This report via our friends at Canadian thinktank C.D. Howe Institute, argues that front-end security screening cannot replace in-person questioning at a hearing.

Accepting Asylum Claims Without Hearings Raises Legal, Security, and Integrity Risks

January, 2026 – Since 2019, the Immigration and Refugee Board of Canada (IRB) has accepted tens of thousands of asylum claims without holding an oral hearing through a paper-based process known as “File Review.” A new report from the C.D. Howe Institute argues that this policy raises serious legal, security, and governance concerns, may exceed the IRB’s authority, and risks undermining core safeguards in Canada’s asylum system.

In “Accepting Asylum Claims Without a Hearing: A Critique of IRB’s ‘File Review’ Policy,” lawyer James Yousif examines how File Review originated as a pilot during the 2017 Yeates Review, when structural reforms, including the possible dissolution of the Refugee Protection Division (RPD), were under consideration. The policy was formally institutionalized in 2019. Introduced as an efficiency measure, the policy allows certain categories of claims – defined by nationality and claim type – to be accepted without questioning claimants or holding a hearing.

Irreplaceable: Oral Interview

The report argues that front-end security screening cannot replace in-person questioning at a hearing, which can reveal inconsistencies, misrepresentation, and inadmissibility concerns that may not be detectable through document review alone.

The report finds that File Review did not achieve its stated objective of reducing the asylum backlog. Despite substantial increases in IRB staffing, resources, and annual decision output between 2016 and 2024, the backlog expanded dramatically from roughly 17,000 claims to nearly 300,000. Over the same period, Canada’s overall asylum acceptance rate rose to approximately 80 percent, roughly double that of peer jurisdictions.

While global migration pressures, post-pandemic travel patterns, and other policy factors contributed to the surge in claims, the report cautions that maintaining a policy that permits rapid acceptance of claims without hearings may reinforce perceptions of speed, success, and reduced scrutiny – potentially increasing Canada’s attractiveness as an asylum destination.

So Called ‘Soft Law’ Was Used To Implement Policy

The report notes that File Review was implemented by the IRB unilaterally using a Chairperson’s Instruction, a form of internal “soft law” typically used for tribunal operations, not for system-wide policy change. The report also raises concerns about adjudicative independence. It argues that File Review may improperly fetter the discretion of RPD adjudicators, delegate aspects of fact-finding functions to non-adjudicative staff, and impose a mandatory internal consultation process. These features, the report suggests, may be inconsistent with established principles of administrative law.

The report concludes that the File Review policy should be brought to an end and that the default requirement of oral hearings should be restored. While this would likely reduce short-term decision volumes, the author argues that a more rigorous adjudicative process would strengthen long-term system integrity, better protect genuine refugees, and help restore public confidence.

“Efficiency gains that rely on shortcuts may prove illusory,” says Yousif. “A policy that prioritizes speed over scrutiny risks reinforcing the very pressures it is meant to relieve.”

December, 2025 – Trade tensions, regulation and growth-stifling taxes are depressing business investment in Canada, undercutting productivity growth and workers’ incomes, according to a new C.D. Howe Institute report. The report notes that the US is far more robust, hurting Canadian competitiveness and threatening to widen the gap between US and Canadian living standards.

.William B.P. Robson and Mawakina Bafale warn that (read below) a decade-long decline in capital per member of Canada’s labour force is putting Canada on a path toward a more labour-intensive, lower-wage economy. The authors urge policymakers to equip Canadian workers with the tools they need to compete and thrive.

Canada stuck in a vicious cycle

“Canada is stuck in a vicious cycle. We need higher productivity to spur capital investment – but we need higher capital investment to spur productivity,” says Robson, President and CEO of the C.D. Howe Institute. “Canadian workers today effectively have less and older capital to work with than they did a decade ago. We need to address this crisis by fixing growth-stifling regulations and taxes.”

Looking globally, the picture is even more concerning. Many OECD peers, and most notably the United States, have increased their investment levels more strongly than Canada, widening longstanding gaps. For example, in 2024, Canadian workers received 41 cents of machinery and equipment investment for every dollar received by US workers. The pattern is similar in intellectual property, where Canadian workers received just 32 cents for every US dollar of investment. These gaps translate directly into differences in productivity and wages, and they affect Canada’s ability to attract and retain talent.

Robson and Bafale identify several factors behind Canada’s weak investment performance: a long-standing tilt toward residential construction; regulatory delays for major projects; tax structures that discourage scaling up; elevated government consumption crowding out private investment; and growing policy and trade uncertainty. Rising US protectionism and the upcoming 2026 CUSMA review add an additional layer of risk for Canadian businesses assessing long-term investments.

To reverse the decline, the authors call for streamlined regulations, more competitive tax policies, stronger innovation support, a clearer path for energy investment, and a more assertive trade strategy.

“We need a renewed focus on growth and investment,” says Bafale, Research Officer for the C.D. Howe Institute. “Without faster, clearer rules and stronger incentives for businesses and workers, Canada will continue to fall behind its international peers.”

Business investment in Canada has been so weak since 2015 that capital per member of the workforce is falling, undermining growth in labour productivity and compensation.

The longstanding gap between investment per available worker in Canada and other OECD countries narrowed from the late 1990s through the early 2010s, but has since widened, especially relative to the United States. In 2025, Canadian workers will likely receive only 70 cents of new capital for every dollar received by their counterparts in the OECD as a whole and 55 cents for every dollar received by US workers.

Labour productivity and business investment go together. Rising productivity creates opportunities and competitive pressures that spur businesses to invest. Investment increases productivity by equipping workers with better tools. Low investment per worker signals that businesses see fewer opportunities in Canada and prefigures lagging growth in earnings and living standards.

Regulatory and fiscal policy changes, particularly those affecting natural resources and investment-related taxes, can prevent Canadian workers from being relegated to lower value-added activities compared to their counterparts in the United States and other advanced economies.

Introduction and Overview

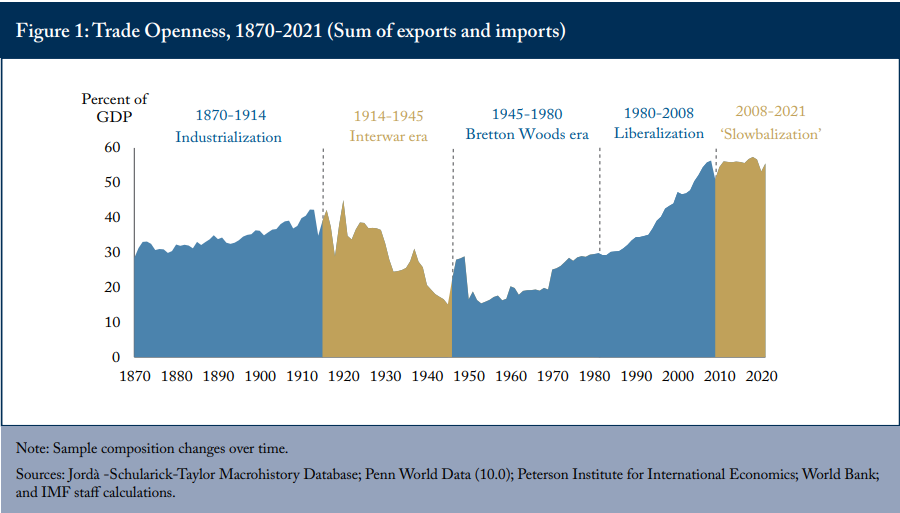

Slow growth in Canadian productivity and living standards has become a top-of-mind concern for Canadian economy watchers and, increasingly, for Canadians themselves. Recent publications highlight Canada’s declining real gross domestic product (GDP) per person and its ominous implications for future living standards (Porter 2024, Marion and Ducharme 2024, McCormack and Wang 2024). Escalating trade tensions between the United States and Canada have led many firms to delay investment decisions (Bank of Canada 2025). Sluggish productivity growth has been a key factor behind Canada’s stagnant living standards, as the Organisation for Economic Co-operation and Development (OECD) recently highlighted in its Economic Survey of Canada (OECD 2025a).

The OECD predicts that the real GDP per capita in Canada will fall for the third consecutive year in 2025. This slide is a troubling break from Canada’s historical pattern of rising living standards. It contrasts with what is happening in other OECD countries, which have overtaken Canada, and contrasts especially strongly with the United States (Figure 1). Declining output per person implies that Canada is becoming a less attractive place for talented people to live and work.

Many influences on GDP per person may not be easily or desirably influenced by policy.

More people participating in the workforce and/or working longer hours will raise output per person, but more work per person has obvious costs. Higher human capital – enhanced skills and more education – and improved technology can raise output per person, but building human capital takes time, and improved technology is not, on its own, something policymakers can directly engineer. Increasing the amount of capital per worker, by contrast, is relatively straightforward to achieve and has positive results that are relatively likely to occur.

High or low levels of business capital, such as non-residential structures, machinery and equipment, and intellectual property products, are strongly associated with higher or lower output per worker. Productivity gains spur investment, and investment in turn boosts productivity. Higher productivity creates opportunities and competitive threats that promote business investment. In turn, higher business investment gives workers newer and better tools, embodies new technologies and gives managers and workers new opportunities to “learn by doing” – all of which raise each worker’s productivity.1

These links between investment and labour productivity make recent figures on Canada’s capital stock and new investment worrying. Canada’s capital stock in the business sector has grown so little since 2015 that capital per member of Canada’s labour force has been falling. Clearly, the recent extraordinary growth in Canada’s labour force, driven by permanent and temporary immigration, has not prompted businesses to provide tools to augment the productivity of the newly available brains and hands.

The spectacle of falling capital per worker forces attention to the fact that capital and labour are not only complementary factors of production – they are also substitutes. Industries and production methods vary in how intensively they use capital relative to labour. In international trade, countries with higher capital per worker tend to specialize in capital-intensive goods and services, while countries with lower capital per worker gravitate toward labour-intensive ones. Since living standards are higher in capital-intensive countries, Canada must confront the risk that low business investment and fast workforce growth are leading Canada down a labour-intensive path.

The United States and other OECD countries are investing at higher rates. Business investment per available Canadian worker was closing in on US and OECD levels from the early 2000s to the middle of the last decade, but the convergence stopped around 2015. Canada’s relative performance then plummeted during the COVID pandemic and has lagged badly since.

Canada’s workers need better tools to thrive and compete. Governments must change policies that are taking Canada’s economy down a more labour intensive, lower-wage path.

The Numbers

Many types of capital enhance productivity and living standards. Our focus in this report is on “reproducible” or “built” capital in the business sector. Human capital and natural capital, such as skills, land and water matter, but they cannot be reliably measured or compared internationally. Capital created and owned by governments also matters, but the services it yields are harder to relate to production and income.

Measures of built capital are relatively robust and easier to compare internationally. Non-residential buildings include offices, warehouses and industrial facilities, as well as engineering structures such as transportation infrastructure. Machinery and equipment (M&E) includes motor vehicles, tools and electronic equipment. Intellectual property (IP) products have three major sub-components (see Box 1). These types of built capital complement other types of capital – human, natural and government – in producing goods and services, generating incomes and helping workers compete internationally.

Labour force measures are also relatively robust and normally easy to compare internationally.2 However, the surge in temporary residents in Canada in recent years has coincided with a growing discrepancy between the number of temporary foreign workers reported by Immigration, Refugees and Citizenship Canada (IRCC) and the number of temporary residents reported in Statistics Canada’s Labour Force Survey (LFS), the most widely used source of data on the workforce and the one relied on by the OECD. Skuterud (2025) shows that IRCC’s count exceeded the LFS figure by 1.3 million in 2024. In translating Statistics Canada’s labour-force count to our measure of available workers, we multiply the labour-force figures since the first quarter of 2022 by the ratio of the populations in Statistics Canada tables 17-10-0009-01 and 14-10-0287-01. This adjustment adds 272,000 more available workers on average to the LFS numbers since the first quarter of 2022.

Notwithstanding variations in the efficiency with which various countries combine labour and business capital to produce output – variations arising from other inputs and influences such as organization of firms, often grouped under the term “multifactor productivity” – countries with high capital stocks tend to enjoy high output. Labour productivity growth and investment interact. Anticipated higher productivity creates opportunities for growth and profit for businesses, as well as threats from innovative competitors and losses. Those opportunities and threats incent investment, which increases the quantity and quality of the capital stock. A larger, newer capital stock raises productivity and workers’ incomes. The correlation between capital stock per member of the labour force (adjusted for undercount in Canada’s case) – for which we use the term “available worker” – and output per available worker across countries is clear (Figure 2).3

The fact that capital formation is both a result of productivity growth and a driver of it makes recent trends in Canada’s capital stock troubling. Figure 3 shows real stocks of each type of capital per available worker.

Total non-residential capital per available worker in Canada peaked in the last quarter of 2015.4 By the third quarter of 2025, per-worker levels of all types of capital were well below the late 2015 benchmark. IP products per available worker were down 4 percent. Engineering construction was down 6 percent. Non-residential buildings were down 12 percent. M&E was down a dramatic 20 percent. The dismal summary: the latest figures show the average member of Canada’s labour force had 9 percent less capital to work with than in 2015.

Because we do not have comparable time-series of capital stocks for many other countries, we turn to a closely related flow measure – gross business non-residential investment – to set up an international comparison over time. Figure 4 shows the Canadian numbers for the three types of business investment – non-residential structures (buildings and engineering), M&E and IP products – per available worker since 1990.

Absent major changes in estimated depreciation and write-offs, changes in gross investment should closely track changes in net capital stock. From 1990 to 2014, notwithstanding setbacks during the slump of the early 1990s and the 2008-2009 financial crisis and recession, the trend in investment per worker was up. But during the second half of the 2010s, investment in structures and M&E per member of the workforce declined, and investment in IP products flatlined. The economic shutdowns and uncertainty around the COVID-19 pandemic hurt business investment in everything except IP products.

Since then, performance in all three categories has been lacklustre. Adjusted per-available-worker investment in the third quarter of 2025 was only about $15,000 in 2024 dollars – down almost one quarter from its 2014 peak of $19,400.

Predictably, low levels of new investment have coincided with ageing of the capital stock and a decrease in the average remaining productive lives of assets.5 When new investment exceeds depreciation and scrapping, the remaining useful life of assets tends to rise, as it did in most categories before 2015. When new investment falls short of depreciation and scrapping, the remaining useful life of assets declines, as it has since then. In 2024, the remaining useful life ratio of non-residential buildings was 1 percent below its 2015 peak, whereas the ratios for IP and engineering construction were 13 and 7 percent lower than their 2015 benchmarks, respectively. An exception is machinery and equipment, where a shift in spending toward longer-lived assets such as transportation equipment has offset weak gross spending. Overall, the remaining useful life ratio of non-residential capital in 2024 was 4 percent below its 2015 peak. This trend highlights the need for increased investment to maintain Canada’s productive capacity as its capital stock ages and becomes obsolete.

Canada’s Investment Performance in International Perspective

Many factors that affect business investment in Canada also affect other developed countries. Over the long term, the growing importance of intangible assets beyond those measured in IP products, such as organizational efficiency, and services that escape traditional measures of value-added, such as internet search engines, may make lower levels of traditional business investment consistent with rising living standards everywhere. Short-term influences such as the pandemic and trade uncertainty also affect many countries. We can check Canada’s experience against that of the United States and other OECD countries with comparable data (the same countries that appear in Figure 2). Is Canada’s apparent path toward lower capital intensity part of a broader and possibly benign global pattern, or is Canada on a unique path that raises unique concerns?

Canada versus the United States

Canada and the United States collect similar capital investment data, and Statistics Canada takes particular care to compare Canadian to US prices. We can therefore measure investment per available worker in the two countries with some confidence that we are getting meaningful comparisons.

We convert the different types of capital investment into Canadian dollars using Statistics Canada’s measures of relative capital-equipment price levels to adjust for purchasing power differences.6 This approach gives a clearer sense of the “bang per buck” spent on structures, M&E or IP products on either side of the border. The results of these calculations appear in Figure 6, panels A through D.

Canada has a longstanding edge in investment in structures (panel A), reflecting the importance of non-residential buildings and engineering structures in natural resource industries. This gap was particularly wide in 2014, at almost $4,000 per worker, when Canadian investment in natural resources, notably oil and gas production and transmission, was booming. Since then, it has shrunk – to less than $500 in 2024.

The picture for M&E investment (panel B) is markedly different. The United States has always invested more heavily in M&E, and that advantage has grown over the past 15 years. Recently, US M&E investment per available worker has been almost three times higher than in Canada – about $11,000 annually in the US compared to $4,600 in Canada. Given the potentially outsized importance of M&E investment for productivity growth (Sala-i-Martin 2001, Rao et al. 2003, Stewart and Atkinson 2013), this gap bodes poorly for the competitiveness of Canadian workers and for Canada’s attractiveness as a place to live and work.

The IP products gap (panel C) is worse yet. In 2024, the Canadian figure stood at about $3,300, up from about $2,600 in 2014, while the US figure stood at $10,600, up from $7,000 in 2014. Part of this gap reflects slumping exploration expenditures and their associated IP by Canada’s struggling resource sector. In general, Canadian firms tend to use IP products owned abroad more than US firms do, which reflects in part Canada’s relative lack of success in commercializing domestic intellectual property.

Looking at all three categories combined (panel D), the United States has outpaced Canada since the 1990s. The gap narrowed in the 2000s but widened markedly after the mid-2010s and expanded further after the pandemic, reaching $13,300 per potential worker in 2024. That is a chasm. Differences in investment per worker on that scale could represent a significant shortening of the replacement and upgrade cycle for equipment such as trucks, excavators, machine tools, workplace equipment, and the potential replacement of entire information and communications technology systems – meaning US workers benefit from more modern tools and higher productivity.

One way to summarize these differences is to ask how many cents of new investment per available Canadian worker occur for every dollar of new investment per available US worker. Figure 7 presents our measure of investment in Canada per dollar of its US equivalent in total and in each investment category.

Canada’s relatively robust rate of structures investment stands out in Figure 7. The surge in the early 2010s is striking: in 2013, each available Canadian worker was getting $1.63 for every dollar received by a US worker. The subsequent decline is just as striking. By 2024, the average member of the Canadian workforce received $1.05 of new non-residential structures for every dollar received by the average member of the US workforce.

As the comparison in Figure 6 suggests, the contrast is worse for M&E. After improving from just 50 cents around the turn of the century to nearly 70 cents around the time of the 2008-2009 financial crisis and slump, Canada’s relative performance has deteriorated. In 2015, M&E investment for every available Canadian worker per dollar enjoyed by a US worker stood at 47 cents for every US dollar. By 2024, it had dropped to a dismal 41 cents – a number that has fallen further since (Robson and Bafale 2025).

The situation with IP products is worse yet. A declining trend since the mid-2000s has led to the point where the average member of the Canadian workforce in 2024 enjoyed only 32 cents of new investment in IP products for every dollar enjoyed by their US counterpart. The measurement of IP products in the two countries is not identical (Box 1), but focusing on the comparable categories reveals that US investment per worker in software is about double Canadian investment per worker, and that US investment in R&D is about four times Canadian investment.

Canada versus the OECD

Widening the international comparison to other OECD countries offers more perspective on Canada’s situation.7 This broader and more forward-looking view comes with caveats. Not all OECD countries break down business investment by type the same way Canada and the United States do, and some measures, notably IP products, differ across countries. Therefore, we use aggregate investment with less confidence that we are comparing like with like. We also do not have current measures of relative prices for different types of investment. We resort to a less precise “bang-per-buck” adjustment: purchasing-power-adjusted exchange rates benchmarked to relative prices of capital investment goods and services in 2017.

For consistency, we use the same OECD measures for the United States as well, which means that the per-available-worker numbers in Canadian dollars are not identical to those in our Canada-US comparison. But the big picture – notably, the story of Canadian underperformance – is consistent (Figure 8).8

Investment per available worker in the other OECD countries with comparable data has typically been less robust than in the United States but more robust than in Canada. This tendency was less pronounced in the early 2010s, when Canada’s resources sector was booming and many other advanced economies were suffering the lingering effects of the 2008-2009 financial crisis and slump. At that point, the gap between investment per Canadian labour-force member and those in other OECD countries (excluding the United States) narrowed, and the two measures were almost equal in 2014.

Since then, the gap has widened again. The OECD’s projections for 2025 yield a figure of about $19,300 of new capital per available worker this year for the other OECD countries, compared with just $15,800 for Canada. In other words, the OECD’s projections for countries other than Canada and the United States indicate that gross new capital per available worker in Canada will be about 20 percent less than in those countries this year.

Figure 9 highlights this relative performance by showing Canadian investment per worker for each dollar invested elsewhere. The figure shows how much new capital each available worker in Canada enjoyed per dollar of new capital per available worker in the United States, the OECD as a whole and in the other OECD countries since 1991, along with the figures calculated from the OECD’s 2025 projections.

For every dollar of investment received by the average worker across the OECD as a whole, the average Canadian worker enjoyed about 75 cents in the early 2000s. Excluding the United States, Canadian workers enjoyed 79 cents. By 2014, this gap had narrowed: the average Canadian worker was enjoying some 89 cents of new investment for every dollar invested per worker in the OECD overall, and 97 cents relative to workers in other OECD countries. By 2025, however, Canadian workers will likely enjoy only about 70 cents of new capital for every dollar enjoyed by their OECD counterparts. The figure compared to workers in OECD countries other than the US is 82 cents. The figure compared to US workers is a dismal 55 cents.

Canada’s Productivity Performance in International Perspective

Higher investment is not a goal in itself. Subsidies and regulations that spur investment in uneconomic assets could raise capital spending but lower productivity and future incomes.9 Our concern about these numbers is their implication that Canadian businesses either do not see opportunities and competitive threats that would prompt them to undertake productivity-improving capital projects, or that when they see such opportunities and threats they respond slowly or incompletely. To that extent, these numbers presage trouble for Canadian workers.

As the relationship in Figure 2 illustrates, and as previous research such as Rao et al. (2003) has noted, countries with higher capital intensity tend to have higher productivity and higher wages. Likewise, countries with lower capital intensity tend to lag on both fronts. Unless human capital per worker is rising and/or multifactor productivity is rising fast enough to offset it, falling built-capital per worker means less output generated per hour worked.

In the 1990s, the US economy produced $27,000 more per available worker than Canada, and the gap has widened since. In the 2000s and 2010s, Canadian output per available worker averaged $128,000 and $136,000, respectively, compared with $164,000 and $184,000 in the United States. By 2024, Canada generated $143,000 per available worker, compared to almost $200,000 in the United States (Figure 10).

Canada generated more output per worker than in other OECD countries in the 1990s, but that advantage has disappeared. Specifically, in the 1990s, Canadian workers produced $3,000 more per worker than their counterparts in other OECD countries. By 2024, notwithstanding a productivity decline post-COVID, workers in other OECD countries were generating $10,000 more per worker than those in Canada.

As with investment per available worker, we can highlight Canada’s relative performance by showing Canadian output per available worker for each dollar of output generated per available worker elsewhere (Figure 11).

In the 1990s, Canadian workers produced 80 cents for every dollar of output generated by US workers. By the 2010s, the ratio was around 74 cents, and by 2024, it had fallen further to 72 cents. In the 1990s, Canada generated $1.03 per worker for every dollar generated per worker in other OECD countries. By 2024, this figure had dropped to 93 cents.

Diagnoses and Possible Responses

What lies behind these ominous numbers and how might Canadian governments respond? Causation flows both ways between labour productivity and investment, but an investigation can usefully start by asking why Canadian businesses may not respond to opportunities and threats as much as they did previously or compared to businesses in other countries. We explore that question in the next subsection, and then ask why Canadian businesses might see fewer opportunities and threats than before and fewer than those in other developed countries.10

Why Might Canadian Businesses Respond Less to Opportunities and Threats?

Do Canadian businesses have some structural predisposition against innovation, entrepreneurship, investment and productivity growth? Porter (2023) provides a list of commonly blamed factors, including low population density, a cold climate, reliance on resource-sector revenues, weak private-sector research and development efforts and interprovincial barriers. As Porter points out, however, other countries with similar characteristics are outperforming Canada. Moreover, factors that have remained unchanged for decades cannot fully explain Canada’s poor performance since the mid-2010s, unless their impact has intensified. What, then, might have changed?

One possible factor is Canada’s bias toward residential construction.11

The federal government backs mortgage lending through Canada Mortgage and Housing Corporation (CMHC) insurance, likely leading lenders to favour residential over non-residential investments (Omran and Kronick 2019). Although mortgage lending has exceeded business lending in Canada since the mid-1980s, a tougher environment for non-residential investment and higher immigration since the mid-2010s may have made residential investment even more attractive. While imports can augment the resources available for capital investment in a given year, domestic output over time limits the total amounts available for consumption and investment of all kinds. As a result, a growing share of residential investment in GDP could limit the responsiveness of non-residential investment to opportunities and threats.

Another clearly negative influence has been the hostile regulatory environment for Canada’s fossil fuel industry since 2015.12

While global investment in oil and natural gas dropped when prices weakened in 2014, the subsequent recovery spurred a much stronger response in the United States than in Canada. Oil and gas investment per worker in Canada has fallen relative to the US, indicating a muted response to strong demand and high prices on the Canadian side of the border. A hint about the importance of the regulatory environment in the Canadian data is the relatively robust performance of investment in conventional oil production in Canada, which has followed a path more similar to that of the US industry. In contrast, investment in oil sands projects, which involve larger commitments of capital for longer periods, has been more subdued.

Porter’s list of suspects also includes the small scale of many Canadian businesses. The widening gaps between the effective tax rate on small businesses and both the general corporate income tax rate and personal income tax rates, combined with generally low interest rates, might have dulled business response to incentives that could have otherwise spurred investment and growth. The wider the gap between the small business tax rate and other rates, the stronger the incentive to keep earnings and assets below the thresholds at which the small business rate phases out, increasing marginal tax rates over that range. This creates distortions (OECD 2025a) and a “lock-in’’ effect, where businesses are incentivized to reinvest earnings within even mediocre firms rather than taking them as personal income. This incentive varies with the return on assets: the lower the rate of return, the larger the marginal effective rate on earnings in the clawback zone.

Dachis and Lester (2015) argue that providing preferential tax treatment to small businesses steers capital from larger, more productive firms to smaller, less productive ones. Since 2009, the gap between effective small business tax rates and ordinary corporate and higher-income personal tax rates has widened, and is wider in Canada than in other G7 countries. Against a backdrop of generally lower returns on assets, this widening gap might help explain relatively lower business investment in Canada in recent years.

The US tax reforms of 2017 likely lowered investment in Canada and certainly did so relative to the United States. Prior to 2017, Canada had improved its tax treatment of investment relative to the United States, with reforms from the late 1980s to the early 2010s reducing the federal general corporate income tax rate from nearly 38 percent to 15 percent and reducing the aggregate marginal effective tax rate on investment in Canada (Chen and Mintz 2015, Bazel and Mintz 2021). These steps strengthened Canada’s investment performance and capital stock (Wen and Yilmaz 2020). As noted already, Canada’s investment performance relative to the US and other OECD countries did improve from the early 1990s until 2014, when the slump documented in this report began.

Those 2017 US reforms, notably the reduction of the federal corporate income tax rate from 35 to 21 percent and faster write-offs for M&E, undid Canada’s business tax advantage (Bazel and Mintz 2021, McKenzie and Smart 2019). As intended, the US reforms lowered the marginal effective tax rate on business investment. Bazel and Mintz (2021) calculate the average US federal and state effective marginal rate at less than 26 percent in 2019, down from nearly 40 percent in 2000. By contrast, the average Canadian federal and provincial/territorial rate was above 26 percent, down much less from nearly 30 percent in 2000.

Chodorow-Reich et al. (2023) compare investment by US-based companies to investment by similar companies abroad, including those in Canada, around the time of the reforms and find a stronger investment performance among the US group, post-reforms. Crawford and Markarian (2024) similarly show that the reforms reversed Canada’s previous tax advantage. They find that US companies significantly increased their capital spending compared to Canadian firms after the reforms.

The US tax reforms also aimed to encourage US-based multinationals to repatriate profits held abroad. Although success in that respect would likely depress capital formation in Canada (Mathur and Kallen 2017, McKenzie and Smart 2019), that result is not guaranteed. Foreign investments can complement domestic investments, and the immediate post-reform US global intangible low-tax income (GILTI) regime applied only to foreign income above 10 percent of foreign tangible capital, which created an offsetting incentive for businesses to invest abroad. However, matched-firm analyses by Chodorow-Reich et al. (2023) found weaker investment among Canadian firms than among US firms following the reforms, and Crawford and Markarian (2024) conclude that the surge in US investment was driven primarily by domestic activity.

A notable trend since 2017 is the decline in Canadian M&E investment per worker relative to the United States, despite Canada responding to the US reforms by introducing accelerated depreciation on almost all capital assets in 2018. This suggests that some of the robust US domestic investment might have come at Canada’s expense or that other factors made Canadian companies’ investment weaker than that of their US counterparts.

The GILTI regime also addressed previous incentives for US multinationals to hold and commercialize IP products abroad (Singh and Mathur 2019). Since the 2017 reforms, Canada’s performance in IP investment relative to the US has been worse than its performance in other asset types. The GILTI rules imposed such a significant tax burden that many IP investments yielded higher after-tax returns in the US than overseas. This reduced the tax advantage of locating intangible assets outside the US. While this does not prove causation, it strongly suggests that the US reforms have played a significant role.13

Why Might Canadian Businesses See Fewer Opportunities and Threats?

A regular critique of Canadian business, also noted by Porter (2023), is a lack of entrepreneurial drive and risk tolerance. These traits may have become more problematic with the rise of information and communication technology, which rewards countries with stronger human capital in these areas. This could explain Canada’s recent poorer showing against the United States.

Another reason for Canadian businesses revising their investment-spurring expectations down, at least relative to US firms, is increased population growth since the mid-2010s.14 This surge reflects higher immigration, shifted toward students and temporary foreign workers, and lower economic stream thresholds. This may have led businesses to favour labour substitution over capital investment (Doyle et al. 2024).

The rising share of government consumption may also mean fewer opportunities for Canadian businesses.15 Government consumption – spending on public employees and other resources – draws directly on the same resources as the private sector. It is expected to rise during downturns, such as the early 1990s, the 2008 financial crisis, the 2014 oil-price collapse, and the pandemic, while business investment – which is strongly affected by economic cycles – falls. But if government consumption remains elevated as the economy strengthens, it can crowd out private spending, including business investment. Canada’s post-pandemic experience is concerning because government consumption has continued to rise while business investment has struggled (Figure 12). Although recent slack in the Canadian economy might appear to reduce the potential for government consumption to crowd out other uses of resources, the sluggish growth in productive capacity prefigured by current feeble investment suggests that competition for resources by government will remain a problem if governments do not reduce their claims on the economy.

Another factor behind Canada’s lower investment rates is US protectionism. Donald Trump’s recent trade policies are exacerbating a problem with many roots. Secure access to the US market has long been a goal of Canadian trade policy, ensuring that Canada remains an attractive production base. Even before Donald Trump’s 2017 inauguration, the 2016 campaign featured anti-NAFTA rhetoric from both parties, potentially discouraging Canadian investment. The 2024 campaign prefigured more protectionism, which hammered Canada’s exports of goods to the United States after his inauguration, down 22 percent between January and August 2025.

Domestic policy uncertainty may also have reduced business dynamism, slowing productivity growth and blunting competition that spurs investment. Key sectors – such as energy, plastics, financial services and telecommunications – have faced restrictive regulations, reducing innovation, competition and investment across the economy. Cette et al. (2025) provide evidence that phasing out restrictive regulations in these key upstream sectors could significantly boost productivity and investment.

The OECD’s Product Market Regulation (PRM) project quantifies regulatory burdens by comparing national regulations to international best practices (OECD 2024). The latest PRM data compare 2023 to 2018. In 2018, Canada scored 1.43, slightly better than the OECD average of 1.46 (lower scores indicate less distortion), but worse than the 0.8 average of top performers. By 2023, Canada improved to 1.38, yet lagged behind the OECD average (1.30) and top performers (0.67). Problem areas include licensing, foreign direct investment barriers, public procurement, and governance of state-owned enterprises (OECD 2024).

Furthermore, indexes of policy uncertainty rose far more in Canada after 2014 than in the United States, Europe and even globally (Figure 13).16 While trade tensions have boosted the Canadian index, other policies that undermine business confidence are more directly under the control of Canadian policymakers. Eliminating internal trade barriers and phasing out supply management in dairy, eggs and poultry would reduce these distortions, lowering prices for consumers and costs for businesses that use the affected products as inputs.

What tax-related influences might account for slower productivity growth in Canada and the reduced perception by Canadian businesses of investment opportunities and threats?

One influence is the increased distortion from varying marginal effective tax rates across industries and capital types. Bazel and Mintz (2021) find inter-industry and inter-asset dispersion in marginal effective tax rates more than doubled from 2016 to 2020. Manufacturing investments faced a 13.7 percent average rate – negative in Atlantic Canada due to tax credits – while communications investments faced an average rate of 22.1. Such disparities reduce overall capital productivity.

Labour mobility and personal income tax salience have grown. Post-pandemic remote work enabled more Canadians to work abroad, and emigration data – though incomplete and affected by a methodology change17 – show increased churn since 2015.18 Remote work may have increased opportunities for higher-earning Canadians to work abroad.19 The associated loss of high-skilled workers may reduce incentives for domestic capital investment.

Populist tax policies further undermine investment confidence. The “Canada Recovery Dividend,” imposed on the largest banks and insurers post-COVID, and higher corporate tax rates on large financial institutions introduced in the 2022 budget, lacked economic rationale (Kronick and Robson 2023). The 2021 luxury tax was based on a similar logic (Halpern-Shavin and Balkos 2023). The abortive move to increase capital gains tax rates in 2024 badly shook entrepreneurial confidence. Like policy uncertainty, perceptions of capricious tax policy reduce the dynamism that could otherwise spur consumer-friendly investment.

Potential Responses

The list of likely negative influences on investment in Canada that may have worsened since 2014 is long, and the list of potential policy responses is nearly as long. Some issues are easier to address in the short run than others.20

The bias toward residential construction is difficult to tackle. Slowing the inflow of permanent and temporary immigrants, whose rapid growth has intensified housing market pressure, would reduce the draw of residential investment on resources otherwise available for non-residential capital investment and lessen any disincentive created by abundant low-skilled labour (Doyle et al. 2024). But the government’s announcements have so far not moved the actual numbers much (C.D. Howe Institute 2025).

Current plans to cut business immigration and shift away from human-capital-based selection toward filling in-demand occupations risk undermining Canada’s ability to attract high-skill workers (Mahboubi 2025). Prioritizing lower-skill positions does little to encourage the high-skilled labour that complements business investment.

By contrast, the hostile regulatory environment for Canada’s fossil fuel industry is easier to fix. The case for Canada to suppress its fossil fuel production to lead global emissions reduction has never been convincing. Global energy demand continues rising, fossil fuels supply most of the world’s energy, and Canadian fossil fuels are economically, strategically and environmentally preferable to most others. The federal government’s recent announcements about easing impediments to expanded production and exports are promising; if followed by action, they could boost capital investment measurably in the years to come.

The materialization of US protectionism demands a proactive and strategic defence of Canada’s trade interests, mirroring the diplomatic intensity seen during the 1988 Canada-US Free Trade Agreement and the evolution of NAFTA into the Canada-US-Mexico Agreement (CUSMA). As the 2026 CUSMA review approaches, Ottawa must calibrate trade concessions and complementary initiatives – such as boosting Canadian defence capabilities – and reinforce the mutual benefits of North American economic integration to US businesses, consumers and policymakers. Canada must also reduce its trade exposure to the US by diversifying trade via agreements with the UK and the Association of Southeast Asian Nations (ASEAN), accelerating high-impact energy and mineral projects, investing in trade infrastructure, and working with provinces to lower internal trade and labour mobility barriers.

Reducing policy uncertainty requires clearer processes and criteria. Businesses need stable rules and predictable outcomes. The federal government needs more rigorous ex post evaluations of regulations (OECD 2025b). At present, it often misses critical insights from the real-world evidence on whether rules work as intended. The federal government’s recent initiatives to accelerate approvals for major projects may help, and a national infrastructure plan sounds good, but specific initiatives such as privatizing federal airports are too few and far off to make a difference.

Addressing the bevy of negative tax-related distortions is required. These include the gap between effective tax rates on small and large businesses; the lower effective tax rate on investment in the post-2017 United States; uneven tax rates across regions, sectors and assets (exacerbated by the November 2025 budget’s faster write-offs for selected machinery and processing equipment only); and Canada’s high personal income tax rates all point to the need for comprehensive, long-overdue tax reform. Options include adopting an allowance for corporate equity (Milligan 2014; Boadway and Tremblay 2016), shifting to a cash-flow tax base (McKenzie and Smart 2019) or taxing only distributed profits (Mintz 2022) could foster more investment and higher productivity. To stimulate innovation, Scientific Research and Experimental Development (SR&ED) incentives should better support large firms, link post-secondary research funding to commercialization plans and reorient the Industrial Research Assistance Program (IRAP) toward commercialization (Lester 2025). Eliminating capital gains tax on Canadian small and medium-sized enterprise (SME) shares would incentivize domestic scale-up. A review of small business supports is also needed to ensure they do not entrench low-productivity firms.

Near-term reforms may need to be less ambitious. Consensus on Canada’s tax system flaws and solutions is weaker than in the United States before its 2017 reforms.21 Major tax reforms are easier when they reduce revenue, but most senior governments in Canada are wary of forgoing revenue at that scale. The most promising near-term responses may be simple reductions in the most distorting tax rates – a lower general corporate income tax rate and lower top personal rates.

Though politically challenging, such cuts are easy to legislate, and evidence suggests the relevant tax bases are elastic enough to limit revenue loss.22 Lower top rates do not fix all tax system flaws that blunt business responses to opportunities, but they are uniquely broad in reducing distortions that suppress investment and productivity.

Another near-term option to jolt Canada out of a low-investment, low-productivity trap is a temporary general investment tax credit. Though more complex to legislate and administer than a tax rate cut, a general investment tax credit (ITC) is a familiar tool with predictable effects. Ideally, it would replace the Atlantic Investment Tax Credit and pre-empt other sector-specific ITCs like the Clean Technology Manufacturing Investment Tax Credit. However, a meaningful general credit – say 5 percent – would entail major short-run revenue costs.

Applying a lower tax rate to business income from IP products would directly address Canada’s lagging performance in this sector. The term “patent boxes” is too narrow: applying the lower rate to income from IP embedded in other goods and services would better incentivize broader IP investment and align with emerging international norms than a lower rate on income from patents alone. The federal government could offset near-term revenue costs by reducing R&D subsidies for small firms, which likely promote too much low-quality, non-commercializable work (Lester 2022).

Beyond changing the tone of tax policy, the federal government must change its fiscal stance. It should rein in regular program spending and subsidies delivered through the tax system, which are disguised spending that raise borrowing costs and interest payments. Even after pandemic-related measures wound down, projections in successive fall economic statements and the November 2025 budget have shown projected federal spending rising sharply (Robson 2025).

Call to Action

Ongoing economic uncertainty continues to plague Canadian firms, which, according to the Bank of Canada’s latest Business Outlook Survey, report weak investment intentions and limited expansion plans (Bank of Canada 2025). This backdrop increases the urgency for policy changes that can reverse Canada’s unprecedented, prolonged decline in capital per worker.

The risk that Canadian workers will become increasingly concentrated in lower-value activities relative to their US and international peers should prompt Canadian policymakers to take action. Canada’s persistently weak business investment, relative to its historical performance and that of OECD economies, threatens long-term prosperity and competitiveness.

It is encouraging that Canada’s low productivity and chronic underinvestment have recently gained more prominence in public discourse. Awareness is a critical first step. Addressing the challenge requires decisive action, however: more effective tax and regulatory policies, and a fundamental reorientation of economic policy toward sustained, long-term growth.

The authors extend gratitude to Don Drummond, Alexandre Laurin, John Lester, Nick Pantaleo, Daniel Schwanen, Trevor Tombe and several anonymous referees for valuable comments and suggestions. The authors retain responsibility for any errors and the views expressed.

REFERENCES

Allen Rupert, Wulong Gu and Ryan Macdonald. 2025. “Data, Intangible Capital and Economic Growth in Canada.” Statistics Canada Catalogue 11F0019M, No. 482. March 13.

Bafale, Mawakina, and William B.P. Robson. 2022. “Canadian Investment in Intellectual Property Products is Too Low.” Intelligence Memo. Toronto: C.D. Howe Institute. May.

Baker, Scott R., Nicholas Bloom, and Steven J. Davis. 2016. “Measuring Economic Policy Uncertainty.” Quarterly Journal of Economics 131(4): 1593-1636.

Bank of Canada. 2025. “Business Outlook Survey – Third Quarter of 2025.” October.

Bazel, Philip, and Jack Mintz. 2021. “2020 Tax Competitiveness Report: Canada’s Investment Challenge.” SPP Research Papers 14(21). University of Calgary.

Boadway, Robin, and Jean-Francois Tremblay. 2016. Modernizing Business Taxation. Commentary 452. Toronto: C.D. Howe Institute. June.

Caselli, Francesco, and James Feyrer. 2007. “The Marginal Product of Capital.” The Quarterly Journal of Economics 122(2): 535-568.

Casi, Elisa, Mohammed Mardan, and Barbara M.B. Stage. 2023. Citizenship/Residence by Investment and Digital Nomad Visas: The Golden Era of Individual Tax Evasion and Avoidance? NHH Department of Business and Management Science Discussion Paper 2023/12. Bergen: Norwegian School of Economics, Department of Business and Management Science. August.

Cette, Gilbert, Jimmy Lopez, Giuseppe Nicoletti, and Oceane Vernerey. 2025. “The Potential Impact of Pro-competitive Regulatory Reforms on Productivity and Growth in Canada.” International Productivity Monitor, No. 49, Fall 2025.

Chen, Duanjie, and Jack M. Mintz. 2015. “The 2014 Global Tax Competitiveness Report: A Proposed Business Tax Reform Agenda.” SPP Research Papers 8(4). University of Calgary.

Chodorow-Reich, Gabriel, Matthew Smith, Owen Zidar, and Eric Zwick. 2023. “Tax Policy and Investment in a Global Economy.” Working Paper no. 2023-141. Becker Friedman Institute for Research in Economics, University of Chicago. November.

Crawford, Steven, and Garen Markarian. 2024. “The Effects of the Tax Cuts and Jobs Act of 2017 on Corporate Investment.” Journal of Corporate Finance 87. August.

Cross, Philip, and Jack Mintz. 2024. “Canada’s Resource Sector: Protecting the Golden Goose.” Ottawa: Macdonald Laurier Institute.

Dachis, Benjamin, and John Lester. 2015. Small Business Preferences as a Barrier to Growth: Not So Tall After All. Commentary 426. Toronto: C.D. Howe Institute.

Doyle, Matthew, Mikal Skuterud, and Christopher Worswick. 2024. Optimizing Immigration for Economic Growth. Commentary 662. Toronto: C.D. Howe Institute.

Grootendorst, Paul, Javad Moradpour, Michael Schunk, and Robert Van Exan. 2022. Home Remedies: How Should Canada Acquire Vaccines for the Next Pandemic? Commentary 622. Toronto: C.D. Howe Institute. May.

Gu, Wulong. 2024. “Investment Slowdown in Canada After the Mid-2000s: The Role of Competition and Intangibles.” Analytical Studies Branch Research Paper Series, Statistics Canada. February 22.

Halpern-Shavim, Zvi, and Elena Balkos. 2023. “Evaluating Canada’s New Federal Luxury Tax.” Perspectives on Tax Law and Policy 4(1).

Kronick, Jeremy M., and William B.P. Robson. 2023. “Special Taxes on Large Canadian Banks and Life Insurers: How Necessary? How Evil?” Perspectives on Tax Law and Policy 4(1).

Laurin, Alexandre. 2018. “Unhappy Returns: A Preliminary Estimate of Taxpayer Responsiveness to the 2016 Top Tax Rate Hike.” E-Brief. Toronto: C.D. Howe Institute.

Lester, John. 2022. “Tax Support for R&D and Intellectual Property: Time for Some Bold Moves.” E-Brief. Toronto: C.D. Howe Institute, July.

_________. 2025. “An Economic Strategy for Canada’s Next Government.” Special Policy Report. Toronto: C.D. Howe Institute, April.

_________. 2024 “Federal Business Subsidies: Explosive Growth Since 2014.” SPP Research Papers 17(1). University of Calgary.

Mahboubi, Parisa. 2025. “Liberal immigration plan needs more clarity”. Intelligence Memo. Toronto: C.D. Howe Institute. November.

Marion, Stéfane, and Alexandra Ducharme. 2024. “Canada is caught in a population trap.” National Bank of Canada. January 15.

Marple, James. 2021. “Meeting Canada’s Innovation Challenge through Targeted Investment and Competition.” TD Economics. July.

Mathur, Aparna, and Cody Kallen. 2017. “Business Tax Reform, Investment and GDP: Potential Impacts of the Tax Cuts and Jobs Act.” Daily Tax Report 1-7. American Enterprise Institute. December.

McCormack, Carter, and Weimin Wang. 2024. “Canada’s gross domestic product per capita: Perspectives on the return to trend.” Statistics Canada. April 24.

McKenzie, Kenneth J., and Michael Smart. 2019. Tax Policy Next to the Elephant: Business Tax Reform in the Wake of the US Tax Cuts and Jobs Act. Commentary 537. Toronto: C.D. Howe Institute. March.

Milligan, Kevin. 2014. Tax Policy for a New Era: Promoting Economic Growth and Fairness. Benefactors Lecture 2014. Toronto: C.D. Howe Institute and Chartered Professional Accountants Canada.

Mintz, Jack M., and V. Balaji Venkatachalam. 2020. “Adjusting to Reality: As Proposed, Restricting Corporate Interest Deductibility Is Ill-Advised.” E-Brief. Toronto: C.D. Howe Institute. April.

Mintz, Jack M. 2022. “A Proposal for a ‘Big Bang’ Corporate Tax Reform.” SPP Research Papers. University of Calgary.

Omran, Farah, and Jeremy Kronick. 2019. “The Productivity Opportunity in Canada’s Financial Sector.” Intelligence Memo. Toronto: C.D. Howe Institute. November 21.

Organisation for Economic Co-operation and Development. 2009. Measuring Capital – OECD Manual 2009: Second edition. Paris: OECD Publishing. https://doi.org/10.1787/9789264068476-en.

Porter, Douglas. 2023. “Canada’s Perennial Productivity Puzzle.” Focus: A Weekly Financial Digest. Bank of Montreal. November 3.

_________. 2024. “Canadian Growth: Time for a Rethink.” BMO Economics. March 8.

Rao, Someshwar, Jianmin Tang, and Weimin Wang. 2003. “Canada’s Recent Productivity Record and Capital Accumulation.” Industry Canada.

Raymunt, Monica. 2023. “VW lays off workers at key EV factory over cratering demand.” The Financial Post. September 14.

Robson, William B.P., and Mawakina Bafale. 2022. Decapitalization: Weak Business Investment Threatens Canadian Prosperity. Commentary 625. Toronto: C.D. Howe Institute. August.

_________. 2025. “We Need to Get Going on Canada’s Four-Alarm Productivity Emergency.” Intelligence Memo. Toronto: C.D. Howe Institute. October.

Robson, William B.P. 2024. “Weak Canadian Investment and Productivity: How Tax Policy Can Help.” Canadian Tax Journal.

_________. 2025. “Fiscal Fantasies: Four Incredible Projections in the November 2025 Federal Budget.” C.D. Howe Institute Verbatim. November 13.

Robson, William B.P., Don Drummond, and Alexandre Laurin. 2023. The Morning After: A Post-Binge Federal Shadow Budget for 2023. Commentary 638. Toronto: C.D. Howe Institute. February.

Sala-i-Martin, Xavier. 1997. “I Just Ran Four Million Regressions.” National Bureau of Economic Research. Working Paper 6252.

_________. 2001. “15 Years of New Growth Economics: What Have We Learnt?” Speech, Fifth Annual Conference of the Central Bank of Chile. November.

Schwanen, Daniel. 2018. “NAFTA: The Case for More Competition in the Dairy Market.” Intelligence Memo. Toronto: C.D. Howe Institute. September.

Sharpe, Andrew, and Tim Sargent. 2023. “The Canadian Productivity Landscape – An Overview.” Canadian Tax Journal 71(4).

Singh, Kartikeya, and Aparna Mathur. 2019. “The Impact of GILTI and FDII on the Investment Location Choice of U.S. Multinationals.” Columbia Journal of Tax Law 10(2). September.

Skuterud, Mikal. 2025. “The Growing Data Gap on Canada’s Temporary Resident Workforce.” E-Brief. Toronto: C.D. Howe Institute. February.

Stewart, Luke A., and Robert D. Atkinson. 2013. “Restoring America’s Lagging Investment in Capital Goods.” The Information Technology & Innovation Foundation. October.

Trebilcock, Michael. 2017. “Ontario’s Green Energy Experience: Sobering Lessons for Sustainable Climate Change Policies.” E-Brief. Toronto: C.D. Howe Institute.

Wen, Jean-Francois, and Fatih Yilmaz. 2020. “Tax Elasticity Estimates for Capital Stocks in Canada.” IMF Working Paper WP/20/77.

The views expressed here are those of the authors and are not attributable to their respective organizations. The C.D. Howe Institute does not take corporate positions on policy matters.

Budget 2025 with Bill Robson: What Canadians Need to Know

November, 2025 – Canada does not have a credible fiscal plan. After Ottawa revealed the details of its “sea change” budget, the C.D. Howe Institute’s President and CEO Bill Robson explains why Mark Carney’s first budget in the age of Trump fails to get a passing grade.

Canada is facing significant budgetary challenges, with projected deficits and increased government spending raising concerns about fiscal sustainability and economic health.

May, 2025 – Canada cannot rely on immigration alone to address the challenges posed by its ageing population and relentless decline in fertility rates [ see Canada’s Soaring Housing and Living Costs Stop Baby Making CP], according to a new report from our friends at the C.D. Howe Institute. Without a broader population strategy, rising immigration could fuel rapid growth while straining housing, healthcare, and infrastructure – without fully resolving rising old-age dependency ratios or labour force pressures.

In this post, Daniel Hiebert confronts an important policy dilemma: although immigration increases overall population and helps address short-term labour gaps, the long-term trade-offs are significant. Without corresponding investment and planning, rising immigration risks compounding the very pressures it aims to alleviate.

“This is a particularly opportune moment to reflect on how immigration fits into Canada’s long-term demographic strategy, especially as both permanent and temporary immigration surged between 2015 and 2024, and are now being scaled back,” says Hiebert. “We need to think ahead about what kind of future we are building — and how we get there.”

Based on current patterns, it takes five new immigrants to add just one net new worker, once dependents and added consumer demand are factored in — a reality that undermines assumptions about immigration as a direct fix for labour shortages.

Hiebert argues that Canada must move beyond short-term immigration planning and adopt a long-range population strategy — one that combines immigration with other tools like delayed retirement, increased workforce participation, and stronger productivity growth. The alternative, he warns, is a “population trap”: a scenario where growth outpaces the country’s capacity to support it, undercutting prosperity in the process.

The report also calls on governments to coordinate immigration levels with long-term planning in housing, healthcare, education, and infrastructure.

“There’s no question that immigration is integral to Canada’s future,” says Hiebert. “But assuming it can carry the load alone ignores the structural pressures we’re facing — and the investments we need to make today to ensure future stability.”

Balancing Canada’s Population Growth and Ageing Through Immigration Policy

Canada faces twin demographic pressures: an ageing population and rapid population growth driven by immigration. The report argues that immigration levels must strike a careful balance – sufficient to offset some effects of low fertility and an ageing workforce, but not so high as to outpace infrastructure and economic capacity.

A sustainable population strategy requires coordinated planning across immigration, infrastructure, workforce participation, and capital investment. The report calls for long-term planning that aligns immigration policy with economic and social goals and emphasizes the need to manage absorptive capacity to avoid overburdening housing, healthcare, and public services.

Introduction

Declining fertility is a global trend and is especially pronounced in countries with high levels of economic development. These countries share the common challenge of ageing populations, with rising old-age dependency ratios (OADRs)1 and a shrinking portion of the population in prime working age. Several policy responses have been established to deal with this emerging reality, including pronatalist and other family-based social programs, efforts to enhance automation and productivity, incentivization of a larger proportion of the population to enter the formal labour force, delaying retirement benefits, and increasing the rate of immigration. The success of these approaches has varied, raising critical questions for policymakers: which strategies are the most efficient? What are their costs? And which policies offer the best balance between risk and reward?

This Commentary explores the potential role and limitations of immigration in alleviating Canada’s challenges of low fertility and ageing. This is a particularly opportune moment to consider such an issue given that both permanent and temporary immigration strongly increased between 2015 and 2024 and will be reduced for the 2025 to 2027 period.

Using custom demographic projections, this paper examines how various immigration scenarios – ranging from historical rates to the peak of 2024 – will affect Canada’s demographic outlook over the next 50 years. The analysis investigates the role immigration could play in mitigating the effects of an ageing population, while also acknowledging the associated trade-offs, including pressures on infrastructure and rapid population growth. The findings highlight that Canada’s immigration policy, while important, should be framed within a long-term population strategy that aligns immigration policy with broader economic and social goals – including capital investment, productivity, delayed retirement, and expanded social infrastructure – to ensure sustainable growth and enhanced prosperity for all Canadians.

Canada’s Demographic Challenge and Recent Immigration Policy Responses

Canada’s current demographic challenge is the product of two primary factors: low fertility and the ageing and retirement of the Baby Boom generation. Canada’s fertility rate first rapidly declined from the peak of the Baby Boom (1950s) to the early 1970s, when it first fell below the replacement level. Since then, it has continued with a slower, though persistent decline, interrupted by occasional slight recoveries. Most recent calculations reveal that Canada’s fertility rate is now at 1.26 – a level unprecedented in Canadian history and among the lowest globally. The consequences of low fertility are particularly pronounced today due to the ageing of the Baby Boom generation. In 2025, this cohort ranges in age from 59 to 79 years old, while the average age of retirement in Canada was 65.1 in 2023. Around two-thirds of boomers have already reached the age of 65, with the remaining third expected to follow in the coming years. The impact of this demographic shift is therefore ongoing and continues to affect the labour market and economy at large.

Throughout its history, Canada has turned to immigration to resolve demographic challenges (Hiebert 2016). From the late 1940s to the mid-1980s, Canada admitted an average of 150,000 permanent residents annually, though numbers fluctuated. By the end of that period, concerns over low fertility began to be articulated. This prompted the government to increase annual immigration levels to 250,000, a figure that was quite consistent over the following 30 years, with annual rates ranging from the low to high 200,000s. By the end of the 20th century, immigration accounted for over half of Canada’s population growth and labour force expansion.

The most recent shift in immigration policy began in late 2015 under the Liberal government, which pursued an expansionary strategy. Annual immigration targets and admission levels increased – save for the 2020 pandemic year – leading to a target of 500,000 for 2025. However, this target will no longer be realized following the revised plan announced at the end of 2024. Along with increased permanent immigration, the government had adopted a more facilitative approach to temporary migration, leading to rapid growth in the number of international students, temporary foreign workers, and other non-permanent residents. In 2023, the Canadian population expanded by 1.27 million, representing an annual growth rate of 3.2 percent, which is highly unusual among advanced economies. For example, the average population growth rate of the other G7 countries in 2023 was less than 0.5 percent (Scotiabank 2023).2

Given Canada’s low fertility, 98 percent of this growth stemmed from net immigration, both temporary and permanent (Statistics Canada 2024a). Today, Canada is approaching a point where all population growth and most of the impetus for population renewal (Dion et al. 2015) will come from immigration. However, the “big migration” trajectory of 2015 to 2024 has shifted. While public opinion historically supported ambitious immigration targets, this sentiment changed sharply in 2024. Concerns about housing shortages, infrastructure strain, and what has been termed a “population trap” – where population growth outpaces capital investment capacity – have fueled resistance to current immigration levels. These pressures clearly influenced the 2025 to 2027 plan, which curtails permanent immigration targets by approximately 20 percent and tightens restrictions on temporary migration programs.

Short- and Long-Term Immigration Policy

Before focusing on the relationship between immigration and demography, it is instructive to explore a fundamental tension in immigration policy: should the Government of Canada prioritize the “maximum social, cultural and economic benefits of immigration”3 for today or for the future? These goals may not always align: satisfying the needs of today may have long-term consequences – a trade-off familiar to anyone who has managed a budget.

It has been long underappreciated that Canada’s immigration policy is built around a combination of short- and long-term goals. Economic selection practices provide a helpful example. Since the introduction of the points system nearly 60 years ago, selection priorities have oscillated between addressing short-term labour market needs (e.g., incorporating and/or prioritizing job offers in selection criteria) and building the human capital of the future workforce, under the assumption that highly skilled individuals can adapt and drive productivity, and therefore prosperity. Striking the right balance between these priorities is challenging and requires careful planning.

The balance between short- and long-term immigration perspectives is reflected in the combination of the economic selection system and levels planning. The former – which includes permanent skilled immigration – involves trade-offs between filling immediate labour shortages and building future human capital.4 The latter determines the scale and composition of Canada’s permanent immigration system. In contrast, temporary migration programs are almost entirely shaped by short-term planning horizons – with the partial exception of the International Student Program, which operates in accordance with a medium-term planning horizon in five-year increments.5

These issues are pivotal to considerations of the relationship between immigration and demography. The impact of immigration extends beyond the number of admissions. If immigrants are selected to enhance the human capital of Canada’s workforce and integrate productively, they can potentially raise per capita GDP and mitigate the challenges of an ageing population (Erkisi 2023; Montcho et al. 2021). Conversely, if the system prioritizes lower-skilled individuals, fails to utilize the skills of highly educated immigrants, or admits newcomers at a scale that exceeds the economy’s capacity to absorb them, it risks lowering per capita GDP and compounding demographic challenges (Smith 2024).

Immigration, therefore, has both scale and compositional effects. Scale impacts include changes to population size, age structure, and regional distribution, which directly affect housing demand and social services. Compositional impacts include broader socioeconomic outcomes such as income inequality, productivity, and trade relationships. While this paper focuses on scale impacts, readers should bear these compositional effects in mind.

Another critical consideration is the relationship between admission levels and the expected economic outcome of admitted immigrants. In Canada’s Express Entry system, admission thresholds are adjusted based on the number of entries. Larger admission cohorts tend to lower the points threshold, potentially reducing the overall human capital of entrants (Mahboubi 2024).

Immigration and Canada’s Demographic Challenge

This paper argues that long-term considerations should play a larger role in immigration levels planning. Immigration decisions made today shape Canada’s demographic structure for decades, as immigrants become part of the population, contribute to fertility, enter the workforce, and eventually retire. These stages must be incorporated into demographic projections and policy planning, yet they are often overlooked due to the focus on immediate needs and political cycles.

To illustrate the long-term demographic impact of immigration, consider two extreme scenarios. In the first, Canada’s fertility rate declines to 1.0 (the 2023 rate in British Columbia) and net migration falls to zero, implying no population growth from migration. Under these conditions, Canada’s population would shrink from 40 million in 2023 to 12.3 million by 2100. In the second scenario, the extraordinary 2023 growth rate of 3.2 percent continues indefinitely, with rising migration levels. By 2100, Canada’s population would reach 452 million.

While neither of these scenarios is realistic, they illustrate the decisive influence that fertility and migration have in shaping the future scale of Canada’s population. Despite their seemingly preposterous nature, the key point remains: with fertility rates remaining low,6 the state is entirely responsible for determining the scale of the Canadian population. Decisions about temporary visas and permanent residence serve as the primary levers of control. Policymakers must recognize that the choices made today will have profound and lasting effects on Canada’s demographic and economic future.

Population Projections and Their Implications

Statistics Canada produced a recent population projection for various scenarios in January 2025, covering the period of 2024 to 2074.7 Across the scenarios, total fertility rates range from 1.13 to 1.66, permanent immigration rates vary from 0.70 to 1.2 percent per year, and net temporary migration figures are assumed to decline in the short term before stabilizing. The selected scenarios suggest that the projected population of Canada would range from 45.2 to 80.8 million in 2074 – a difference of over 35 million people, roughly equivalent to Canada’s current population. The scale of infrastructure and social investments needed to accommodate such growth would be enormous.

Beyond sheer numbers, government policy also affects the age structure of Canada’s future population. The OADR is expected to rise, and increased immigration is often proposed as a solution. However, the retirement age is, to an important extent, a social construct and this paper explores the efficiency of changing Canada’s retirement age compared with adjusting immigration levels to address the issue.

While migration can temporarily mitigate low fertility effects by maintaining a larger workforce, it cannot fully offset population ageing (Robson and Mahboubi 2018). Even doubling Canada’s population through immigration would only reduce the average age by five years, as immigrants’ average age is close to that of the receiving population (around 30 versus 40).8 Doyle et al. (2023) argue that increasing immigration could delay ageing impacts but would require continuously higher volumes, becoming unsustainable.9 Immigrants are typically concentrated in the labour force ages (25-40) but, in 30-35 years, this group will be approaching retirement, creating an economic challenge similar to the Baby Boom generation’s retirement. Unless increasing rates of immigration are in place continuously (an unrealistic scenario), at some point society must adjust to a smaller, older population.

Moreover, there appear to be additional costs to rapid population growth that are driven by high immigration. Doyle et al. (2023 and 2024) contend that when the labour force expands faster than investment in capital and infrastructure, the result is a dilution of capital per worker, reducing Canada’s productivity and living standards. This concern highlights not only the pace of immigration-driven growth but also Canada’s historically low levels of business and infrastructure investment, suggesting a need to boost investment alongside population growth.10

Research shows that while larger immigration targets increase real GDP through a larger labour supply, they could also reduce GDP per capita (El-Assal and Fields 2018).11 Indeed, in recent years of very high population growth through net international migration (2022-2023), Canada’s level of real GDP per capita has been stagnant.12

Furthermore, house price escalation associated with a surge in demand may negatively affect fertility decisions, particularly for families renting homes (Dettling and Kearney 2014; Fazio et al. 2024). In other words, compensating for low fertility through high rates of immigration may indirectly contribute to additional fertility decline.

Studies show that immigration alone has a limited impact on altering age composition (Robson and Mahboubi 2018). Even doubling immigration rates would only slightly improve the OADR (Beaujot 2001). All of the immigrants admitted by Canada between 1951 and 2001, for example, are believed to have reduced the median age of Canadians in 2001 by only 0.8 years.

The effect of younger immigrants, as seen in Australia’s approach, would improve outcomes,13 but Guillemette and Robson (2006) found that this impact would still be modest. An unintended consequence of focusing on younger immigrants is that it contrasts with Canada’s economic selection system, which rewards human capital development. Half of the 2022 Express Entry applicants were 30 or older (IRCC 2022), challenging the idea that immigration could rapidly reduce the average age of the population.14

A Custom Glimpse of the Future

To update our understanding of the role immigration could play in Canada’s demography, this section explores the results of a special population projection, using Statistics Canada’s microsimulation model called Demosim, to assess the impact of varying immigration rates on the Canadian population in the future. Two demographic outcomes are highlighted in this analysis: population size and the OADR.