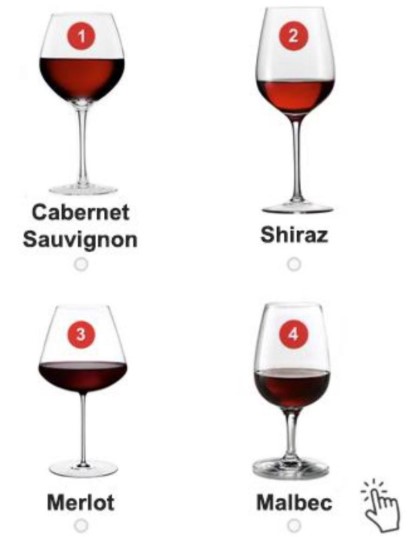

French scientists have discovered one of the following wines offers up to 10X more cancer-protective and cardio-protective effects than the rest…

Plus, this one wine also supports significantly improved metabolism when you drink it a certain way.

But which one? Is it…

(Click on the wine image you think is right.)

HINT – Researchers point to one wine above to explain the French Paradox. So, if you want to be lean AND still drink wine, it should definitely be THIS.

A whole generation of Americans (and Canadians!) grew up staring out of their high school class windows and imagining invading Soviet paratroopers landing outside. Many of them (a few decades older and wiser) are reliving the past through interesting throwback fashion choices and in extreme cases- full on cosplay.

If you have always wanted a Calumet High Varsity jacket or one of those cool Russian camo coats that the Wolverines eventually commandeer and rebelliously wear as their own- our friends at kommandostore.com have some good news for you.

But first here is a mini-review written waaaay back in 2002 that does a good job of explaining the believable paranoia vibe of Red Dawn.

“Someone else before me wrote that a lot of people don’t understand how believable this movie was in it’s day. I have to agree with the author. I remember this movie as being pretty scary and pretty violent. I haven’t seen it in a while but there’s a lot of scenes that haunt me. One in particular is when several of the kids look for their parents at a concentration camp. Harry Dean Stanton gives a powerful performance that serves to show that he’s a genuine actor. That scene is heartbreaking, as well as a scene that follows with Patrick Swayze breaking down in the snow covered woods. C. Thomas Howell vs. the helicopter. The ritual of the deer blood. Powers Boothe. The final battle and resolution. Yeah, it’s a little much and these days, it wouldn’t exactly fly but dammit Jim, I dug it at the time and I still do. I think everyone should see it, just so you can either remember or learn what it was like to live in a time when the general thinking was a little paranoid. I think the movie manages to capture at least that, being what it is, a paranoid fantasy of someone who probably has a huge gun collection in his concrete reinforced cellar.” Mr. Parker via imbd.com

The Bad Guy Look

The Good Guy Look. Well one of them anyway.

Now if only we could find that 1977 Chevy Cheyenne Cayenne step-side that Jed drove the hell out of escaping those pesky Russkies.

Fun Facts from the Movie via imdb

Five of the 36 paratroopers in the beginning of the film got blown as much as a mile off-course during filming. One got stuck in a tree, and had to convince locals that he wasn’t really an enemy soldier.

C. Thomas Howell had been a rodeo cowboy. He helped teach the rest of the cast to ride horses.

The plot, a Soviet and Cuban invasion from Mexico, was based on C.I.A. and War College studies of U.S. weaknesses at the time.

Patrick Swayze got frostbite during filming. A few years later, he said it still felt like someone shoving toothpicks up his fingernails when he got too cold.

The film contains no computer graphics effects, chroma key composites, or miniatures. All of the explosions are real, and actual size.

The film made the Guinness Book of Records for the most acts of violence in any film up to that time. According to their calculations, 135 acts of violence occur per hour, or 2.23 per minute.

The actors trained using real weapons so that they wouldn’t make mistakes using the prop ones. Lea Thompson recalled, “We went to a firing range and there was every kind of gun you could imagine.”

The cast underwent an intensive eight-week military training course before filming started.

Lea Thompson said that this is the best time she’s ever had on a movie.

Real Green Berets helped with the actors’ boot camp training.

William Smith didn’t receive any special language training for his role. Thanks to years of military service, and work with the C.I.A. and N.S.A., Smith was already fluent in Russian and several other languages.

Patrick Swayze stayed in character throughout filming. He said, “I became Jed Eckert.”

The story was originally to be set in the real town of Calumet, Michigan. It was moved to a fictionalized version of Calumet, Colorado. It was a more central location within the United States, which better fit the story. In real life, Calumet, Colorado is a tiny former mining town abandoned in the 1970s.

“Red Dawn” was the code name for the military operation that captured Saddam Hussein on December 13, 2003. Writer and director John Milius felt honored by that.

The original trailer, on the LaserDisc release, includes a scene in which a tank rolls up to a McDonald’s where enemy soldiers are eating. The scene did not appear in the final cut, and was likely removed due to a mass shooting at a McDonald’s in San Ysidro, California, a few weeks before the film opened.

This was the first film released with a MPAA PG-13 rating, on August 10, 1984. The Flamingo Kid (1984), the first film to get a PG-13 rating, sat on the shelves for five months before release.

Two C.I.A. agents came to the set, investigating reports of Russian tanks in the area. They were relieved to hear the tanks were for a movie.

A more involved love story between Jed and Toni was cut because Patrick Swayze didn’t feel it would work in the context of the film’s plot. Swayze and Jennifer Grey later appeared in Dirty Dancing (1987).

As it got colder, the actors and actresses had to adapt to freezing temperatures, often well below 0°F (-17.7°C).

This movie was initially banned in Finland due to excessive violence, disagreements with Finland’s foreign policy, and being “too anti-Soviet.” It was eventually released on video there.

While generative AI transforms how Americans shop, it’s also quietly powering a counterfeit crisis now spiraling out of control. A groundbreaking new report from Red Points and OnePoll, The Counterfeit Buyer Teardown, reveals that AI is no longer just helping consumers find the best deals—it’s helping them find fakes. From influencer-driven “dupe culture” to hyper-realistic fake storefronts, the study exposes a booming underground economy that’s been supercharged by technology. With 28% of counterfeit buyers now using AI tools to seek out knock-offs, and fraudulent social media ads spiking 179% in just one year, the findings deliver a wake-up call for brands, regulators, and shoppers alike. Red Points execs are available to break down the data, discuss solutions, and explain why this rapidly evolving trend is both a technological and ethical crisis for the digital marketplace. Interest here as we hope?

AI Supercharging U.S.and Other E-Commerce Counterfeit Crisis

An explosive new report, “The Counterfeit Buyer Teardown, ” paints a concerning picture of a rapidly evolving and increasingly sophisticated counterfeit goods market, driven by a new factor: Artificial Intelligence. Forget the back alleys; findings from the research—conducted by market research firm OnePoll and AI company Red Points in February 2025—highlight that the future of fakes is digital, AI-assisted, and alarmingly mainstream.

The convergence of technology, social media, and shifting consumer mindsets is reshaping e-commerce—and not always for the better. As AI accelerates both the spread and appeal of counterfeit goods, the challenge is no longer just spotting fakes—it’s confronting a counterfeit economy that’s growing smarter, faster, and harder to contain.

“As counterfeiters adopt advanced tools like AI, the fight against fakes is becoming more complex and more urgent,” said Laura Urquizu, CEO & President of Red Points. “We’re now seeing AI shape both the threat and the solution. In 2024 alone, our firm detected 4.3 million counterfeit infringements online—an alarming 15% increase year-over-year.”

Alarming indeed. Here are 5 key revelations from the study.

1. AI is the New Enabler of Counterfeiting – A Two-Sided Threat:

The Counterfeiters’ Edge: AI is dramatically lowering the barrier to entry for bad actors. They can now mimic brand listings, and impersonate social media accounts with unprecedented ease and speed. They can also effortlessly create professional-looking fake websites—a situation that, according to Red Points’ data, is projected to surge 70% in 2025.This isn’t just about cheap knock-offs anymore; it’s about sophisticated deception at scale.

The Consumers’ Assistant: Shockingly, 28% of online shoppers who bought fake goods used AI tools to find them. This isn’t a fringe behavior; it’s a growing trend, especially among Gen X, suggesting consumers are actively leveraging AI in their pursuit of cheaper alternatives. This fundamentally shifts the narrative – it’s not just about being tricked; some are actively seeking fakes with AI’s help.

2. Accidental Counterfeiting is a Major Problem – Trust Signals are Being Hijacked:

1 in 4 luxury counterfeit purchases are unintentional. This shatters the perception that buyers knowingly seek out high-end fakes. Realistic pricing, secure payment promises, and active (but fake) social media presence are successfully deceiving consumers. AI-generated legitimacy cues are becoming indistinguishable from the real deal.

Brands are Paying the Price for These Mistakes: A staggering one in three shoppers stop buying from the genuine brand after an accidental counterfeit experience. This highlights the significant damage to brand loyalty and future sales, even when the brand isn’t directly selling the fake. High-trust categories like luxury and toys are particularly vulnerable.

3. The “Dupe Economy” is Real and Influencer-Driven:

Nearly a third (31%) of intentional counterfeit buyers were swayed by influencer promotions. Social media is driving the demand for “dupes” – budget-friendly replicas. Authenticity is taking a backseat to price and perceived identical appearance, especially among younger demographics.

This isn’t just about saving money; it’s a shift in consumer mindset. The report suggests a growing acceptance of fakes as clever alternatives, fueled by social validation and influencer endorsements.

4. Marketplaces Remain Key, But Social Media and Fake Websites are Surging:

Marketplaces (both US and China-based) are still the primary channels for counterfeit purchases. However, fake websites (accounting for 34% of unintentional purchases) and social media are rapidly gaining ground as sophisticated avenues for distribution, amplified by AI’s ability to create convincing facades.

Social media ads redirecting to infringing websites saw a massive 179% year-over-year growth. This highlights the increasing sophistication of counterfeiters in leveraging advertising platforms to drive traffic to their fake storefronts.

5. Younger Generations are More Vulnerable in Key Categories:

Millennials are significantly more likely to have their personal data stolen after purchasing from fake websites (44% vs. 34% average). This suggests a higher susceptibility to sophisticated phishing scams disguised as legitimate e-commerce sites.

Gen Z and Millennials are 2-4 times more likely to accidentally purchase counterfeit luxury goods and toys compared to Baby Boomers. Their online savviness might be a double-edged sword, making them more exposed to deceptive listings.

This study serves as both a consumer alert and a brand wake-up call. The rise of AI as a tool for both counterfeiters and consumers is a seismic shift that demands urgent attention. With compelling data and a clear-eyed look at accidental purchases, influencer-driven “dupe culture,” and the growing sophistication of fake storefronts, the findings paint a stark warning for the future of online shopping.

“Counterfeiting poses a serious and evolving threat to innovative businesses and consumer safety,” notes Piotr Stryszowski, Senior Economist at the Organization for Economic Co-operation and Development (OECD). “Criminals constantly adapt, exploiting new technologies and shifting market trends—particularly in the online environment. To effectively counter this threat, policymakers need detailed, up-to-date information. This study makes an important contribution to our understanding of how counterfeiters operate and how consumers behave online.” Ultimately, The Counterfeit Buyer Teardown report underscores a new reality: counterfeiting is no longer confined to shady sellers or easily spotted scams—it’s embedded in the very technologies shaping modern commerce. As AI continues to blur the lines between real and fake, the pressure is on for brands, platforms, and policymakers to respond with equal speed and sophistication. Combating this growing threat will require more than just awareness—it demands collaboration, innovation, and a commitment to restoring trust in the digital marketplace before the counterfeit economy becomes the new normal. For the Silo, Merilee Kern.

Merilee Kern, MBA is a brand strategist and analyst who reports on industry change makers, movers, shakers and innovators: field experts and thought leaders, brands, products, services, destinations and events. Merilee is a regular contributor to the Silo. Connect with her at www.TheLuxeList.com and LinkedIN www.LinkedIn.com/in/MerileeKern.

She designed a sanctuary for herself. Unfortunately, it turned out to be a modern masterpiece. E.1027 Eileen Gray and the House by the Sea

Opens May 16 at the IFC Center in New York City & May 23 at Laemmle Theatres in Los Angeles

Director Beatrice Minger will attend the New York and Los Angeles premieres and is available for interviews.

In 1929, Irish designer Eileen Gray created E.1027 on the sun-soaked Côte d’Azur – a bold and hidden gem of avant-garde architecture. This striking house was meant to be a personal refuge.

But when the legendary architect Le Corbusier stumbled upon it, fascination turned to obsession. He covered its walls with his murals, completely disregarding Gray’s wishes and her vision. His defiant act ignited a battle for creative control, with Gray demanding restitution for the destruction of her work, He ignored her wishes and instead built his famous Cabanon house directly behind E.1027.

E.1027 – Eileen Gray and the House By the Sea is an unusual hybrid docu-fiction film that tells a story about the power of one woman’s creative expression and a man’s desire to control it.

“Eileen Gray was a creative genius and the first woman to conquer the world of architecture at a time when men controlled it all. This new film reflects on Gray’s impressive career and her stunning modernist house on the Cote d’Azur.” – Meredith Taylor, Finito World

“The directors put architecture in dialogue with cinema in order to bring to life the sensibility of a woman who was a visionary yet is too rarely celebrated. Elegant and well thought-out, the film uses the cinematic medium to enrich a discourse.” – Giorgia Del Don, Cineuropa

“Based on the memoirs of Eileen Gray, this meticulously crafted docu-drama, where poetry slips into frames, angles and tones, almost feels like a hallucination.”– Le Monde

“As more women have the opportunity to make films, a distinct form of female narrative based on a particular female gaze and female sensitivity is being developed.” – Melita Zajc, Modern TImes Review

A First Run Features / Architecture & Design Film Festival Release E.1027 – Eileen Gray and the House By the Sea Written & Directed by Beatrice Minger Co-Directed by Christoph Schaub With Natalie Radmall-Quirke, Axel Moustache & Charles Morillon 90 minutes, color, 2024 | English & French w/English subtitles

The Canadian Wood Council has released new Environmental Product Declarations for 5 Canadian manufactured wood products.

“The release of these new EPDs reinforces our commitment to transparency and sustainability in the wood products sector.”

The Canadian Wood Council (CWC) is pleased to announce the release of five new Environmental Product Declarations (EPDs) for Canadian softwood lumber, oriented strand board (OSB), plywood, trusses, and prefabricated wood I-joists. These EPDs provide comprehensive, transparent environmental data on the potential impacts associated with the cradle-to-gate life cycle stages of these essential wood products.

“The release of these new EPDs reinforces our commitment to transparency and sustainability in the wood products sector,” said Peter Moonen, National Sustainability Manager at the Canadian Wood Council. “By providing robust, science-based environmental information, we’re equipping the industry with the tools needed to demonstrate the environmental benefits of wood and support low-carbon construction.“

Developed as Type III declarations by region for business-to-business use across the Canadian industry, they comply with the most stringent international standards, including ISO 21930, ISO 14025, ISO 14040, ISO 14044, applicable product category definition rules, and ASTM’s general program instructions for Type III EPDs. This ensures complete and credible information on the environmental impact that has been verified by an external source. The new EPDs will be able to help designers, construction companies and decision-makers make informed choices about sustainable materials.

“The publication of the new Environmental Product Declarations reinforces our commitment to transparency and environmental responsibility in the wood sector,” says Peter Moonen, National Director of Sustainability for the Canadian Wood Council. “By providing reliable, science-backed environmental data, we are giving industry the tools to demonstrate the environmental benefits of wood and to support low-carbon construction.”

For the Silo, Sarah Hicks.

Environmental Product Declarations can be downloaded from the Canadian Wood Council’s Digital Resource Centre:www.cwc.ca.

Based in Saint-Petersburg, on the shores of the Baltic Sea, Raketa Watch Factory has been creating watches for sailors, submariners, and divers for more than half a century. Raketa presents today a new version of its model for divers – Amphibia.

While preserving both the spirit and identity of its predecessors, this iconic model is now in conformity with all the modern requirements for diving, both in terms of design and functionality:

case made from stainless steel and capable of withstanding pressures at 200 metres depth.

a screw-incrown securing the movement from any water entry.

a unidirectional bezel with a 15-minute scale and luminescent indexes, producing clear clicking sound for error-free adjustment with no risk of accidental misalignment. The start marker is embossed as part of a functional design.

a high-contrast dial with large indexes and hands, easy to read and enhancing dive control. The luminescent coating ensures a bright and long-lasting glow. At greater depths, where visibility is often low and light conditions vary, orange stands out more effectively than any other color because its wavelength is less absorbed by water.

a brightly colored silicone strap crafted for comfort in aquatic environments: with its full-length perforations, you may adjust the size for a snug fit with your wetsuit and prevent water build-up beneath the strap. A second strap in black silicone is included, and swapping is easy with a quick-release system.

The heart of Raketa Amphibia is its automatic movement, manufactured from A to Z at the Raketa Watch Factory in St. Petersburg. The movement’s rotor is adorned with an image of a mermaid designed in the style of illustrations from Russian fairy tales. It reminds every diver of his secret dream — to encounter a beautiful mermaid under the sea.

Price

The cost is 2200 EUR / 3397 CAD (including VAT). For the comfort of customers, Raketa watches are delivered worldwide free of charge by DHL directly up to the front door.

Specifications:

Manufacture:

Raketa Watch Factory (Saint-Petersburg)

Movement:

Calibre:

2615

Functions:

Automatic

Number of jewels:

24

Testing positions:

4

Average rate (s/d):

-10+20

Average running time (h):

40

Frequency/hour:

18.000 / 2.5 Hz

Decoration:

Printing

Case:

Material:

Stainless steel

Size:

41.6 mm

Dial glass:

Sapphire

Back glass:

Sapphire

Water resistance:

20 АТМ

Bezel:

Superluminova

Hands:

Superluminova

Dial:

Superluminova

Straps:

Material:

Silicone

Strap width:

22 mm

Sex:

Male

FR

Raketa Amphibia –Une Raketa pour l’immersion totale

Située à Saint-Pétersbourg, aux bords de la mer Baltique, la manufacture horlogère Raketa a toujours créé des montres pour marins, sous-mariniers et plongeurs. Raketa présente aujourd’hui une version actualisée de sa légendaire Amphibia pour plongeurs.

Tout en conservant l’esprit et l’identité de ses prédécesseurs, le design et les caractéristiques de ce modèle répondent à toutes les exigences modernes d’une montre de plongée :

son nouveau boîtier en acier inoxydable est capable de résister à des pressions jusqu’à 200 mètres de profondeur ;

sa couronne filetée et vissée protège le mouvement de toute pénétration d’eau ;

sa lunette unidirectionnelle avec des index luminescents et à l’échelle de 15 minutes, produit des clics audibles assurant un réglage sans erreur et sans risque de désalignement accidentel. Le repère de départ est en relief ce qui rend son utilisation encore plus pratique ;

son cadran à contraste élevé avec des index et des aiguilles de grande taille, assure une lecture facile et permet d’améliorer le contrôle de la plongée. Le, revêtement luminescent assure une brillance intense et durable. À grande profondeur, où la visibilité est souvent faible et les conditions de luminosité variables, l’orange ressort mieux que toutes les autres couleurs car sa longueur d’onde est moins absorbée par l’eau ;

son bracelet en silicone de couleur vive est conçu pour le confort en milieu aquatique : grâce à ses perforations sur l’ensemble de la longueur, on peut ajuster la taille pour qu’elle s’adapte parfaitement à la combinaison de plongée et éviter l’accumulation de l’eau sous le bracelet. Un autre bracelet en silicone noir est inclus, et le changement de bracelet est très facile grâce au système d’attache rapide.

Le cœur de la Raketa Amphibia est son mouvement automatique, fabriqué de A à Z à la manufacture horlogère Raketa à Saint-Pétersbourg. Son rotor est orné de l’image d’une sirène inspirée par les illustrations des contes folkloriques russes. Elle nous rappelle le rêve secret de tous les plongeurs : rencontrer une magnifique sirène sous la mer.

Coût

Le prix est de 2200 Euros (TVA comprise). Pour le confort de nos clients, les montres sont livrées gratuitement jusqu’à leur porte par DHL.

Haldimand and Norfolk Counties in Ontario, Canada have become an attractive area to explore for marine fossils.

The Great Lakes Basin, once inundated by a vast ancient, shallow sea that covered much of central North America, is today revealing an abundance of fossil corals, invertebrates, and marine organisms found within many limestone formations uncovered by glaciers and erosion.

Haldimand and Norfolk County have especially become an attractive area to explore for fossils of marine organisms by both scientists and amateur fossil collectors who can travel to local locations such as Rock Point Provincial Park near Dunnville, Ontario.

However, these fossils represent more than just evidence of unique life forms that once numbered in the tens of thousands of species co-existing in a marine ecosystem. They are scientific evidence of marine ecosystems in ecological transition, shifting continents, changing climates, and a record of our planets’ every day rotation around the sun.

Many fossil corals found in Haldimand and Norfolk County date around 410 to 360 million years ago. It is a time geologically known as the “Devonian Period”, the “Devonian Reef” or the “Age of Fishes”. During this period, fishes of many different species became abundant in the fossil record. A partly submerged North America, or as yet to be formed Great Lakes Basin, was colliding with Europe close to the equator. Reef building environments began to develop and produce some of the largest reef complexes in the world.

The reef complexes were in large areas of shallow equatorial seas that existed between the continents.

Evidence of a saltwater sea supporting a vast coral reef system once covering southern Ontario over 400 million years ago in the form of fossilized coral deposits support the theory that a coral reef system existed for a very long time. It was in the basins of these former shallow seas that great quantities of rock salt, gypsum, and other types of minerals precipitated, and today, mining industries dig well below the lowest depths of Lake Erie to recover these minerals.

The “Heliophylum halli” is a fossil particular to the Great Lakes region and studies of its growth rings revealed 400 days in one Earth year when this coral was alive.

Exposure of reef basins varies and depends on how glaciers or water erosion has pushed or washed soil off bedrock. Under these conditions, a geologist’s field magnifying glass can help find very small fossils such as radiolarians and diatoms. Otherwise, larger fossils such as different varieties of bivalves (clams), trilobites, and even large fragments of fossilized coral are exposed. In some case, there are discoveries of fossilized marine organisms that are both rare and some times difficult to identify.

The fossilized remains of a Devonian Reef. Rock Point Provincial Park, Ontario.

Rock Point provincial park- exposed fossilized reef system holds an incredibly amount of fossils.

What ended these reef complexes and created one of the greatest mass extinction events of earth’s biota is not completely understood but was a combination of events that took place over a period of 25 million years.

Since species rely on a warm water marine ecosystem for their survival it would seem that a slow and gradual continental shift north from the equator would over time impact a large variety of marine species, including those supported by coral reefs. Therefore, events such as shifting continents, lowering of sea levels, climatic changes influencing land and sea ecologies, and/or possibly a glaciation had significant roles in the extinction of earth’s biodiversity.

The large deposits of fossil corals and invertebrates found in Norfolk and Haldimand County has been of great interest to scientists and fossil collectors for many decades. However, fossil collecting took on a new importance in the last 50-60 years when it was determined there was a connection between growth rings of coral skeletons with the number of days in a year.

Scientists studying samples of coral skeletons from contemporary coral reef systems discovered growth rings on the outer surface of coral skeletons.

By studying a large sample of coral skeletons and determining how many growth rings represented a year’s growth of calcium carbonate, scientists were able to calculate an average of 360 rings per year. Thereby, approximately one growth ring represented one day’s growth for each day of the year. Taking this new information, scientists began collecting large numbers of exceptionally well-preserved coral fossils belonging to the Late Devonian Period. One particular species, found in the Great Lakes region, called a “Heliophylum halli” (see above) exhibited many growth rings developing in one year during this period. The result surprised even scientists.

Fossil coral showed there were approximately 400 growth rings per year 370 million years ago. Therefore, there were about 400 days in a year in the Devonian Period. Astronomers who have calculated that our earth’s rotation has been slowing at a rate of about 2 seconds every 100,000 years have since supported the new information.

Exposures of ancient reef basins can be discovered in dried up stream beds and even under farmers fields.

Despite Haldimand and Norfolk County being a small example of a region once holding a thriving coral reef system, existing over 400 million years ago, the number of fossils of different species exposed is vast. Fossil corals, invertebrates, and species of marine organisms exist in many different shapes, sizes, and can be very fragile. Therefore, whether you are a scientist or amateur fossil collector, the next time you take a walk across the landscape to explore and search for fossils be sure to take along a fossil guide. You never know what new fossil discoveries you might make just walking across the countryside for an afternoon. For the Silo, Lorenz Bruechert.

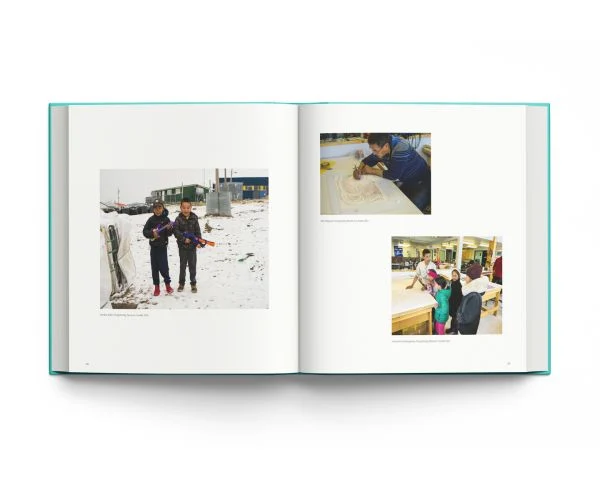

The Metropolitan Museum of Art to Receive Major Gift of Relief Prints by renowned Inuit printmakers from René Balcer and Carolyn Hsu-Balcer.

(New York, March, 2025)—The Metropolitan Museum of Art announced today the landmark gift of the René Balcer and Carolyn Hsu-Balcer Inuit Print Collection, which features over 500 relief prints by renowned Inuit printmakers from multiple regions across Nunavut and Nunavik, the semiautonomous Arctic homeland of Canada’s Inuit population. This important collection, gifted to The Met by René Balcer and Carolyn Hsu-Balcer, is among the strongest examples of Inuit graphic art in the United States. With works ranging from the mid-1940s to the present day, it includes major works by some of the most influential Indigenous women artists in history and will significantly enhance The Met’s collections of Inuit objects. The Balcer Collection represents diverse Inuit printmaking methods, including sealskin and paper stencils; monoprints; and carved stone, or stone-cuts, on paper, and features imagery of birds, animals, Inuit peoples, transformative figures, dreams, cosmologies, and hunting scenes.

Kenojuak Ashevak’s drawings and prints feature fantastical creatures and bold colors and forms. This captivating image of an arctic owl was among the first prints produced by the West Baffin Eskimo Cooperative. It quickly became a Canadian icon, and in 1970 the print was chosen for the country’s commemorative stamp.

“We are deeply grateful to René Balcer and Carolyn Hsu-Balcer for this extraordinary gift, which is a leading collection of Inuit masterworks in a U.S. museum,” said Max Hollein, The Met’s Marina Kellen French Director and Chief Executive Officer. “Mr. and Mrs. Balcer’s dedication to the support of Inuit artists is evident in this magnificent and comprehensive collection that celebrates the remarkable artistry of Native and Indigenous individuals and communities, and we are thrilled to be able to share these prints with visitors in our American Wing galleries.”

René Balcer began collecting Inuit art in Montreal, Canada, in the late 1970s. The René Balcer and Carolyn Hsu-Balcer Inuit Print Collection highlights the famous artists’ collective and printmaking studio at Baffin Island’s Cape Dorset, the source of Inuit printmaking that was established in the 1950s. The original artists working at Cape Dorset collectively identified as the West Baffin Eskimo Co-operative, and in 1960 they released their first official catalogued collection of 41 prints to great critical acclaim. The René Balcer and Carolyn Hsu-Balcer Inuit Print Collection includes some of the most celebrated Inuit artists associated with the collective, such as Jessie Oonark (1906–1985) and Kenojuak Ashevak (1927–2013), whose print The Enchanted Owl (1960) was featured on a commemorative Canadian postal stamp in 1970 and was on view in The Met exhibition A Decade on Paper: Recent Acquisitions, 2014–2024(August 26, 2024–February 23, 2025). Looking ahead, select works in the Balcer Collection will be included as part of ongoing annual rotations in the Art of Native America installation in the Museum’s American Wing.

“This is an aesthetically and culturally significant gift, and it has been an absolute pleasure to work with René Balcer and Carolyn Hsu-Balcer in our mutual goal to more strongly represent Inuit artists in The Met collection,” said Patricia Marroquin Norby (P’ urhépecha), Associate Curator of Native American Art in the American Wing. “The arrival of this beautifully curated collection aligns with our departmental vision to prioritize previously underrepresented artists and the presence, voices, and experiences of peoples and communities who have contributed greatly to our cultural and national identities. We look forward to collaborating with Inuit communities and individual artists to highlight these works in our galleries and programming.”

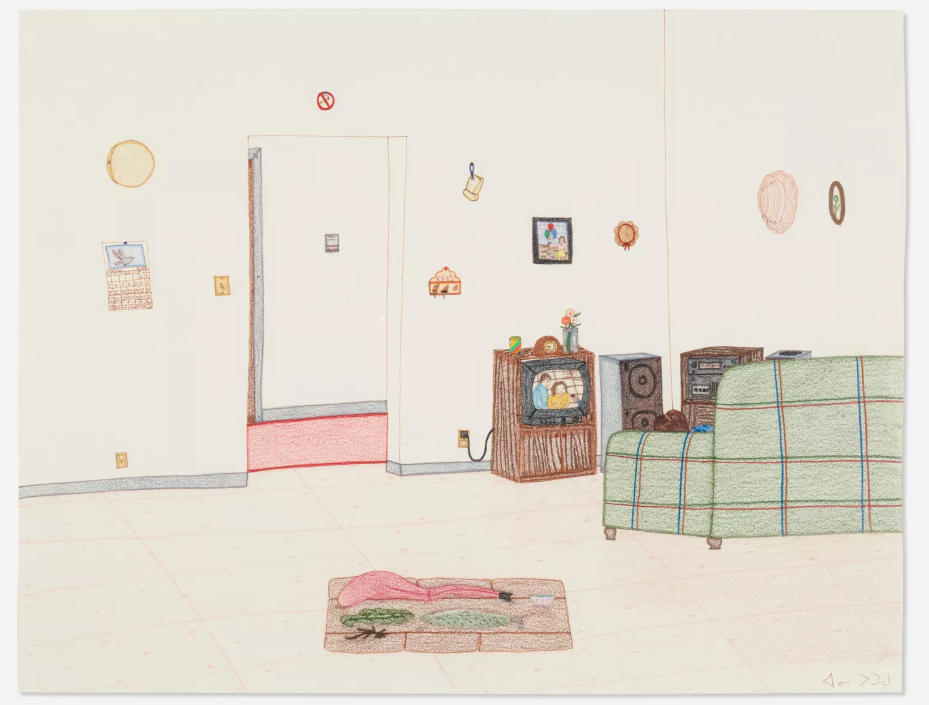

René Balcer and Carolyn Hsu-Balcer said, “One of the greatest challenges the Inuit face vis-à-vis the southern world is invisibility. At best, the Inuit and their brethren in the Circumpolar region are an abstraction to the rest of the world, glimpsed mostly through the distorted lens of pop history. At worst, the reaction the Inuit get when meeting non-Indigenous people is, ‘Oh, I thought you all died off years ago.’ It is our modest hope that this collection will demonstrate that the Inuit and their culture are very much alive and very much engaged in the modern world (to wit, see the following image of Annie Pootoogook’s Watching Jerry Springer from 2003). My wife, Carolyn, and I are very grateful to The Met for accepting the collection and committing its vast resources and reach to showcase to the world the creative brilliance, wisdom, and humor of Inuit artists.”

About René Balcer and Carolyn Hsu-Balcer

René Balcer is an Emmy-winning writer, producer, and creator of critically acclaimed TV series and documentaries. René’s engagement with the Canadian North began as a teenager working in lumber mills, hydro projects, and construction on airstrips in remote communities, often alongside First Nations and Inuit coworkers.

Among other artistic endeavors across North America and Asia, René and Carolyn recently organized and participated in a multiyear artist’s residency with Chinese artist Wu Jian’an and Inuit artists at the Uqqurmiut Centre for Arts and Crafts in Pangnirtung, Nunavut, and with renowned artists Shuvinai Ashoona, Ningiukulu Teevee, and Qavavau Manumie at Kinngait Studios (Cape Dorset). René’s poignant photographs of the Arctic have been featured in gallery exhibitions in New York and appear in his recently published portfolio, Seeing As (ACC Art Books UK). For the Silo, Meryl Cates/ The Metropolitan Museum of Art.

(above) Sample pages from Rene’s “Seeing As” Artbook

About The Met

The Metropolitan Museum of Art was founded in 1870 by a group of American citizens—businessmen and financiers as well as leading artists and thinkers of the day—who wanted to create a museum to bring art and art education to the American people. Today, The Met displays tens of thousands of objects covering 5,000 years of art from around the world for everyone to experience and enjoy. The Museum lives in two iconic sites in New York City—The Met Fifth Avenue and The Met Cloisters. Millions of people also take part in The Met experience online. Since its founding, The Met has always aspired to be more than a treasury of rare and beautiful objects. Every day, art comes alive in the Museum’s galleries and through its exhibitions and events, revealing both new ideas and unexpected connections across time and across cultures.

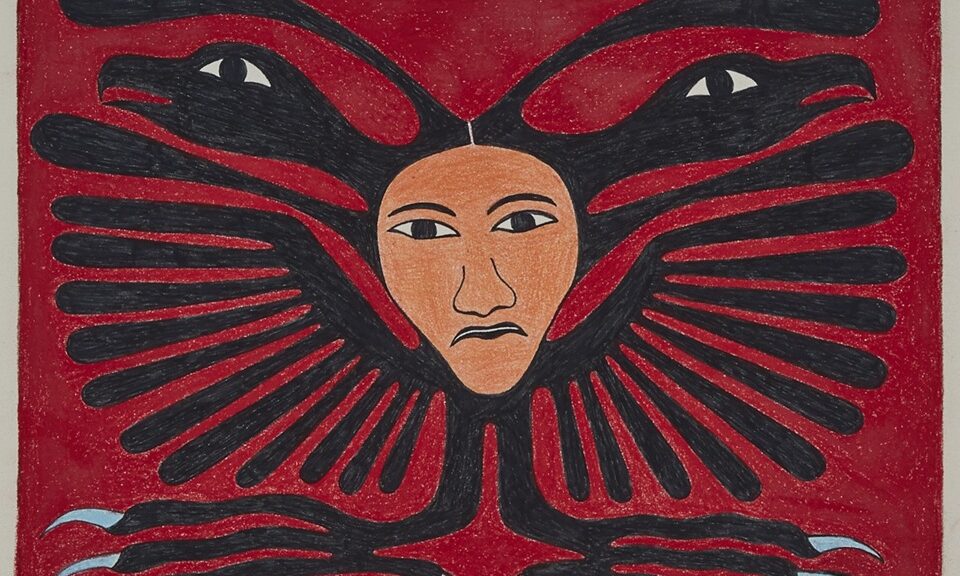

Feature Image: Kenojuak Ashevak. “Untitled (red woman/birds/wings/feet),”Drawing, pencil and ink 10x14in, 25.4×35.6 cm. Waddington, 9/18/20. René Balcer and Carolyn Hsu-Balcer Collection, Gift of René Balcer and Carolyn Hsu-Balcer, 2024 Kenojuak Ashevak. “Untitled (red woman/birds/wings/feet),”Drawing, pencil and ink 10x14in, 25.4×35.6 cm. Waddington, 9/18/20. René Balcer and Carolyn Hsu-Balcer Collection, Gift of René Balcer and Carolyn Hsu-Balcer, 2024

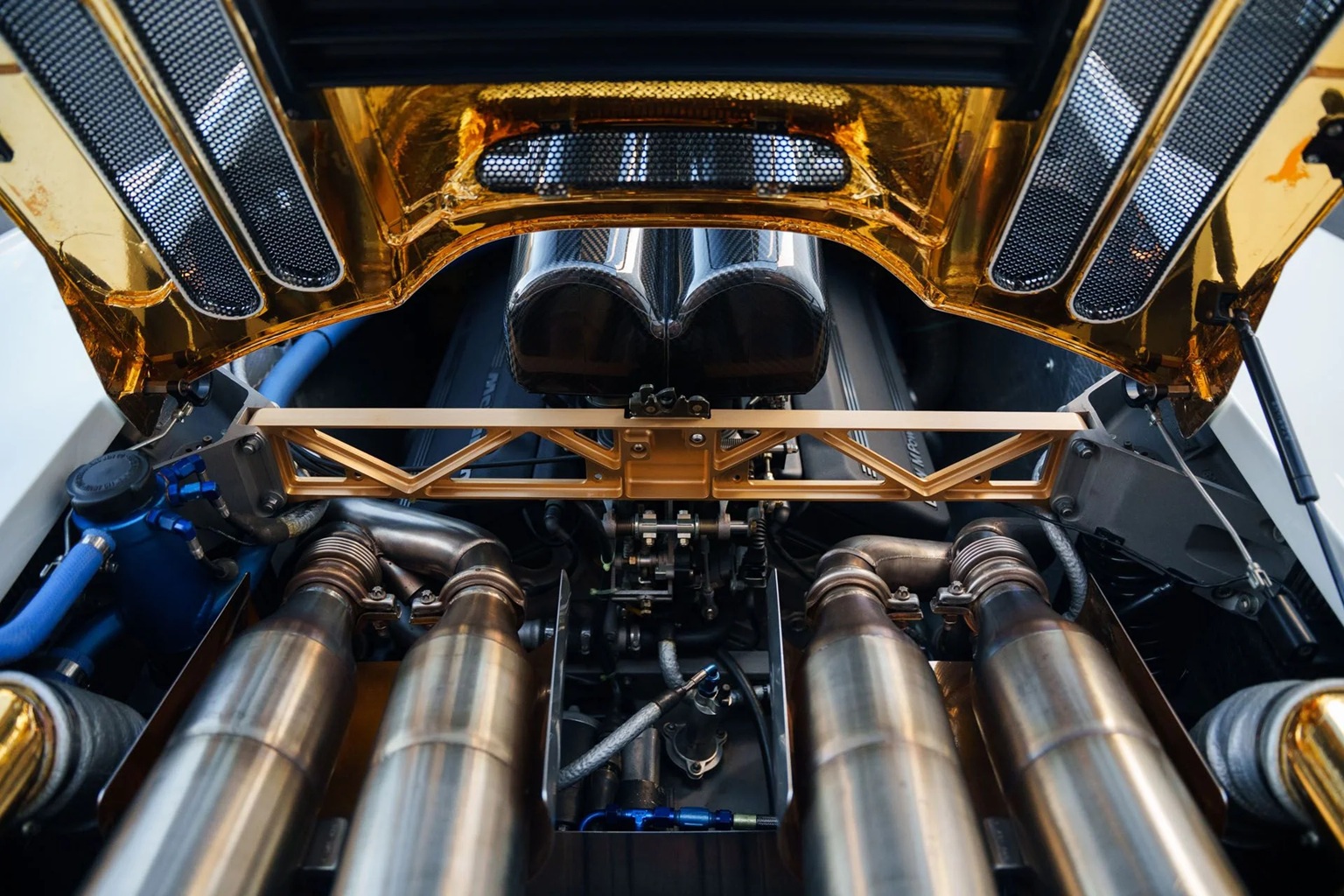

One of only two McLaren F1 road cars finished in the striking Marlboro White exterior

Attractive interior configuration with light blue Alcantara driver’s seat and dark blue/grey leather and Alcantara passenger seats

Incredibly low mileage with just 1,291 kilometers (802 miles) from new

Unaltered and maintained exclusively by McLaren Special Operations in Woking throughout its life

Received a fuel cell replacement in 2021, followed by comprehensive recent maintenance in November 2024

Documented ownership history from new, beginning with Japanese racing team owner Kazumichi Goh

Complete with original owner’s manuals, fitted luggage set, tool roll, and Facom toolchest

Chassis No. SA9AB5AC6S1048053

The McLaren F1 emerged from what might be the most consequential airport delay in automotive history. In 1988, following the Italian Grand Prix, TAG-McLaren Group executives Ron Dennis and Mansour Ojjeh found themselves stranded at Linate Airport alongside McLaren’s Technical Director Gordon Murray and head of marketing Creighton Brown. Their conversation turned to creating the ultimate road car—not just another supercar, but in Dennis’s words, “…the finest sports car the world had ever seen.”

In May 1992 at Le Sporting Club Monaco, the McLaren F1 redefined the supercar genre upon its unveiling. Built around a carbon fiber monocoque—a world first for a production road car—and powered by a bespoke 6.1-liter BMW Motorsport V12 engine, the F1 delivered 627 horsepower and a power-to-weight ratio of 550 horsepower per ton. Its unique central driving position, gold-lined engine bay, and no-compromise approach to performance and driver engagement set new standards that remain unmatched to this day. Limited to just 106 examples across all variants, only 64 were built as standard road cars, making them the most revered and sought after supercar of the modern era.

This superlative example of the F1, chassis number 053, was ordered on 31 March 1995, and assigned production sequence 044. Assembly began on 28 July 1995, with the car being officially delivered “ex-works” on 27 November 1995, showing just 193 kilometers on the odometer. The original purchaser was Kazumichi Goh, the Japanese businessman behind Team Goh, which would go on to win the All Japan Grand Touring Car Championship (JGTC) in 1996 with a pair of McLaren F1 GTRs sponsored by Philip Morris cigarette brand Lark.

Chassis 053 featured a highly distinctive specification highlighted by its Marlboro White exterior finish—one of only two F1 road cars to wear this color. The cabin was finished with a unique blue-themed interior featuring dark blue/grey leather with pierced blue/grey Alcantara cloth central panels for the passenger seats, while the central driver’s seat was entirely covered in light blue Alcantara. This bespoke specification was completed with blue Wilton carpet, light blue Alcantara headlining, and an optional black suede steering wheel. The car was also delivered with a matching bespoke luggage set in dark grey leather with a blue Alcantara strip carrying the embossed chassis number. Factory driver settings were configured with the steering wheel at height position A (highest), pedals at position C (long), reach at position A (near), clutch foot rest at position D (extra long), and standard seat with extra long rails.

In 2004, chassis 053 was purchased by another Japanese collector. By late 2006, the car showed just 432 kilometers when it was sold by WHA Corporation of Nagoya, Japan, to dealer SPS Automotive Ltd. (Hong Kong) on 28 November. The car subsequently came to Europe in 2007 when it was acquired by dealer Lukas Huni AG in Switzerland on behalf of a European client with a recorded mileage of 482 kilometers. On 14 March 2014, chassis 053 was sold via Morris & Welford to collector in the United States. During this ownership, the car spent time in both the U.S. and U.K., and the mileage had increased to 1,108 kilometers. On 16 November 2016, the car was acquired by its next long-term European owner via McLaren Special Operations in Woking and subsequently registered in the U.K. with the appropriate license plate “53 MCL.”

Throughout its life, chassis 053 has been meticulously maintained by McLaren Special Operations. The service book records regular maintenance with all work completed at McLaren’s Woking headquarters on December 12, 2006 (481 kilometers), 14 June 2010 (998 kilometers), 25 October 2016 (1,185 kilometers), 24 April 2018 (1,238 kilometers), and most recently on 12 November 2024 (1,290 kilometers). In July 2021, the car received a comprehensive fuel cell service at McLaren Special Operations totaling £52,061.55 (excluding VAT), which included £31,624.50 in labor charges and £15,472.74 for the fuel cell unit itself. A covering letter from McLaren Heritage Manager Thomas Reinhold noted the return of a “favourite F1” to MSO, an F1 that also “drives extremely well.”

Further work was carried out in November 2021, including replacement of various pipes, fittings, suspension rose-joints and bushes, plus a new water pump at a cost of £23,992.05 (excluding VAT). Most recently, the car returned to MSO in late 2024 for a “3 Year Life Items” service, during which the steering wheel battery, instrument binnacle battery, key fob battery, air conditioning receiver dryer, engine oil and filters, gearbox oil, and coolant were all replaced. The car also underwent a full suspension set-up and headlamp alignment at a cost of £4,861.10 (excluding VAT). Heritage Manager Michael Wrigley’s covering email following this most recent service summed up the car’s exceptional condition: “It’s a truly lovely example so there is very little of note to comment on!”

With just 1,291 kilometers recorded from new, chassis 053 represents one of the lowest mileage and most original McLaren F1 road cars in existence. Its unique color combination, low mileage, comprehensive documentation, complete set of factory tools, owner’s manuals, and fitted luggage make it an unparalleled example of Gordon Murray’s masterpiece. Maintained throughout its life without regard to cost and exclusively serviced by McLaren Special Operations, this McLaren F1 offers its next custodian the opportunity to acquire the ultimate modern collector car in truly museum-quality condition.

A RIG THAT’S SEEN IT ALL (And would probably rather not have)

Born in the 50s for the People’s Liberation Army, the type 56 Chicom Chest Rig is without a doubt a Cold War Legend of the East. The Viet Cong rocked it in Vietnam, Soviet Spetsnaz snagged it in Afghanistan, and every commie-aligned rebel and LARP-ist from Rhodesia to the borders of South Africa copied it.

Naturally the Type 56 caught the attention of the US Special forces in Vietnam and other Western countries too. The US used the rig in conjunction with the family of AKMs borrowed from downed VCs & blend in with the enemy as much as a 6’4 Iowan MACVSOG commando could – it’s high speed and ease of use changed the western world’s opinions on belt-mounted kit as a means of combatting Insurgency.

A spiritual evolution to the bandoleers of old, the Type 56 would go on to inspire the Russian Lifchik, and spread the gospel of chest-stowed-ammo to the western world via Soldiers of Fortune in Rhodesia & South Africa. It still saw use deep within enemy territory in the past few decades. And of course, we could even credit the USA’s very own Pattern 84 rig to the Type 56’s legacy.

To us Zoomers It’s been made famous again by its depictions in cyberspace and on the big screen – CoD Black Ops, Escape from Tarkov, and hit films like Apocalypse Now & Platoon all show the influence of the OD canvas OG.

So stay loaded, unhinged and within the limits of Xi Jinping’s social credit system with the type 56.Or go hog wild and modify it. It’s only $30usd / $42.94cad from our friends at kommandostore.com and is great to get your sewing and seam ripping practice in. Just make sure the party isn’t watching, they don’t like when us filthy capitalists misuse their gear, we wouldn’t want a Cold War II: 电动布加洛.

In case this message is seen by CCP members: Zǎo shang hǎo zhōng guó! Xiàn zài wǒ yǒu Chicom rig—wǒ hěn xǐ huān! We love TEMU, Alibaba, and Xiaohongshu!

Boulder, Colorado, March, 2025 – PS Audio announces the release of The Audiophile’s Guide, a comprehensive 10-volume series on every aspect of audio system setup, equipment selection, analog and digital technology, speaker placement, room acoustics, and other topics related to getting the most musical enjoyment from an audio system. Written by PS Audio CEO Paul McGowan, it’s the most complete body of high-end audio knowledge available anywhere.

The Audiophile’s Guide hardcover book series is filled with clear, practical wisdom and real-life examples that guide readers into getting the most from their audio systems, regardless of cost or complexity. The book includes how-to tips, step-by-step instructions, and real-world stories and examples including actual listening rooms and systems. Paul McGowan noted, “think of it as sitting down with a knowledgeable friend who’s sharing hard-won wisdom about how to make music come alive in your home.”

The 10 books in the series include:

The Stereo – learn the essential techniques that transform good systems into great ones, including speaker placement, system matching, developing critical listening skills, and more.

The Loudspeaker – even the world’s finest loudspeakers will not perform to their potential without proper setup. Master the techniques that help speakers disappear, leaving the music to float in three-dimensional space.

Analog Audio – navigate the world of turntables, phono cartridges, preamps and power amplifiers, and vacuum tubes, and find out about how analog sound continues to offer an extraordinary listening experience.

Digital Audio – from sampling an audio signal to reconstructing it in high-resolution sound, this volume explains and demystifies the digital audio signal path and the various technologies involved in achieving ultimate digital sound quality.

Vinyl – discover the secrets behind achieving the full potential of analog playback in this volume that covers every aspect of turntable setup, cartridge alignment, and phono stage optimization.

The Listening Room – the space in which we listen is a critical yet often overlooked aspect of musical enjoyment. This volume tells how to transform even challenging spaces into ideal listening environments.

The Subwoofer – explore the world of deep bass reproduction, its impact on music and movies, and how to achieve the best low-frequency performance in any listening room.

Headphones – learn about dynamic, planar magnetic, electrostatic, closed-back and open-air models and more, and how headphones can create an intimate connection to your favorite music.

Home Theater – enjoy movies and TV with the thrilling, immersive sound that a great multichannel audio setup can deliver. The book explains how to bring the cinema experience home.

The Collection – this volume distills the knowledge of the above books into everything learned from more than 50 years of Paul McGowan’s experience in audio. Like the other volumes in the series, it’s written in an accessible style yet filled with technical depth, to provide the ultimate roadmap to audio excellence and musical magic.

Volumes one through nine of The Audiophile’s Guide are available for a suggested retail price of $39.99 usd , with Volume 10, The Collection, offered at $49.99 usd. In addition, The Audiophile’s Guide Limited Run Collectors’ Edition is available as a deluxe series with case binding, with the books presented in a custom-made slipcase. Each Collectors’ Edition set is available at $499.00 usd with complimentary worldwide shipping.

About PS Audio Celebrating 50 years of bringing music to life, PS Audio has earned a worldwide reputation for excellence in manufacturing innovative, high-value, leading-edge audio products. Located in Boulder, Colorado at the foothills of the Rocky Mountains, PS Audio’s staff of talented designers, engineers, production and support people build each product to deliver extraordinary performance and musical satisfaction. The company’s wide range of award-winning products include the all-in-one Sprout100 integrated amplifier, audio components, power regenerators and power conditioners.

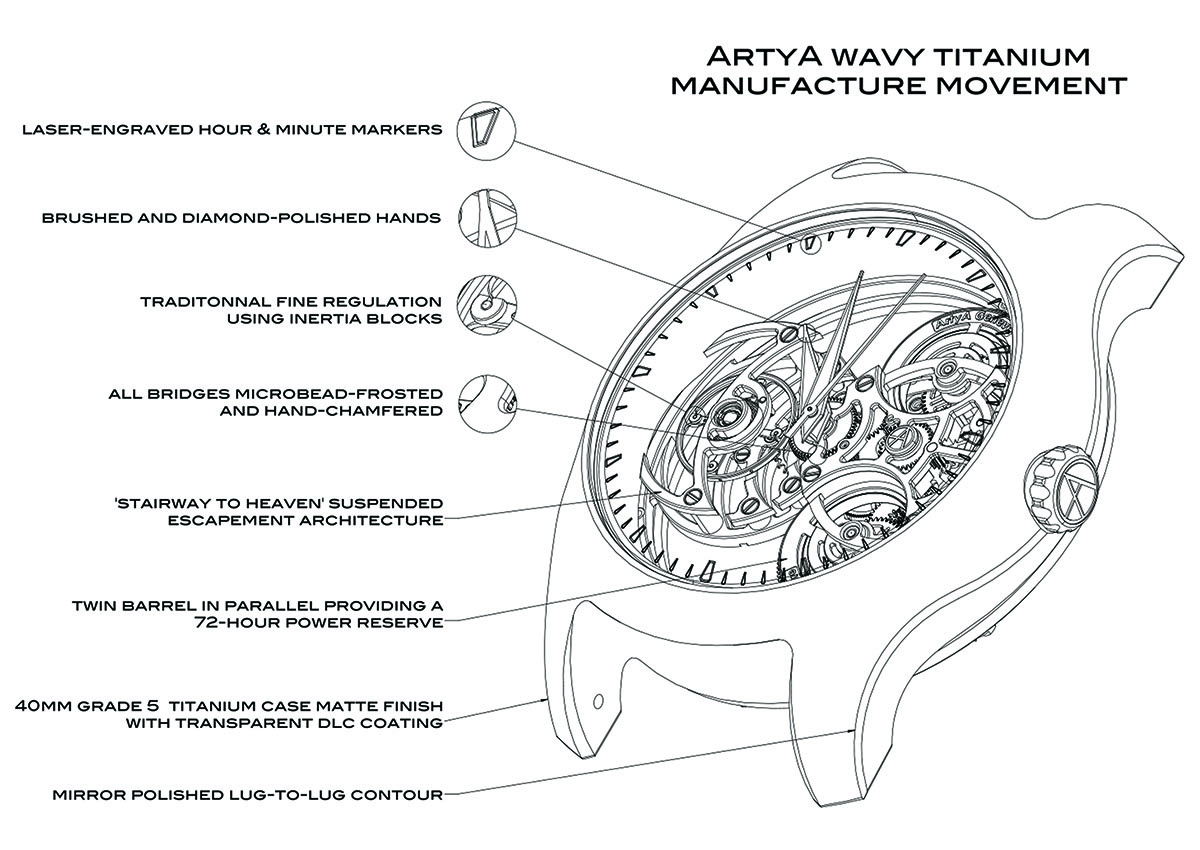

ArtyA unveils an avant-garde horological creation:

“Purity Wavy HMS Mirror” A fully in-house caliber reimagined through masterful handcraftsmanship. The perfect union of design and comfort, encased in the groundbreaking Wavy case, crafted from titanium with a transparent protective DLC coating. The first-ever mirror casebackStairway To Heaven: The Movement At the heart of this exceptional timepiece, ArtyA’s latest in-house caliber: Stairway To Heaven HMS. This manual-winding movement embodies the Manufacture’s dedication to both visual spectacle and horological excellence: • Microbead-frosted and hand-chamfered minute wheel train and balance bridges. • Pulsing at 4 Hz, the spectacularly “starified” escapement is positioned like a podium centerpiece, suspended in mid-air. • Traditional fine regulation – a hallmark of haute horlogerie that ensures optimal precision. This process involves meticulously adjusting the balance wheel’s inertia using peripheral weights (inertia blocks) to maintain the hairspring’s steady and consistent oscillation. The result: optimized caliber performance and lasting chronometric stability. • Twin barrels, working in parallel, equipped with longer, finer mainsprings for a more stable and linear energy release. The polished barrel blade reduces friction for improved efficiency. The redesigned drum barrels, with fluid, curving lines, seamlessly integrate with the bold bridge architecture of the movement. Proudly bearing the manufacture’s name and caliber designation, this subtle detail completes the movement’s refined aesthetic. Wavy Titanium Case A bold evolution in the Wavy collection, this is the first case crafted from grade 5 titanium, a material prized for its strength and lightness. • Ultra-light yet incredibly strong, titanium embodies both modernity and innovation, delivering exceptional comfort without compromising durability. • The matte finish results from meticulous hand polishing, followed by microbead frosting for a refined texture. • A transparent DLC coating boosts resistance to scratches, shocks, and fingerprints. For comparison, stainless steel has a Vickers hardness of 200 HV, titanium 400 HV, and transparent DLC-treated titanium an impressive 1,200 HV (1,800 HV for the black DLC version). • A mirror-polished lug-to-lug contour adds a discreet yet sophisticated touch, enhancing the timepiece’s elegance without diluting its avant-garde appeal. This meticulous finish – exceptionally complex to achieve on titanium – creates a striking contrast with the case’s matte surface, balancing power with refinement. • Designed by Jérémie Arpa, son of Yvan Arpa, the case embodies independent, family-driven watchmaking at its finest. Its flowing, organic contours evoke the power of ocean waves, an effect heightened by titanium’s natural opacity – delivering a case design unlike anything seen before in haute horlogerie.

Mirror Effects The Wavy Titanium’s mirror caseback introduces an unprecedented innovation, a world first in watchmaking: • A fully reflective surface that offers a striking new way to experience the movement. • From the front, seeing through to the mirrored bottom creates the illusion of depth, with the movement seemingly floating in space, enhancing the ethereal purity of the skeletonized caliber’s aesthetic. • From the back, the one-way mirror effect teases the complexity of the movement without fully revealing it complexity, adding an element of mystery and sophistication.

Limited Edition of 99 pieces Case Grade 5 titanium, satin-finished, mirror-polished lug-to-lug contour Transparent or black DLC protective coating Diameter40 mm Thickness13 mm Water resistance50 meters Caseback Screw-in, engraved, fitted with a one-way mirror Crystal Sapphire, triple ant-reflective coating, laser-engraved chapter ring Hands Brushed and diamond-polished Crown Engraved with the ArtyA signet Caliber ArtyA Purity Stairway To Heaven HMS in-house movement Winding Manual Indications Hours, minutes, and central seconds Power reserve Minimum 72 hours, thanks to twin parallel barrels Frequency 4 Hz (28,800 vph) Finishes Fine regulation through precision adjustment of inertia blocks on the balance wheelMicrobead-frosted minute wheel train and balance bridgesHand-chamfered edgesPolished mainsprings to optimize friction in the barrel assemblies Strap Alligator or grey nubuck leather Buckle ArtyA pin buckle, available with or without black DLC coating Swiss Made Entirely designed and crafted between Geneva and the Swiss Jura Price (excluding VAT)Titanium & Black Titanium CHF 25,900 (reference price) EUR 27,900 (subject to exchange rate) USD 29,900 (subject to exchange rate) CAD 42,754 Also available with transparent, hued or NanoSaphir case From CHF 44,900 (reference price) From EUR 47,900 (subject to exchange rate) From USD 50,900 (subject to exchange rate) VERSION FRANÇAISE

If you have them should you keep them? Read on via this interesting article from our friends at Hagerty.

The nuts and bolts that make up our beloved automobiles have not changed that much over the last 150 years. But the tools needed to maintain them? Those have changed a lot. Software has cemented itself as part of a service technician’s day-to-day regimen, relegating a handful of tools to the history books. (Or, perhaps, to niche shops or private garages that keep many aging cars alive and on the road.)

How many of these now-obsolete tools do you have in your garage? More to the point, which are you still regularly using?

Though spark-plug gap tools can still be found in the “impulse buy” section of your favorite parts store, these have been all but eliminated from regular use by the growing popularity of iridium and platinum plugs. These rare-earth metals are extremely resistant to degradation but, when it comes time to set the proper gap between the ground strap and electrode, they are very delicate. That’s why the factory sets the gap when the plug is produced.

These modern plugs often work well in older engines, meaning that gapping plugs is left for luddites—those who like doing things the old way just because. Nothing wrong with that; but don’t be surprised if dedicated plug-gapping tools fade from common usage fairly quickly.

Verdict: Keep. Takes up no real space.

Dwell meter

sodor/eBay

50 years ago, a tuneup of an engine centered on the ignition system. The breaker points are critical to a properly functioning ignition system, and timing how long those points are closed (the “dwell”) determines how much charge is built up in the ignition coil and thus discharged through the spark plug. Poorly timed ignition discharge is wasted energy, but points-based ignition systems disappeared from factory floors decades ago, and drop-in electronic ignition setups have never been more reliable (or polarizing—but we’ll leave that verdict up to you.)

Setting the point gap properly is usually enough to keep an engine running well, and modern multifunction timing lights can include a dwell meter for those who really need it. A dedicated dwell meter is an outdated tool for a modern mechanic, and thus most of the vintage ones are left to estate sales and online auction sites.

Verdict: Toss once it stops working. Modern versions are affordable and multifunctional.

Distributor wrench

Snap On tools

When mechanics did a lot of regular timing adjustments and tuning, a purposely bent distributor wrench made their lives much easier. However, much like ignition points, distributors have all but disappeared. Thanks to coil-on-plug ignition systems and computer-controlled timing, the distributor is little more than a messenger: It simply tells the computer where the engine is at in its rotation.

Timing adjustments have become so uncommon that a job-specific tool is likely a waste of space. If you’ve got room in your tool chest, keep yours around; but know that a standard box-end wrench can usually get the job done and is only fractionally less convenient than the specialized version.

Verdict: Keep if you have them. No need to buy if you don’t.

Prior to the required standardization of on-board diagnostic computers by the U.S. in 1996, a single car could host a wild mix of analog and digital diagnostic methods. OBDII, which stands for On-Board Diagnostic II, wasn’t the first time that a small computer was used to pull information from the vehicle via an electronic connection; it merely standardized the language.

Throughout the 1980s and early 1990s each OEM had its own version of a scan tool. Now those tools can be reverse-engineered and functionally spoofed by a modern computer, allowing access to diagnostic info tools that, at the time, were only available to dealers. Since many pre-OBDII cars are now treated as classics or antiques and driven far less frequently, the need for period-correct diagnostic tools is dropping.

Verdict: Keep. These will only get harder to find with time, and working versions will be even rarer.

Distributor machine

A distributor is simple in concept. Trying to balance the performance and economy of the ignition system, with the distributor attached to a running engine, and achieving proper operation starts to get pretty complicated. That’s where a distributor machine comes in.

A distributor is attached to the apparatus and spun at engine speed by an electric motor. This allows you to literally see how the points are opening and closing. You can also evaluate the function of vacuum or mechanical advance systems. These machines are still great but the frequency that this service is needed these days is few and far between, especially when trying to justify keeping a large tool around and properly calibrated.

Verdict: Keep, if you are a specialty shop or tool collector.

Engine analyzer

ajpperant

Even a casual enthusiast can see there is a lot more information that can be gleaned from a running engine than whatever readouts might be on the dash. Enter the engine analyzer, a rolling cabinet of sensors and processors designed to fill in the data gaps between everything that is happening in a car and what its gauges report.

An engine analyzer is essentially a handful of additional instruments packaged into a small box hanging around the bottom of your tool drawers. It can also house a lot of sensors in a giant cabinet, which was likely wheeled into the corner of the shop in 1989 and left to gather dust. Now engine analyzers can be found listed online for as cheap as $200usd/ $287cad.

The funny thing is that many of the sensors in these engine analyzers are often the same systems that come built into modern dynamometer tuning systems. In a dyno, the sensors allow the operator to see more than max power; they also show how changes to an engine’s tune affect emissions. Maybe engine analyzers didn’t disappear so much as change clothes.

Verdict: Toss. The opportunity cost of the space these take up can be tough for most home garages. Sensors went out of calibration decades ago so the information you might get from one is dubious at best.

Most pneumatic tools (for home shops)

Ingersoll Rand

Air tools hold an odd place in the hearts of many gearheads. For many years the high-pitched zizzzz and chugging hammers of air-driven die grinders and impact drills were the marks of a pro. Or, at least, of someone who decided that plumbing high-pressure air lines around the shop was easier than installing outlets and maintaining corded tools. Air tools are fantastic for heavy use, as they are much easier to maintain and can be rebuilt and serviced.

Those tools can really suffer in lack of use, though, since pneumatic tools rely on seals and valves, neither of which deal well with dry storage. Battery tools have caught up to air tools for most DIY folk. No more air lines or compressors taking up space in the shop—and requiring additional maintenance—and, in return, a similarly sized yet more agile tool.

Verdict: Keep, if you already have the compressor. Don’t have one? Invest in battery tools.

Babbitt bearing molds/machining jigs

Every engine rebuild has to have bearings made for it in some fashion. Today’s cars use insert bearings that are mass-produced to surgical tolerances for a multitude of applications. If you wanted—or more accurately needed—new bearings in your Model T circa 1920, you needed to produce your own … in place … inside the engine. Welcome to Babbitt bearings.

The process is a true art form, from the setup of the jigs to the chemistry of pouring molten metal and machining the resulting orbs to actually fit the crankshaft and connecting rods. Now there are newly cast blocks for your T that replace the Babbitt with insert bearings. Since those antique Ford engines just don’t get abused the way they used to, and lead fairly pampered lives, they need rebuilding far less often than they did in-period. Modern oils also do a better job of protecting these delicate bearings. Since they are less and less in demand, the tooling and knowledge to make Babbitt bearings are difficult to find, and precious when you do.

Verdict: Keep. It’s literally critical to keeping a generation of cars alive.

Split-rim tire tools

Universal Rim Tool Company

Among the realm of scary-looking tools that have earned their infamy, split-rim tools hold court. The concept is simple: The rim is sectioned, allowing it to contort into a slight spiral that can be “screwed” into a tire. (This is almost the reverse of a modern tire machine, which stretches the tire around a solid wheel rim.) When tires needed tubes, both tire and rim were relatively fragile, and the roads were rough, split rims were popular—and for good reason. Now the tooling for drop-center wheels is ubiquitous and shops often won’t take on split-rim work. Success is hard to guarantee, even if techs are familiar with split rims—and they rarely are.

Verdict: Keep. No substitute for the right tools with this job.

These tools might not make much sense in a dealership technician’s work bay, but that doesn’t mean they should disappear forever. Knowing how to service antiquated technology is as important as ever, whether using old tools or new ones. If you’ve got any of these items, consider it your responsibility to document what the tool does and how to safely use it. Keeping alive the knowledge of where our modern tools came from is powerful.

JG O’Donoghue imagines a ‘versus’ scenario to demonstrate the struggle of ‘languages at risk’

There is a mass decline in linguistic diversity happening all over the planet and in places geographically far apart and I think that if things don’t change, the loss of language diversity will be immense.

In the book, Irish in the globalcontext, Suzanne Romaine mentions that linguists believe 50 to 90 % of the world’s estimated 6,900 languages will simply vanish over next 100 years.

At this moment in time, 85% of the world’s languages have fewer than 100,000 speakers and over half of the world’s remaining languages are spoken by just .2 % of the world’s population. These facts have informed my work and have become the wider subject of my illustrations, specifically the linguistic decline of the Irish language.

In some ways the battle between the Irish and the English languages is one of the defining features in modern Irish culture, but it is Irish which defines this island more, and the Irish language tells the entire history of Ireland in its influences and in its form.

Ruairí Ó hUiginn said in his book The Irish language: you have influences of Latin from the Christianization of Ireland in ecclesiastical words, influences from Viking invasions in words for “seafaring, fishing and trade”, influences from the militaristic Normans [ French CP] in words for “architecture, administration and warfare”, and from English colonialism you get English in every day words.

“To create my intended mood, the english words are given a general typography while the Irish words are given a distinctive script reminiscent of Geoffrey Keating’s book Foras Feasa ar Eirinn”

Each influence shows an aspect of Irish culture. What people forget to realize is that a language is much more than something spoken to express oneself. Ancient peoples created language in an attempt to describe the world around them and the world within them, in other words their worldview.

An example in Irish is- you don’t say ‘I’m angry’, you say ‘tá fearg orm’, which means ‘I have an anger on me’.

Nevertheless, Irish is important internationally too, and Irish is the third oldest written language in Europe, after Latin and Greek, and as a spoken language it may even be older than both.

How should an artist illustrate a language? And more specifically the struggle of one language with another? I choose nature as my metaphor, from the ancient forests of Ireland, mostly gone now, to Islands which stand for thousands of years but are slowly worn away by the tide. The words that make up these landscapes are either ‘for’ or ‘against’.

My illustrations therefore visualize the real life drama of ancient language versus modern language.

I imagine a “versus” scenario. On the “against” side I chose English words plucked from peoples statements in online forums and in letters to newspapers. On the “for” side I chose Irish words, and they were chosen from recent investigations into the creation of the ancient Irish language. Irish words in my illustrations such as “dúchas (heritage), tír (country), litríocht(literature), and stair(history)” reflect the Irish language’s cultural importance, while “Todhchaí(future), féinmhuinín(self-confidence), beatha(life), and anam(soul)” reflect its importance in a metaphysical way to Ireland.

The Irish language forest- An Coill Teanga Gaeilge

The english ‘against’ words can range from the practical benefits of english within subjects such as “tourism, movies, business, and comics,” to words that reflect the interaction of English speakers with Irish. To illustrate the concept, I chose words like “conform, bend, harass, and adapt”.

To create my intended mood, the english words are given a general indistinctive typography reflecting uniform mono-linguilism, while the Irish words are given a distinctive Irish manuscript/Gaelic script reminiscent of Geoffrey Keating’s 17th century book- Foras Feasa ar Éirinn/History of Ireland.

The core message in my illustrations is a positive one, the sun is rising for a new day as the Irish language holds on, like a lot of minority languages. It is diminished but not beyond hope. I believe it can make a comeback, and this is exactly what is happening all over this country today, because of the work of people far more dedicated than myself. I hope my work can help reinforce linguistic diversity as well as all forms of heritage. I have the will to preserve these for future generations, so they too can live in a world full of diversity spending their lives discovering and exploring it in all its beautiful variety.

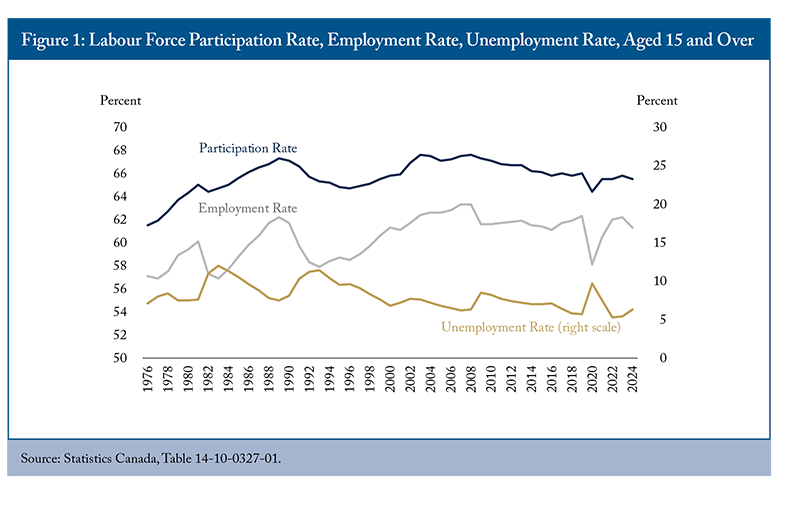

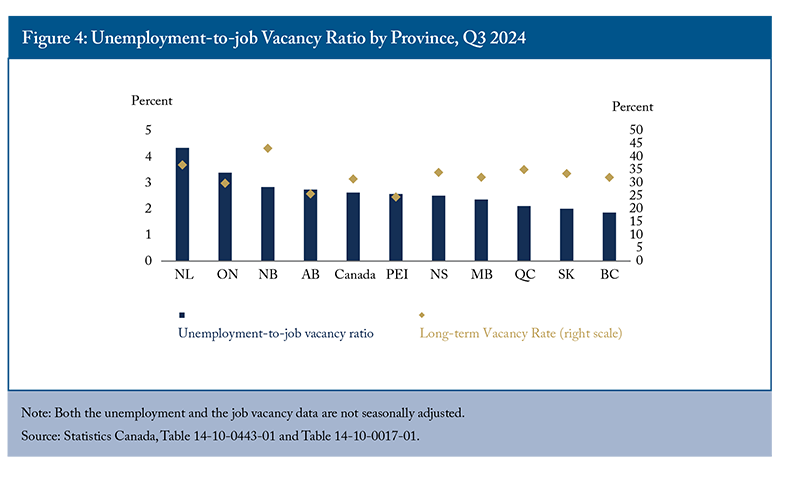

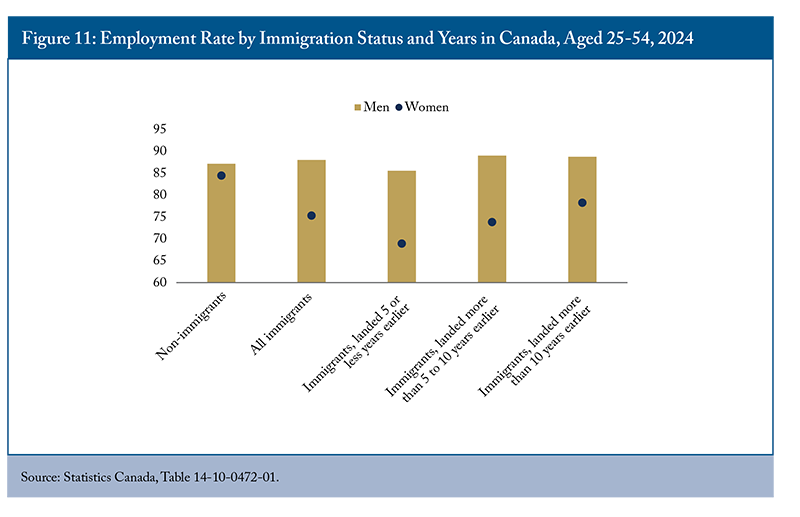

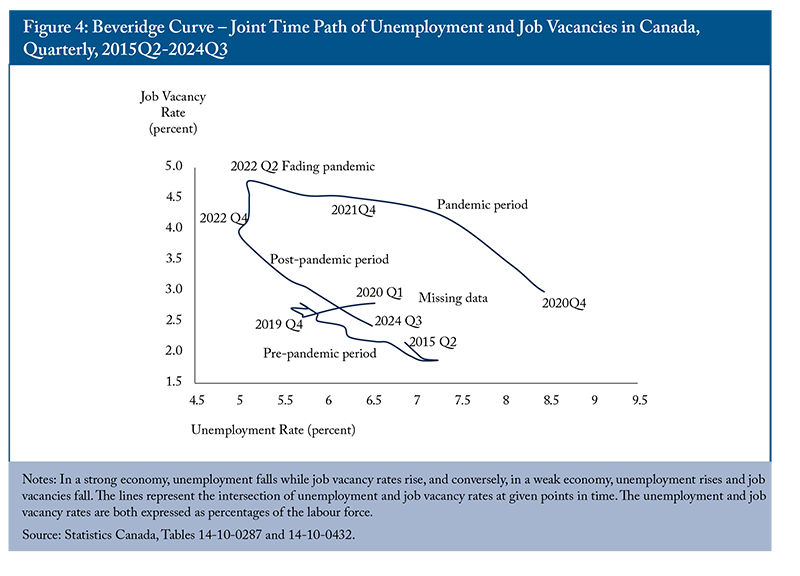

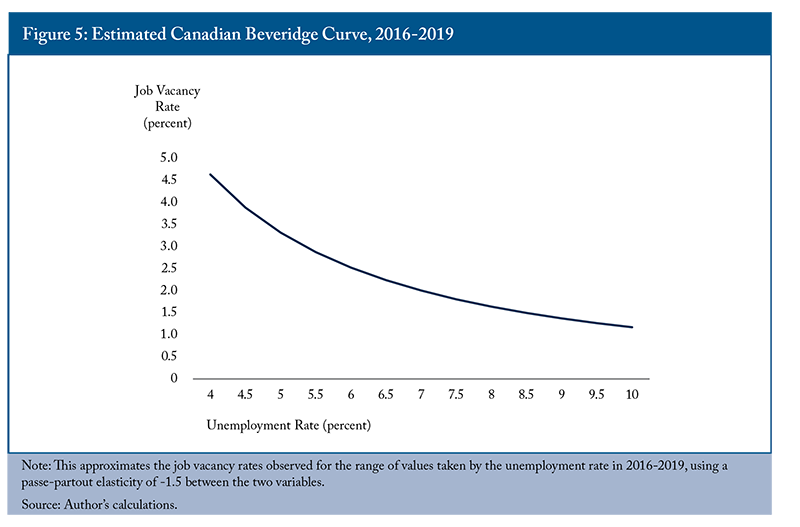

In 2024, Canada’s labour market showed modest growth, with job creation continuing but lagging rapid population growth. This led to an increase in the unemployment rate, reflecting a mismatch between labour force expansion and job creation rather than a decline in sector-specific labour shortages.

Ongoing challenges persist, such as declining labour productivity, sector-specific labour shortages, underemployment, demographic shifts and disparities, and regional imbalances.

Our international comparisons show that Canada typically ranks at or below the Organisation for Economic Co-operation and Development (OECD) average in terms of labour force participation and employment rates for certain population segments. This is largely due to weaker performance in specific regions, such as the Atlantic provinces, and pension policies that incentivize early retirement.

This labour market review emphasizes the need for tailored policies to improve labour market outcomes for seniors and immigrants. Recommendations include gradually increasing the retirement age, offering high-quality training support, and easing labour mobility barriers.

Introduction

The labour market is where economic changes most directly affect working-age Canadians, influencing their job opportunities and income. The supply of labour also determines the availability of Canadians’ skills and knowledge to employers who combine them with capital to produce goods and services that drive our national income and its distribution among income classes. Therefore, the labour market is one of the most important components of Canada’s – or any – economy.

In 2024, Canada’s labour market saw moderate growth, with employment rising to 20.7 million jobs. However, the employment rate declined to 61.3 percent, down from 62.2 percent in 2023, and remains below the pre-pandemic level of 62.3 percent in 2019. While over 1.7 million employed persons have been added since 2019, employment growth has lagged behind population growth, partly due to an aging population, despite high levels of immigration.1 The unemployment rate also increased, reflecting a gap between job creation and labour force expansion, partly due to limited absorptive capacity to keep pace with population growth.

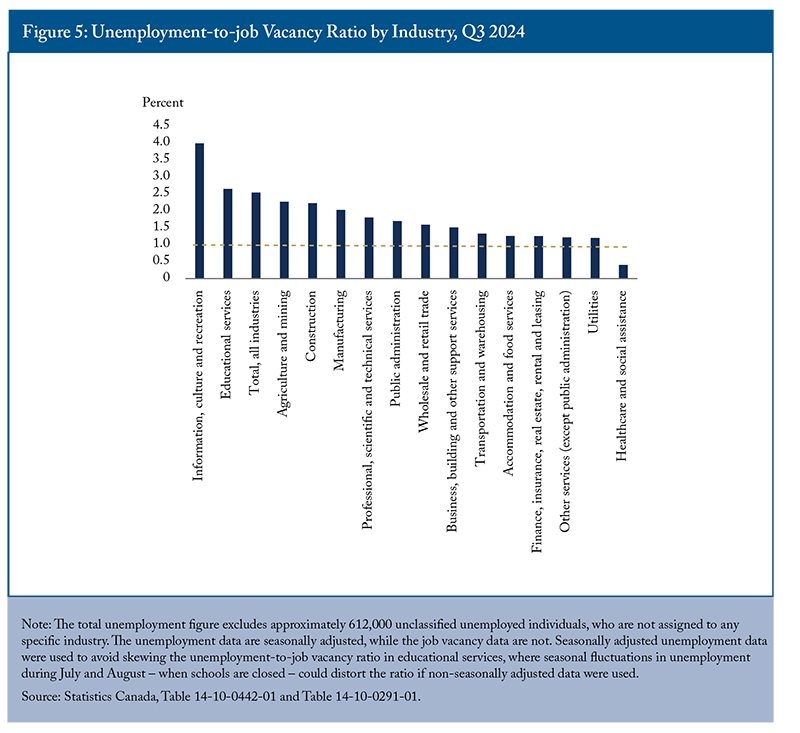

Job vacancies have decreased since mid-2022, but over half a million positions remained unfilled during the third quarter of 2024 (12 percent higher than the pre-pandemic level). Of these vacancies, the majority were full-time (432,810 positions), with more than 31 percent remaining vacant for the long term – persisting for over 90 days. Despite high full-time vacancies, more than half a million workers were underemployed in 2024, seeking full-time work while employed part-time, indicating mismatches between the skills needed by employers and the skills offered by job seekers. Among sectors facing labour shortages, factors such as better relative wages and working conditions appear to be helping, particularly in industries like construction. Healthcare, on the other hand, may benefit from raising wages and reducing training costs to better attract and retain workers.

Further, Canada faces declining labour productivity, which can be attributed to factors such as stagnant capital investment and automation, high reliance on temporary foreign workers to fill low-paying positions, underemployment (including immigrants’ overqualification), a growing public sector with lower productivity, and shifts in industry composition.

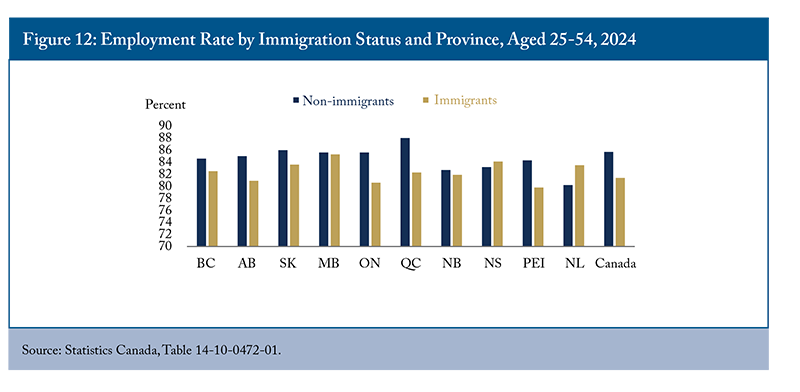

This inaugural C.D. Howe Institute labour market review highlights major differences in the labour market across provinces and sectors and among socio-economic groups. It shows that labour force participation and employment of older workers and recent immigrants still have room for improvement.

Canada needs targeted workforce development policies to improve labour market participation and outcomes for diverse population groups and encourage a longer working life (Holland 2018 and 2019). Our recommendations are to:

Gradually raise the normal retirement age from 65 to 67 and delay pension access.

Support older workers with flexible work, part-time options, and self-employment, especially in the Atlantic provinces.

Invest in high-quality training programs for underrepresented groups, focusing on digital skills and job search strategies.

Streamline credential recognition and licensure for skilled immigrants and ease labour mobility in regulated occupations while maintaining the quality of professional services.

Enhance settlement strategies for immigrants, including workplace-focused language training.

Businesses should integrate automation and artificial intelligence (AI) to boost productivity while improving retention and encouraging later retirement by offering training2 and flexible scheduling (Mahboubi and Zhang 2023).Finally, better informing Canadians about learning and training opportunities and addressing financial and non-financial barriers would improve their training participation rates and empower them to acquire the skills needed in a changing labour market.

Overview of Canada’s Labour Market

Canada’s labour market has undergone major changes over time, influenced by factors such as the COVID-19 pandemic, globalization, technological progress, and demographic shifts. These forces have affected the functioning of the labour market, with demographic changes playing a particularly important role. This section reviews key indicators (i.e., labour-force participation, employment and unemployment) and highlights the major trends and disparities in provincial and national labour markets.

The labour force has grown steadily since 1976 but experienced a decline in 2020 due to the pandemic. The lockdowns and public health measures significantly reduced worker participation, especially among women, in the labour market. However, once the restrictions were lifted, workers returned, and the labour force fully recovered. By 2024, Canada had 22.1 million people in the labour force, an increase of about 1.9 million from 2019, mainly driven by the expansionary immigration policy that the country has followed until recently.3 Immigrants accounted for 56 percent of this increase in the labour force, while non-permanent residents made up 32 percent.4

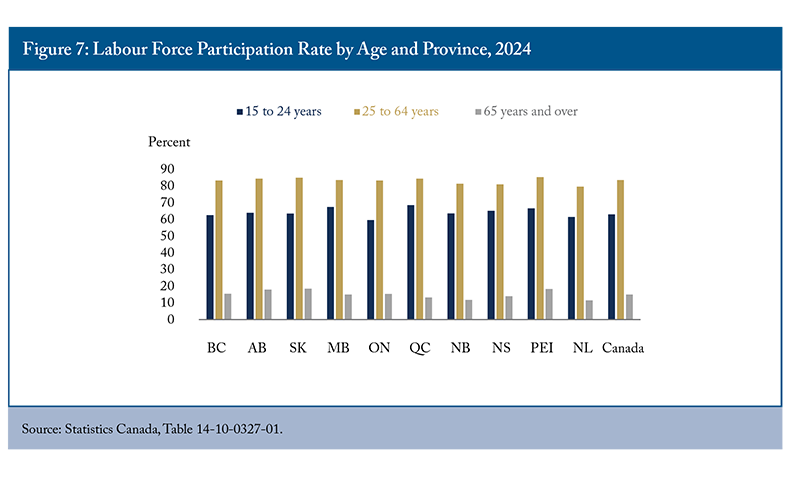

Although the labour force has grown over time, the labour force participation rate (LFPR) has trended downward over the last two decades. This trend is largely driven by an aging population, as participation rates drop sharply after age 54 and continue to decline with age. While the LFPR among prime-aged workers (25-54) reached a record high in 2023, the overall rate remained below pre-pandemic levels and declined further in 2024, reaching 65.5 percent despite high levels of immigration.5 Three factors contributed to this decline compared to pre-pandemic levels: a lower participation rate among youth, a substantial increase in the older population (aged 55 and over) and a decline in the latter group’s participation rate. This decline in older workers’ participation is primarily due to aging, as the proportion of seniors aged 65 and over within the 55-and-over age group increased from 54.8 percent in 2019 to 60 percent in 2024.

The employment rate is more sensitive to economic conditions and fluctuates with cyclical changes in the unemployment rate. It is also influenced by factors such as government policies on education, training, and income support, as well as employers’ investments in skill development and their effectiveness in matching people to jobs. Despite some volatility during economic booms and recessions, the employment rate trended upward until 2008 but has declined since then, mirroring the impact of an aging population on the participation rate (Figure 1). The pandemic caused a sharp decline in the employment rate, followed by a modest recovery. In 2024, the rate, however, declined again by approximately one percentage point to 61.3 percent, as employment growth (1.9 percent) failed to keep pace with the population growth (3 percent).

Regional disparities in employment persist across Canada. Alberta consistently maintains the highest employment rate, while Newfoundland and Labrador lags. Despite significant improvements since 1976, the Atlantic provinces continue to face challenges with employment. For its part, Ontario’s employment rate – historically the second highest in the country – has been below the national average since 2008. Regional differences in economic development, sectoral specialization patterns, educational attainment, family policy, and demographic characteristics are factors behind these employment disparities. For example, Newfoundland and Labrador and New Brunswick had the highest old-age dependency ratios (OADs) in 2024 at 39 and 37 percent, respectively, while Alberta remains the youngest province with an OAD ratio of less than 23 percent.6

The unemployment rate, a key short-term indicator, tends to rise during economic downturns and fall back during recovery, affecting employment outcomes in the opposite direction (Figure 1). The onset of the pandemic in 2020 led to a temporary surge in the unemployment rate to 9.7 percent – a four-percentage point hike from the previous year. As the economy recovered, the unemployment rate plummeted to a record low of 5.3 percent in 2022. However, by 2024, it had risen to 6.3 percent, a figure that remains relatively low by historical standards but higher than the pre-pandemic rate in 2019.

While employment grew by 1.7 million people between 2019 and 2024, the labour force expanded even faster, increasing by 1.9 million people. This imbalance – where the labour force grew more quickly than employment – pushed the unemployment rate higher, reflecting a loosening labour market and making it more challenging for job seekers to secure employment.

Overall, the labour force and employment in Canada have been expanding due to a surge in immigration. Despite unemployment rates remaining higher than the pre-pandemic level, this primarily reflects the exceptional growth in the labour force rather than a lack of job creation. The labour market continues to adjust to the increase in labour supply through strong job creation.

Looking ahead, several uncertainties and factors could influence unemployment rates. For example, the imposition of trade tariffs by the United States poses a direct risk to export-related jobs. In 2024, 8.8 percent of workers – equivalent to 1.8 million people – were employed in industries dependent on US demand for Canadian exports.7 Sectors most vulnerable to these risks include oil and gas extraction, pipeline transportation, and primary metal manufacturing.

On the other hand, stricter immigration policies that limit the inflow of permanent and non-permanent residents may reduce the growth of the labour force, which could, in turn, place downward pressure on the unemployment rate. However, the ongoing arrival of refugees, which contributes to the growing population of non-permanent residents, could lead to higher unemployment rates, particularly if newcomers face significant challenges integrating into the labour market.