to help build a consensus on a more prudent approach to fiscal policy and a revamped expenditure management system. According to Lester, this consensus should be ratified by legislation setting out general principles for sound fiscal policy, supplemented with non-legislated operational rules to guide annual policy and monitor progress. This approach would impose discipline on fiscal policy while allowing flexibility to address unexpected developments. Legislation would strengthen the consensus on fiscal prudence and help prevent backsliding by future politicians.

Conclusion

The evidence presented at the conference confirmed that Canada has a debt problem. Existing debt levels are not prudent, and they raise concerns about generational fairness. Prudence requires that Canada’s public debt be reduced by about 10 percentage points of GDP before the decade’s end. This would require increasing the combined federal-provincial primary balance by 1.4 percent of GDP, or $43 billion, starting in 2025/26.

Tax increases harm economic performance, so elimination of public spending that does not provide enough benefits to offset this damage should be the first step in reducing deficits and debt. Identifying wasteful spending will require comprehensive value-for-money assessments. Governments must not take the easy way out by implementing across-the-board spending cuts. Successful expenditure restraint will also require setting binding multi-year expenditure ceilings to prevent governments from spending revenue windfalls or from increasing spending to improve chances of electoral success.

Canada’s public debt is imposing a burden on future generations. A comparison of the lifetime tax burden on the recently born with distant future generations reveals only a small generational transfer in favour of the recently born. However, burden shifting is much larger from currently living generations to persons born shortly after the pandemic-induced recession. The $430 billion in pandemic-related debt should be paid down by the people that benefited from the income stabilization measures. Achieving this fairness objective would require more fiscal consolidation than needed to ensure sustainability of the debt. For the Silo, Alexandre Laurin/John Lester via C.D. Howe Institute.

Appendix: Assumptions and Methods for the Sustainability Analysis

References

Aiyagari, S. Rao, and Ellen R. McGrattan. 1998. “The Optimum Quantity of Debt.” Journal of Monetary Economics 42 (3): 447–69.

Ambler, Steve, and Craig Alexander. 2015. “One Percent? For Real? Insights from Modern Growth Theory about Future Investment Returns.” E-Brief. Toronto: C.D. Howe Institute. October.

Burgess, David F. 1996. “Fiscal Deficits and Intergenerational Welfare in Almost Small Open Economies.” Canadian Journal of Economics, 885–909.

Canada. 2024. “Budget 2024.” Department of Finance Canada. April.

Checherita-Westphal, Cristina D., and Marcel Stechert. 2021. “Household Saving and Fiscal Policy: Evidence for the Euro Area from a Thick Modelling Perspective.” Available at: https://papers.ssrn.com/sol3/papers.cfm?abstract_id=3992188.

Conklin, David, and Thomas Courchene. 1983. “Deficits: How Big and How Bad?” Special Research Report. Toronto: Ontario Economic Council.

Grady, Patrick, and Richard W. Phidd. 1993. “Budget Envelopes, Policy Making and Accountability.” Government and Competitiveness Project, School of Policy Studies, Queen’s University. http://global-economics.ca/budgetenvelopes.pdf.

International Monetary Fund (IMF). 2022. “Staff Guidance Note on the Sovereign Risk and Debt Sustainability Framework for Market Access Countries.” 2022–039. IMF Policy Papers.

James, Steven, and Philippe Karam. 2001. “The Role of Government Debt in a World of Incomplete Financial Markets.” Department of Finance, Economic and Fiscal Policy Branch.

Jenkins, Glenn, and Chun-Yan Kuo. 2007. “The Economic Opportunity Cost of Capital for Canada-an Empirical Update.” Queen’s Economics Department Working Paper. Available at: https://www.econstor.eu/handle/10419/189409.

Kim, Junghum, and Sean Dougherty (eds.) 2020. “Adaptability, accountability and sustainability: Intergovernmental fiscal arrangements in Canada,” in Ageing and Fiscal Challenges across Levels of Government, OECD Publishing, Paris.

Mahboubi, Parisa. 2019. Intergenerational Fairness: Will Our Kids Live Better than We Do? Commentary 529. Toronto: C.D. Howe Institute. January.

McDavid, Jim, Astrid Brousselle, Robert P. Shepherd, and David Zussman. 2018. “Linking Evaluation and Spending Reviews: Challenges and Prospects.” Canadian Journal of Program Evaluation 32 (3): 297–304. https://doi.org/10.3138/cjpe.43176.

Modigliani, Franco. 1983. “Government Deficits, Inflation and Future Generations.” In Deficits: How Big and How Bad, pp. 55–71.

Nakajima, Tomoyuki, and Shuhei Takahashi. 2017. “The Optimum Quantity of Debt for Japan.” Journal of the Japanese and International Economies 46:17–26.

Okamoto, Akira. 2024. “The Optimum Quantity of Debt for an Aging Japan: Welfare and Demographic Dynamics.” The Japanese Economic Review. May. Available at: https://doi.org/10.1007/s42973-024-00156-7.

Panizza, Ugo, Richard Varghese, and Yi Huang. 2019. “Public debt and private investment.” Centre for Economic Policy Research. VOXEU Column. December 4.

Reinhart, Carmen M., and Kenneth S. Rogoff. 2010. “Growth in a Time of Debt.” American Economic Review 100 (2): 573–78. https://doi.org/10.1257/aer.100.2.573.

Robson, William, and Parisa Mahboubi. 2024. Another Day Older and Deeper in Debt: The Fiscal Implications of Demographic Change for Ottawa and the Provinces. Commentary 665. Toronto: C.D. Howe Institute. August.

Robson, William, and William Scarth. 1994. Deficit Reduction – What Pain, What Gain? (Policy Study 23). Toronto: C.D. Howe Institute.

January , 2025 – One of the most consequential policy changes in this year’s federal budget – an increase in the capital gains inclusion rate – would have far-reaching consequences for Canadians, many of which are underestimated by the government, according to a new study from the C.D. Howe Institute. Leading economist and former President and CEO of the C.D. Howe Institute, Jack Mintz, examines the extensive economic repercussions of this proposed change in his latest report available in full at the end of this article.

Fiscal and Tax Policy

With Parliament prorogued on January 6, the future of the proposed capital gains tax increase remains uncertain. Canadians face the possibility of the measure being passed, amended, or withdrawn entirely under a new government.

Meanwhile, tax planners and the affected individuals and corporations must await the outcome, even though the Canada Revenue Agency began administering the tax on June 25, 2024, after it was announced in the spring budget. At this time, taxpayers could be assessed interest and penalties if they do not comply with the proposed law. If the law is never passed, taxpayers will have to claim refunds. The provincial budgets reliant on the new revenues will be affected if the planned measure is ultimately withdrawn, adding to the confusion and disruption.

“The planned measure to increase the capital gains inclusion rate should never see the light of day when Parliament resumes after March 24, nor be revived thereafter by a new government,” says Mintz. “The hike would create a triple threat: harming Canadian businesses, discouraging investment, and penalizing middle-income Canadians.”

While the government estimated this change would only impact 40,000 individual tax filers and 307,000 corporations, Mintz’s analysis, using longitudinal data, reveals the true impact would be significantly broader. Over 1.26 million Canadians would be affected over their lifetimes – representing 4.3 percent of taxpayers or some 22,000 Canadians per year – with many middle-income earners among those hardest hit.

The report projects significant economic harm caused by the proposed increase – Canada’s capital stock would decline by $127 billion, GDP would fall by nearly $90 billion, and real per-capita GDP would drop by 3 percent. Further, employment would decline by 414,000 jobs, which would raise unemployment from 1.5 million to 1.9 million workers. Importantly, half of the affected individuals would be earning otherwise less than $117,000 annually, with 10 percent earning as little as $18,000, excluding capital gains income.

“This would not just be a tax on the wealthy,” says Mintz. “Many middle-income Canadians would bear the brunt of this increase, and the economic costs would ripple across the entire economy.”

Mintz also highlights the broader implications for Canadian businesses. The planned measure would likely deter equity financing, discourage investment, and exacerbate inefficiencies in financial and corporate structures. Contrary to government claims of “neutrality,” he argues the tax would disproportionately harm domestic companies. These companies will pay corporate capital gains taxes that will increase investment costs. Moreover, they are dependent on Canadian investors due to “home bias” in equity markets. The changes would risk weakening Canada’s productivity and competitiveness at a critical time.

The report further critiques the lack of mechanisms to mitigate the effects of “lumpy” capital gains. Significant asset disposals, such as selling real estate, farmland, business assets, secondary homes or during events like death or emigration, may occur only once or twice in a person’s lifetime. Without provisions to average or defer taxes, individuals would face disproportionately higher burdens. Additionally, the planned tax hike would exacerbate the “lock-in effect,” which discourages the efficient reallocation of capital.

“If the proposed law does not proceed, it would be worthwhile for a government to review capital gains taxation as part of a general tax review that would improve opportunities for economic growth rather than hurt it,” says Mintz.

On August 30, the US requested consultations respecting Canada’s Digital Services Tax Act under the dispute settlement procedure set out in the Canada-US-Mexico Agreement (CUSMA). The US maintains that by imposing the tax, Canada has failed to provide US service providers and investors treatment no less favourable than it provides to Canadian service providers and investors. Given Canada’s unique trade relationship with the US, this could have major implications.

The essence of the complaint is that Canada is violating a specific CUSMA obligation to grant US firms terms that are no less favourable than its own companies receive.

This is called national treatment. The crux of the US argument is that the revenue and earnings thresholds are so high that no Canadian service provider would be subject to the tax, but at least some US providers would be. While the DST is not discriminatory on its face, its practical effect is discriminatory.

Canada’s taxation of digital services has been an on-going contentious issue with the US. The new legislation entered into effect on June 20 and imposes a 3-percent levy – retroactive to January 1, 2022 – on revenue (not income) earned from digital services when certain thresholds are met. Annual gross revenues in a calendar year must exceed €750 million for the tax to apply. The taxpayer must also earn at least C$20 million in Canadian digital services revenue in a calendar year. Affected companies are to start paying the tax next June 30.

On August 1, the Congressional Research Office released a paper outlining multiple concerns. It cites industry associations that maintain that Canada’s DST could “cost US exporters and the US tax base up to $2.3 billion annually and could directly result in the loss of thousands of full-time US jobs.” The paper also cites possible violations of CUSMA and WTO obligations.

The paper also notes that the United States Trade Representative (USTR) has applied sanctions under Section 301 of the 1974 Trade Act against digital services taxes enacted by other countries. Section 301 is much broader in its application than either CUSMA or the WTO.

The CUSMA panel could decide for the US if the facts establish that only US companies meet the €750 million threshold for overall earnings and whose Canadian digital earnings exceed C$20,000,000.

Aside from the possibility of an adverse panel decision and action by the US under Section 301, there are other factors that Global Affairs Canada should consider before the Canadian government commences with the retroactive portion of the tax.

CUSMA is up for renegotiation on July 1, 2026. The process on the US side starts with a USTR report to Congress, due by the end of 2025, that will include an assessment of CUSMA’s operation, as well as a recommendation on CUSMA extension. As Canadian initiatives to impose digital taxes have been a US concern for years now, the recommendation will doubtless address the question of Canada’s DST regime. If that regime remains an open issue and US concerns are not satisfied, the stage could be set for the ultimate demise of CUSMA in 2036.

CUSMA Article 32.6 also provides that a party can withdraw from CUSMA upon giving six months’ notice to the other parties.

Decision time for the Canadian government falls on June 30, 2025, and it has to decide whether to go ahead and start collecting its retroactive DST and face the inevitable hostile reaction of its largest trading partner. This has to be carefully managed, or this small issue could become a big one. For the Silo, Jon Johnson.

Jon Johnson is a former advisor to the Canadian government during NAFTA negotiations and is a Senior Fellow at the C.D. Howe Institute.

Bookkeeping is tedious for most business owners unless you are a seasoned accountant or a fan of working with numbers. That is because businesses have a lot of financial details that need to be recorded, for instance, which supplier should be paid, outstanding customers, equipment to buy, significant purchases to make, and more. Without an accounting and bookkeeping system, you may lose essential business data, miss important goals, or make uninformed decisions that may affect your company’s finances.

Proper money-handling strategies are integral in any business as it helps you keep track of your long-term goals, improve your profits, and streamline seasonal cash flow changes. In addition, it will help your business stay out of trouble with the Internal Revenue Service or IRS.

By adopting good bookkeeping habits, you can avoid costly errors when it comes to record keeping. You can opt to have an in-house team to handle all your bookkeeping services, but this can be un-economical for small business owners. To save on cost, you can work with a bookkeeping agency, which often offers professional online and virtual services in Canada at very fair rates.

Here are seven tips for better bookkeeping for businesses in Canada.

Separate Your Business and Personal Finances

If you are a sole business owner, you should learn to separate your personal and business accounts. This will help you maintain records of every business and personal spending and help you keep the boundary to alleviate eating into the business growth finances.

For limited liability companies, the business is a separate entity from you, and your finances should be kept separate. That means you need to know which assets belong to the business and which are yours. By eliminating all personal transactions from the business accounts, you will lower the number of transactions the bookkeeper needs to categorize and reconcile. Additionally, your tax preparation and filing process will be seamless. You can find a bookkeeper in Canada to help you separate your accounts and provide outsourced business and personal bookkeeping services.

Control Your Business Credit

One of the common signs of an insolvent business is the inability to make payments promptly. The company may need better credit scores, lack of funding, or challenges in fulfilling its working capital needs.

When your business depends on bank financing to fund everyday operations, you will need help to pay back your high-interest debt. Therefore, you need to do due diligence before taking external funding.

You should set strict deadlines for your clients to pay what they owe and consider blocklisting repeat offenders that are taking advantage of you. Eliminate any late payments, as it is just like an interest-free loan. Your business may quickly become a cash-flow crisis if you lack rigorous credit control.

Track Business Expenses

Business expenses may be claimed against tax; therefore, tracking them is crucial if you want to cut overhead and maintain a healthy cash flow. You should always use a business credit card and keep records of expenses based on business activity.

Categorizing your expenses can be crucial, especially when your business is undergoing an CRA audit. The numbers on tax returns are often estimates, and these records help offer supporting evidence. Always remember that even trivial expenses will add up, and having records of everything can be helpful in the long run.

Overspending negatively affects any business; hence, keeping track of your expenses will ensure you track all your expenditures. Always remember that every dollar that you spend takes the business one step away from making a profit. Therefore, when running a business, keep a close watch on all your expenses, understand the benefit you gain from each expense, and document everything carefully. With outsourced online bookkeeping services, you can keep track of all your business expenses and maintain good records.

Schedule Routine Bookkeeping Times

As a business owner, you are handling many things at once, which can eat into the time you can use to monitor your financial record books.

The best way to keep your accounts is by consistently scheduling times to balance your books or working with a bookkeeping company in Canada. You can set aside time when your credit card statement is due and check through your monthly transactions to ensure everything is accurate. Although this task will take about one or two hours, it will simplify your life during the tax season by making tax preparation and filing much more effortless.

Create Budgets For Your Expenses And Set Financial Goals

Planning for business expenses, especially significant purchases, can help you best utilize your business resources and credit while giving you the peace of mind you need. Setting up and reviewing business budgets is directly related to the success of your business.