|

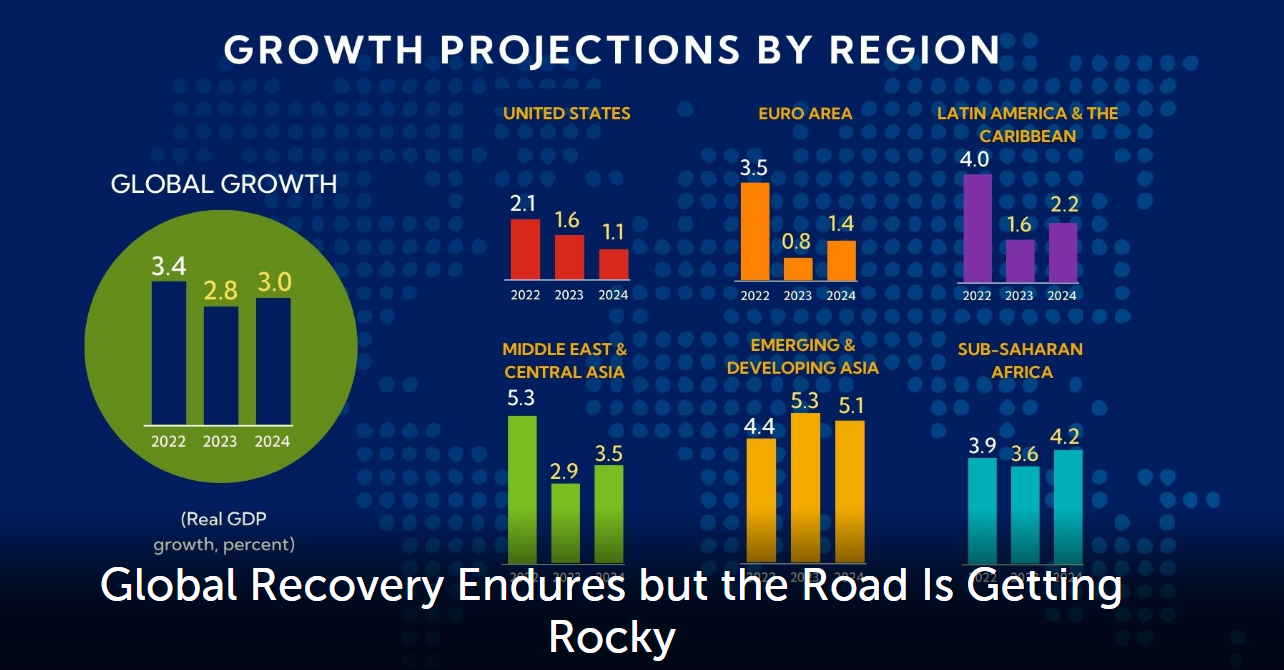

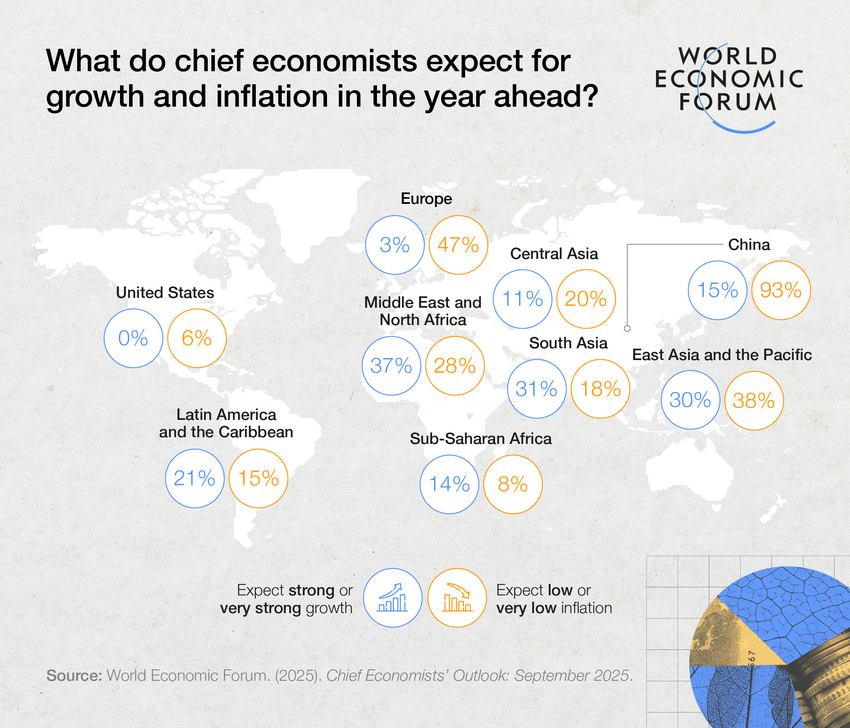

| 中文 | 日本語 | Español Quick Takeaways -72% of chief economists expect global economy to weaken in 2026 as disruptions in trade, technology, resources and institutions signal a shift to a new economic environment. -Regional growth pathways are diverging: 56% anticipate greater divergence between advanced and developing economies, with MENA and South Asia emerging as bright spots. -Debt risks are intensifying in advanced economies, with 80% of respondents expecting vulnerabilities to grow. New York, USA, October 2025 – The global economy is entering a period of weak growth and systemic disruption, according to the World Economic Forum’s latest Chief Economists’ Outlook, published today. Some 72% of surveyed chief economists expect the global economy to weaken over the next year, amid intensifying trade disruption, rising policy uncertainty and accelerating technological change. The findings point to the emergence of a new economic environment shaped by persistent disruption and growing fragmentation. Diverging Pathways in a Fragmented Global Economy The Outlook highlights sharp regional fault lines. Emerging markets are anticipated to be the main engines of growth, with the Middle East and North Africa (MENA), South Asia and East Asia and Pacific seen as bright spots. One in three chief economists expect strong or very strong growth in these regions. The outlook for China is more mixed, with 56% of chief economists anticipating moderate growth, though deflationary pressures are expected to persist. Growth is expected to remain more stagnant in advanced economies. In Europe, 40% expect weak growth with fiscal loosening (74%) and low or moderate inflation (88%). In the United States [& Canada ed.], most chief economists (52%) anticipate weak or very weak growth and high inflation (59%) as monetary policy is loosened (85%). The chief economists warn that advanced and developing economies are on increasingly divergent growth pathways – 56% expect greater divergence over the next three years. Towards a New Economic Environment Chief economists overwhelmingly agree that today’s disruptions are structural rather than cyclical. Large majorities anticipate long-term disruption in natural resources and energy (78%), technology and innovation (75%), trade and global value chains (63%) and global economic institutions (63%). This marks an important shift. The global economy is not so much weathering isolated shocks as realigning, raising the stakes for new forms of leadership, cooperation and resilience. “The contours of a new economic environment are already taking shape, defined by disruption across trade, technology, resources and institutions,” said Saadia Zahidi, Managing Director, World Economic Forum. “Leaders must adapt with urgency and collaboration to turn today’s turbulence into tomorrow’s resilience.” Trade Realignment, Fiscal Strain and Debt Risks Structural shifts in the global economy are playing out most visibly in trade, fiscal policy and debt. Some 70% of surveyed chief economists rate the current level of trade disruption as “very high”, far above other domains of the economy, and over three-quarters also expect disruption to trade and global value chains to cascade into other domains. In financial markets and monetary policy, 45% of surveyed economists rate disruption as high or very high, yet only 21% expect it to last. Even so, while 52% see a major near-term crisis in advanced economies as unlikely, 85% warn that any shock could have wide systemic effects. With global public debt levels mounting, the chief economists surveyed highlight that debt vulnerabilities, once largely associated with emerging economies, are increasingly centred in advanced ones – 80% expect risks in advanced economies to grow in the year ahead. Fiscal vulnerabilities are also more frequently identified among the top growth inhibitors in advanced economies (41%) compared to developing economies (12%). Follow the Sustainable Development Impact Meetings 2025 here and on social media using #SDIM25. About the Chief Economists’ Outlook The report builds on extensive consultations and surveys with chief economists from the public and private sectors, organized by the World Economic Forum’s Centre for the New Economy and Society. The report supports the Future of Growth Initiative, aiming to foster dialogue and actionable pathways to sustainable and inclusive economic growth. About the Sustainable Development Impact Meetings 2025 The Sustainable Development Impact Meetings 2025 takes place from 22 to 26 September in New York, bringing together over 1,000 global leaders from diverse sectors and geographies. Held ahead of the World Economic Forum Annual Meeting 2026, these meetings are part of the Forum’s year-round work to accelerate progress on the growth, resilience and innovation through multistakeholder dialogues and action. |

For the Silo, Jarrod Barker.